Submitted:

20 September 2024

Posted:

23 September 2024

You are already at the latest version

Abstract

The study aims to explain the relationship of financial literacy with spending habits and behavior. Financial behavior is a mediator of Generation Z. Financial literacy is a very important dimension in making financial decisions, and this research highlighted the direct and indirect impacts that financial literacy exerts on spending behavior. Data is collected from 317 respondents using a structured questionnaire measuring financial literacy, financial behavior, and spending behavior. Correlation, regression, mediation analysis, and Structural Equation Modeling have been used in evaluating these relationships. Financial literacy directly reflects a strong relationship with spending behavior, and its coefficient is 1.167. Financial behavior, therefore, exercises a strong mediation effect on this relationship with a mediation coefficient of 0.797, thus indicating that financial behavior is an essential tool in successfully translating financial knowledge into responsible spending. From these findings, greater financial literacy and responsible financial behavior may increase the aggregate financial efficacy of Generation Z. Although the current study heavily focuses on the fact that financial literacy and behavior are highly associated with financial well-being, it shows that targeted financial literacy education programs on either behavior or financial literacy enhance healthier spending behavior. The scope of future studies involves considering the role of income and personality characteristics as well as an elongation of the time horizon to uncover the impact of financial literacy on shifts in the individual's financial well-being.

Keywords:

financial behavior

; financial literacy

; spending habit

; Generation Z

; exploratory factor analysis

Introduction

Financial literacy is the most urgent need for Gen Z as it begins navigating its personal finance. The cost of living continues to rise, in addition to being easily accessible digitally, which means this generation faces unique challenges. Financial education would enable Gen Z to prioritize clear goals, forward planning, and the avoidance of terrible spending habits and high-interest debt (Shan et al., 2023). Added to that, financial literacy increases their ability to make proper financial planning and avoid risky financial products (Andiani & Maria, 2023). However, at the same time, despite these benefits, the financial knowledge relationship with actual spending still remains poorly understood since research shows that although more financial literacy is well related with more spending behavior, it is in fact the positive financial behavior which leads to a better saving result (Rodriguez et al., 2024).

What is probably lacking in the present studies are the ways through which financial behavior acts to mediate the relationship between financial literacy and spending habits among Gen Z. Compared to other types of study, only a few have looked into the interaction between these elements. Understanding how financial knowledge influences behavior and spending will thus form a more solid base to gain a more profound understanding of the best ways Gen Z can improve their financial outcomes and develop healthier spending and saving habits. This will serve to fill a gap that may exist and contribute toward developing even more effective financial education programs for the next generation.

Statement of the Problem

This study wants to examine the mediation effect of financial behavior to financial literacy and spending habits among Gen Z. In specific, this study wants to uncover the following questions:

- RQ1: Is there a significant relationship between Financial Literacy and Spending among Gen Z?

- RQ2: How does financial behavior mediate the relationship between financial literacy and spending habits of Gen Z?

- RQ3: To what extent does financial literacy influence the financial behavior of Gen Z?

- RQ4: What role does financial behavior play in shaping the spending habits of Gen Z?

Hypothesis

Based on the research question, here are the following hypotheses derived:

- HO1: There is no significant relationship between financial literacy and spending habits among Gen Z.

- HO2: Financial behavior does not mediate the relationship between financial literacy and spending habits among Gen Z.

- HO3: Financial literacy does not significantly influence the financial behavior of Gen Z.

- HO4: Financial behavior does not significantly influence the spending habits of Gen Z.

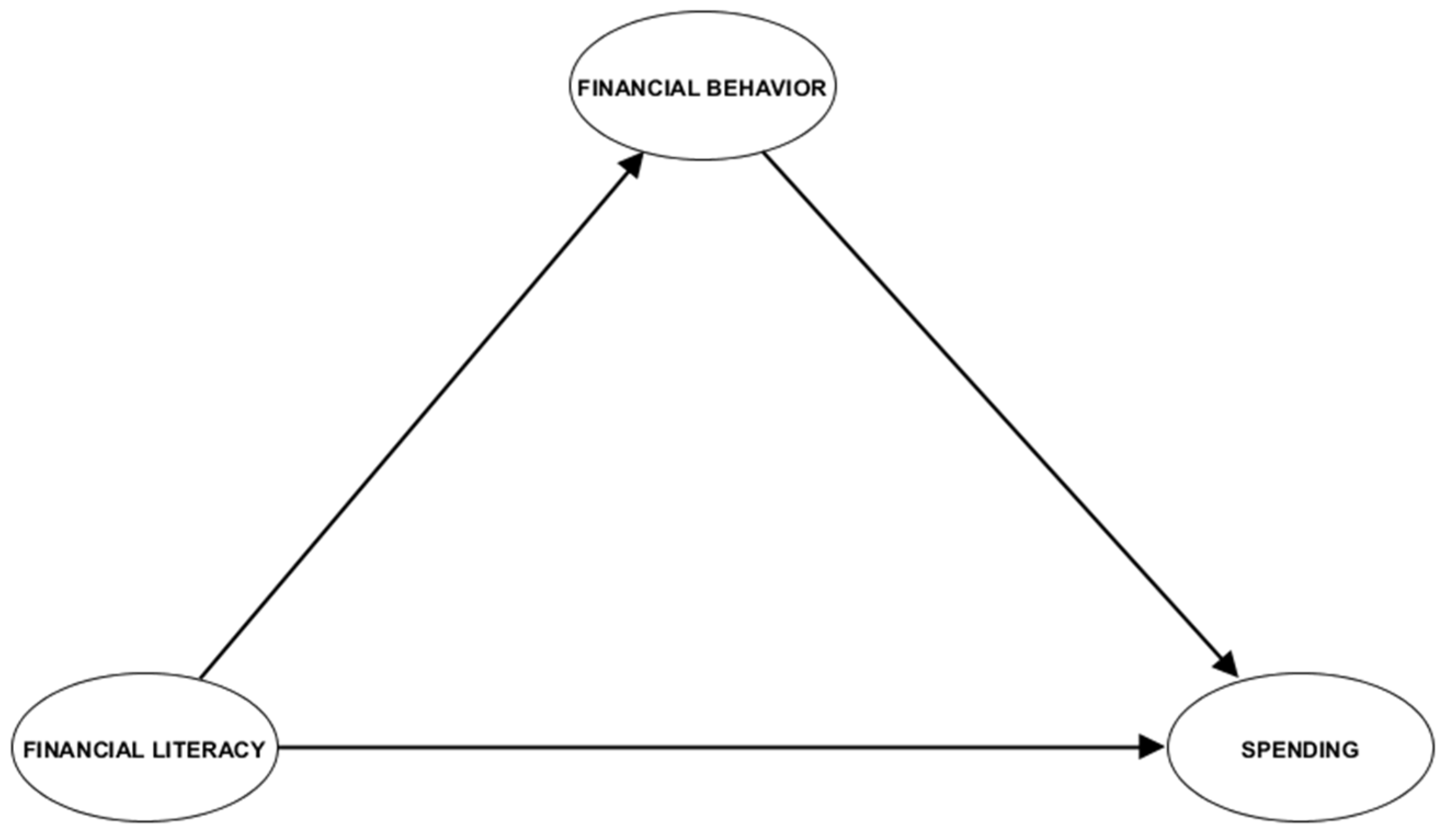

Conceptual Framework

The conceptual framework shows how financial literacy affects expenditures directly and indirectly through financial behaviors. It further argues that the better his or her financial knowledge, the better the spending decision he or she makes while also adopting positive financial behaviors like budgeting and saving, which also influence his or her spending. It is, in other words, financial behavior that bridges this relationship between spending and financial literacy. This framework will help one understand if high financial literacy leads to better spending practices and if there is a principal role of financial behavior in this process.

Figure 1.

Conceptual Framework.

Review of Related Literature

The Relationship between Financial Literacy and Spending Habits of Gen Z

Financial literacy plays an important role in setting clear financial goals and planning the future, but in turns affects how the choices of spending are made (Shan et al., 2023). Studies determined that having digital financial literacy had a high positive impact on saving and shopping behaviors, indicating that financial education had to be included in the digital age (Alysa et al., 2023). There are also aspects of financial literacy and buying habits connected with money management, which indicate that the better a person’s financial knowledge, the better the finances will be managed (Wuisang et al., 2023). This is an interesting fact that more financial literacy is associated with more spending behavior. Such a relationship calls for an investigation into how it might reflect better and more conscious spending rather than impulsive financial decisions (Rodriguez et al., 2024). Essentially, such findings reveal the impact of financial literacy on saving and spending behaviors, thereby concluding that educating members of Gen Z on financial matters will assist in the focused management of money.

The Mediation of Financial Behavior to Financial Literacy and Spending Habits of Gen Z

For members of Generation Z, financial behavior can be considered to mediate the gap between financial literacy and spending habits. Rather than directly, several studies have reflected that financial literacy combines with a host of factors such as income and self-control to significantly influence financial management behavior, which therefore dictates spending patterns (Anjani & Darto, 2023). More studies also highlight financial self-efficacy, locus of control, and lifestyle, as aspects that affect the consumer’s financial behavior, thereby developing the connection between financial literacy and consumption-related choices (Ulumudiniati & Asandimitra, 2022). Consumerist behavior has also been found to act as a mediator between financial management and lifestyle, which simply means that financial behavior impacts the way that financial literacy translates into real-world consumption patterns (Mahendra et al., 2023). Importantly, financial behavior is thought to be a mediator in the relationship between financial literacy, attitudes, and personal financial management, and therefore underlines its role in linking financial knowledge with effective money management (Purboningrum & Fathoni, 2023). This relates to the fact that improvements in financial behavior may be one of the ways to ensure the practical changes in financial literacy will lead to appropriate spending.

The Influence of Financial Literacy on Financial Behavior of Gen Z

This is why financial literacy takes the center stage in establishing the attitude of Generation Z towards their finances. It aids in setting priorities and defining objectives for managing their financial condition and, later on, commands the flow of its usage (Shan et al., 2023). Empirical studies reveal that income and self-control come together with financial literacy and shape the financial management behavior that results in better financial outcomes for this generation (Anjani & Darto, 2023). Besides influencing financial management behavior, financial literacy also has implications on the investment decisions and consequently directs Gen Z towards more strategic financial choices as underlines Ulfa et al., 2023. Family factors such as father education, discussion of financial matters are critical predictors of sound financial behavior; that is to say once again that financial literacy is a vital input for responsible financial decision-making, as concludes Meriku et al., 2023. Above all, findings indicate that financial literacy combined with self-control positively impacts the current performances of individuals, with self-control appearing especially favourable for more educated individuals (Mawad et al., 2022). This again shows that financial literacy is crucial in inculcating disciplined and thoughtful financial behaviors among Gen Z.

The Influence of Financial Behavior on Spending Habits of Gen Z

Financial behavior has a great impact on the spending habits of Generation Z, because often through financial integration and the influence of socialization agents on their financial attitude, they cannot save well nor spend well (Qamar et al., 2023). More financial knowledge was directly related to more desirable financial behavior and this in turn, to healthier spending habits according to Azmi & Ramakrishnan (2018). Further, being positive financially has been related to better financial well-being and better financial well-being in young Gen Zers as it helps reflect good management of finances for their overall financial health (Shankar et al., 2022). Further, their investment, debt management, and expenditure activities are the mediating factors between the socioeconomic variables and personality characteristics or their financial life satisfaction since how Gen Z decides to operate their finances seems to hold sway over the outcomes with regard to their finances. This is an added proof that sound financial behavior needs to be inculcated so as to engender optimum expenditure and financial well-being in Gen Z.

Methods

Research Design

This study attempts to establish associations between financial literacy and financial behaviors, and also spending habits with Generation Z, using a quantitative research design. In general, the primary aim is to measure the association between financial literacy and spending habits, as well as to examine how financial behaviors mediate this relationship, and the direct impact of financial literacy on financial behaviors.

Population and Sampling

Respondents for this study will be members of Generation Z. This age range consists of individuals from 18 to 25 years old in 4 barangays in Quezon City. Different backgrounds would be included within the study, so the population sample size of 317 would be used to determine the required minimum to achieve adequate statistical power. The researcher used stratified random sampling where it is helpful in determining the variations across socioeconomic status, educational background, and geographical location.

Data Collection

Data was collected through a structured questionnaire on financial literacy, financial behavior, and spending habits. The questionnaire will be based on validated scales that exist in the literature on conducting the study, incorporating some demographic information to control for variables such as income and education. An online form will use platforms where surveys can be administered online.

Statistical Tools Used

This study used various statistical tools to understand how the relationships exist among these variables. Specifically, Pearson’s correlation analysis will be applied to analyze the relationship that financial literacy has with spending habits, whereas mediation analysis and Structural Equation Modeling will test whether financial behavior mediates this relationship. To examine the role of financial literacy on financial behavior, one would conduct a regression analysis and then another regression analysis to see whether financial behavior predicts spending habits. Therefore, these tools will offer an all-around understanding of the roles that interconnect financial literacy and behavior in molding the spending habits of Generation Z.

Result

The Relationship between Financial Literacy and Spending Habits

Table 1 shows a strong positive relationship between financial literacy and spending habits since Pearson’s r = 0.821, and the p-value is less than 0.001, showing a statistically significant. It indicates that the higher the level of financial literacy, there is more spending behavior. In the previous studies show that beyond just facilitating and having well-defined financial goals and plans for the future, financial literacy also affects how spending decisions are made (Shan et al., 2023). Furthermore, financial literacy has been shown to affect saving and shopping behaviors in this digital era (Alysa et al., 2023). According to Wuisang et al. (2023), the more financially literate an individual is, the better money management skills he or she develops-underlining its importance. It is of interest that although high financial literacy is associated with higher spending, this could simply be an expression of more mindful, intentional spending rather than impulse buying (Rodriguez et al., 2024). In a broader sense, the strength of the relationship suggests that financial education is important in pointing Gen Z in the direction of better-informed and healthier financial choices.

Mediation of Financial Behavior to Financial Literacy and Spending Habits

The results for Table 2 have directly pointed to the effect of financial literacy on spending, with an estimate of 0.642; that is, higher financial literacy influences greater spending behavior. At all conventional levels, the p-value is less than 0.001, thus confirmed. The 95% CI from 0.555 to 0.728 further supports the reliability of this finding. This would mean that financial literacy does have a huge impact on spending decisions. Therefore, it will agree with research stating how better knowledge in finance leads to conscious and informed choices with regards to spending.

As shown in Table 3, the indirect effect of financial literacy on spending through financial behavior is reported to be 0.180. This means that financial literacy will affect spending indirectly since it will influence one’s financial behavior. The z-value in the mediation effect is 5.401, and the p-value is less than 0.001; therefore, this effect is statistically valid. Also, the 95% CI from 0.114 to 0.245 confirms the validity of this result. Therefore, financial behavior is a salient mediating variable for how financial literacy tends to play out in the context of spending decisions, making it important to develop good financial behaviors alongside financial knowledge.

Table 4 shows the total effect of financial literacy on spending, with an estimated value of 0.821. It shows that financial literacy has a very strong and highly significant effect on the spending behavior. The z-value is 25.581 with a p-value less than 0.001, so very statistically significant. The 95% CI of 0.758 to 0.884 further proves the reliability of the finding. This assumes that financial literacy is an extremely strong influencing factor that determines spending habits but indirectly through other factors like financial behavior.

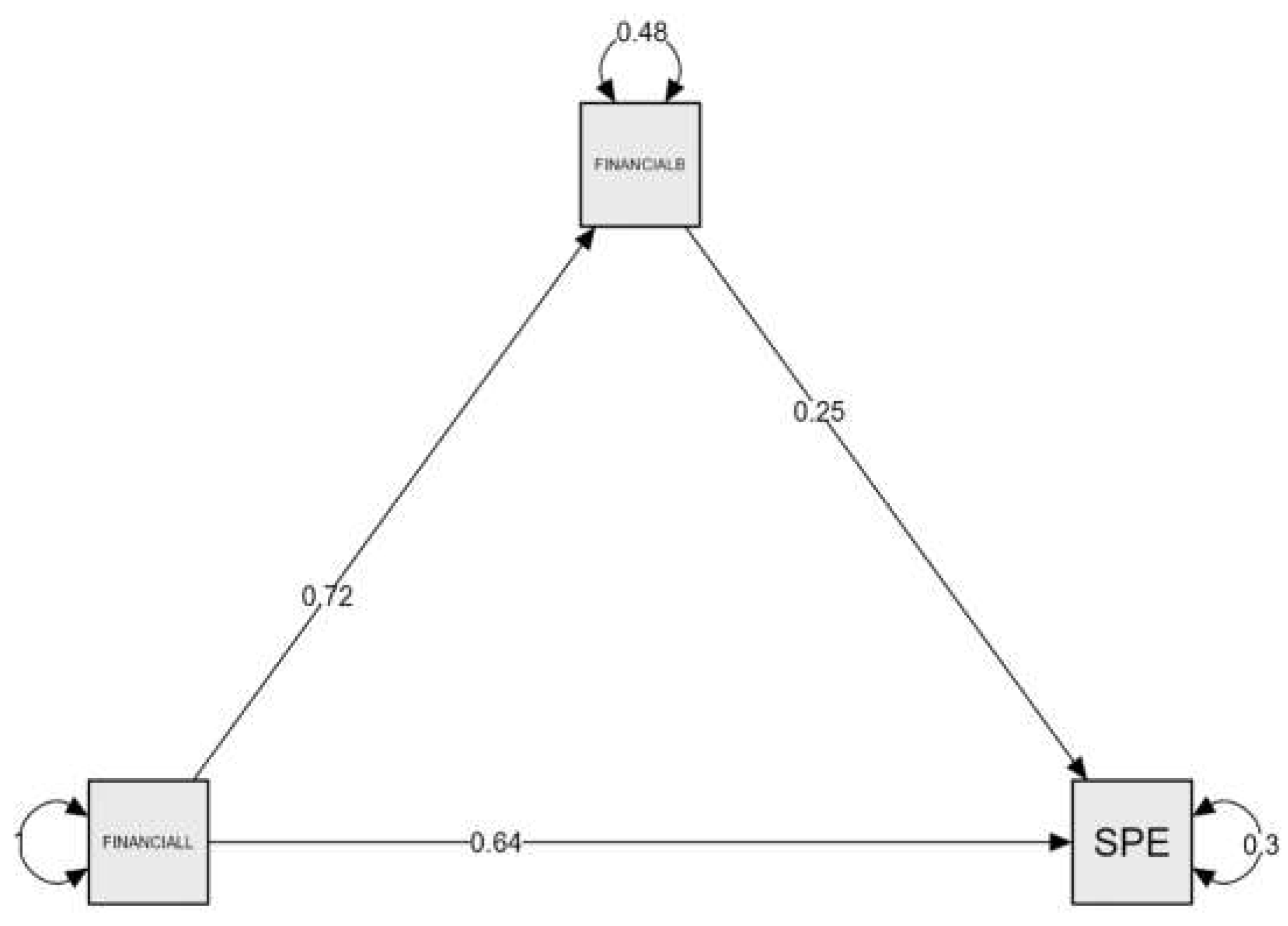

Figure 2.

Path plot Analysis.

Table 5 shows the Path Analysis on Financial Literacy, Financial Behaviour, and Spending Habits Which Show the Significant Relationships between the Variables Concerned Financial literacy has a direct impact on spending habits, which confirms that financial behavior does indeed act as a mediator. This corresponds to research findings that indicate that financial literacy interacts, for example, with income, self-control, and self-efficacy in managing finances to influence behavior, which further serves to affect spending (Anjani & Darto, 2023; Ulumudiniati & Asandimitra, 2022). This also says that financial behavior influences how financial literacy is actually transformed into real consumption, thereby underlining its mediating function (Mahendra et al., 2023). This mediation highlights that improving financial behavior is actually what would make sure that financial knowledge is translated into the proper management of money and optimum expenditure decisions (Purboningrum & Fathoni, 2023). Thus, in this way, it is these improvements in financial behavior that are important for translating such financial knowledge into practical financial outcomes, especially for Generation Z.

Influence of Financial Literacy on Financial Behavior

Table 6 Regression Model Summary Showing the Effect of Financial Literacy on Financial Behavior The baseline model, M0, with no predictors, shows zero explanatory power R² and Adjusted R² are at 0.000-and a relatively high RMSE (Root Mean Square Error) of 0.553, which indicates poor model fit. In contrast, M1 with financial literacy as a predictor shows improved fittedness with an R of 0.721, which is a fairly strong positive relationship between financial literacy and financial behavior. The R² for this model is 0.519, meaning that financial literacy accounts for about 51.9% of the variance in financial behavior; the Adjusted R² closely matches at 0.518, confirming a strong model fit. The RMSE is also minimized to 0.384, indicating more accurate predictions. The analysis hence reflects how financial literacy has a robust influence on the behavioral patterns of Gen Z toward finances.

Table 7 ANOVA results of regression models with financial literacy as the predictor of financial behavior Regression sum of squares 50.115 Residual sum of squares 46.365 This result clearly indicates that the regression sum of squares is much larger than the residual sum of squares, meaning financial literacy accounts for a big portion of the variance in financial behavior. At p-value < 0.001, the F-value of 340.478 is huge, thereby confirming the fact that the model is statistically significant. This means that there is an influence of financial literacy on financial behavior, strong and significant, and thus it contributes meaningfully to the overall variance in financial behavior.

Table 8 shows the financial literacy model of regression coefficients for financial behavior. The unstandardized coefficient for financial literacy was 0.707 while the standardized one equated to 0.721, meaning that it had a close positive association between financial literacy and financial behavior. The t-value for this one was 18.452, while its p-value was still less than 0.001, which means that the relationship is indeed statistically significant. The meaning of this simply presents that with increases in financial literacy, then there are increases in financial behavior. The results can be understood to align with the literal notion of earlier findings: financial literacy results in more ideal financial practice, which again influences proper spending behavior or vice versa (Azmi & Ramakrishnan, 2018). Gen Z also frequently suffers from almost chronic disorders in terms of saving and proper spending because of the attitudes toward finance, influenced by socialization and integration (Qamar et al., 2023). On the other hand, there is some evidence that financial literacy does improve good sound financial behavior and correlate with better financial well-being and overall financial health, Shankar et al. (2022). Therefore, teaching good financial practices among Gen Z will result in effective spending habits and lead to building their financial well-being.

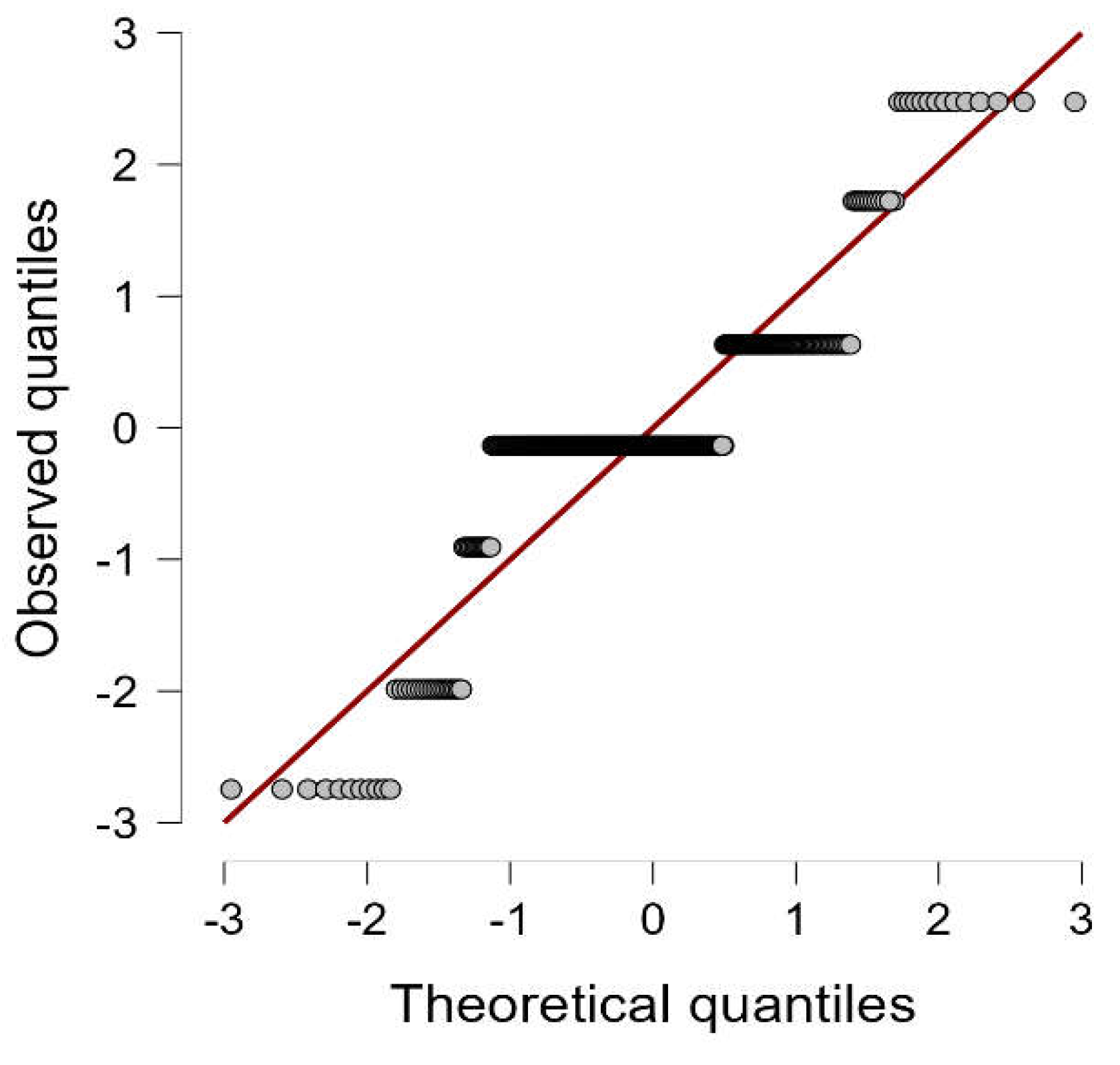

Figure 3 shown the Q-Q plot of standardized residuals with the goal of residual normality in the model. The points on the graph appear to follow the diagonal red line fairly well, which suggests that the residuals are somewhat normally distributed. There are a few minor deviations at the tails, but on average the distribution is very close to normal. This would indicate the fairly satisfied assumptions of normality of residuals. The regression model has come out to be valid from here, which is a positive indicator.

Confirmatory Analysis Factor for Model Fit

Table 9 Descriptive Statistics of Indicators for the Model Fit CFA, the mean values of the indicators range between 3.0189 and 3.3312. This consequently shows that there is consistency in the responses. The variances were also small indicating that the scores were not wide spread. Skewness is negative across the indicators, and it indicates that the data are slightly left-skewed, meaning that respondents tended to give higher ratings. Kurtosis is quite near to zero, and this suggests that the data distributions are relatively normal, with no extreme outliers. In general, these descriptive statistics indicate that the data are suitable for conduct of confirmatory factor analysis and there are no alarming issues related to normality.

Table 10 shows the loadings of the indicator of CFA for constructs Spending, Financial Literacy and Financial Behavior. For Spending, the loadings range between 0.5116 and 0.7937. Here, it is established that moderate to strong relationships exist between indicators and spending constructs, with SPEND. FINLIT: 0.5507 to 0.7785. FINLIT1 is the one with the strongest association with the financial literacy construct. FINBEH: 0.6312 to 0.7517. The loadings are pretty strong, and high in relation to FINBEH2, which would have the highest loading there. In general, it is observable that selected indicators for each construct capture very well the underlying factors; the higher value of most of the loadings over the accepted value of 0.5 supports the correctness of the measurement model.

Table 11 represents the Average Variance Extracted (AVE) of the constructs in this study. AVE to measure convergent validity of the model: Spending = 0.4151; Financial Literacy = 0.4044 and Financial Behavior = 0.4999. These values denote that the constructs explain a moderate amount of variance, while AVE values below 0.5 propose that less than half the variance in the indicators is explained by the constructs. Even though AVE values are just a little below 0.5 which is the recommended threshold for strong convergent validity, they are still close and an indication of reasonable validity but leave room for further refinement of the measurement model.

Table 12 presents the construct reliability of Spending, Financial Literacy, and Financial Behavior with Dijkstra-Henseler’s rho (ρA), Jöreskog’s rho (ρc), and Cronbach’s alpha (α). From the measures given above, all the reliability measures for Spending are above 0.67, with Dijkstra-Henseler’s rho at 0.7031 and Cronbach’s alpha at 0.6805, thus having acceptable reliability. The reliability of Financial Literacy is slightly lower with values on the order of 0.66 for Jöreskog’s rho and Cronbach’s alpha of 0.6568- it indicates potential for improvement but is close to the acceptability thresholds. Financial Behavior has the greatest reliability of the items, with values above 0.74 on every measure, with very strong internal consistency. Overall, the constructs yield reasonable reliability, although financial literacy may require further refinements to increase its internal consistency.

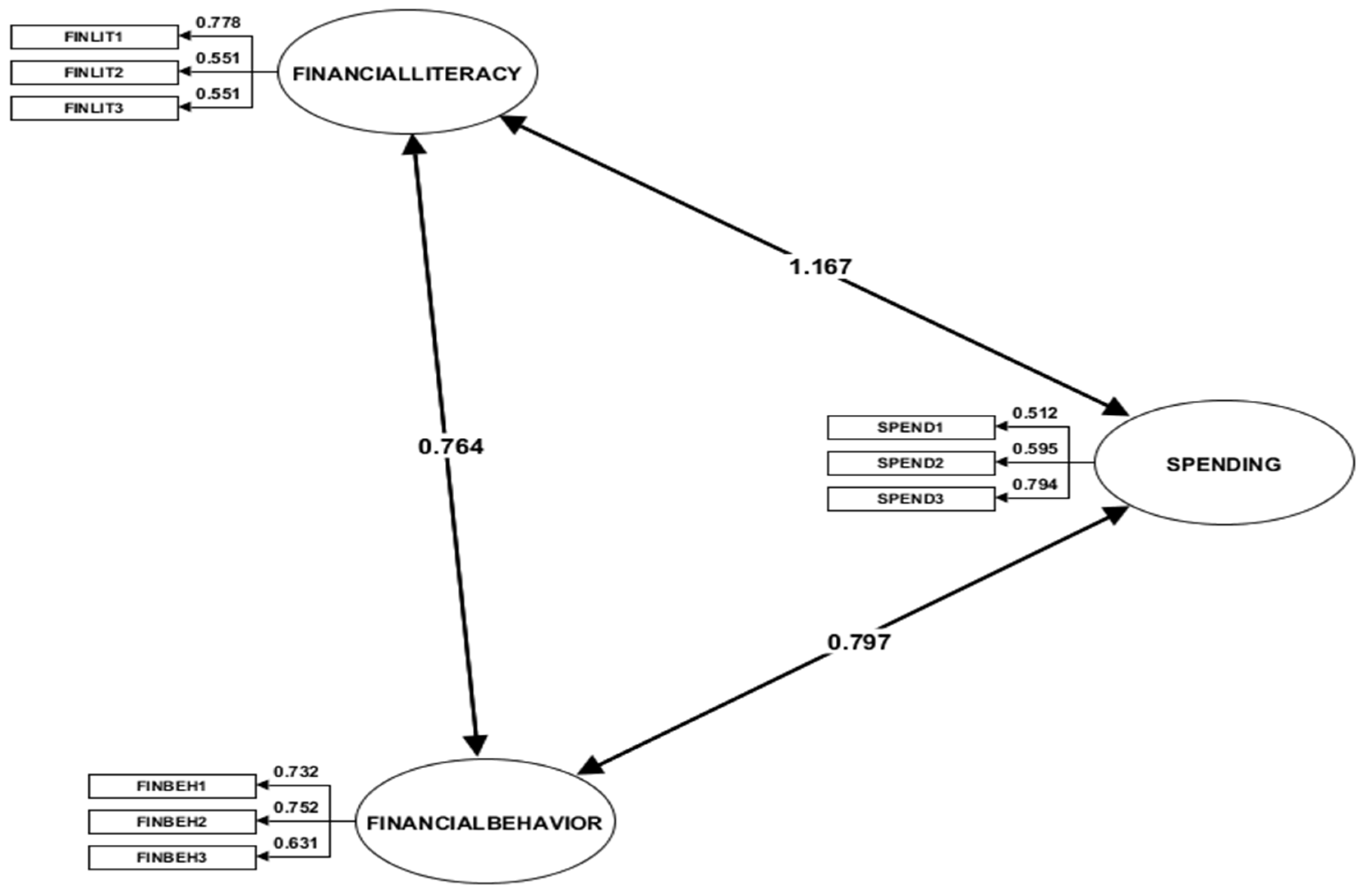

Table 13 Structures Equation Modeling SEM Result: Relationship Among Spending, Financial Literacy, and Financial Behavior Between Financial Literacy and Spending, the coefficient is 1.1666 along with a strong positive relationship; the financial more literate one is, the higher the likelihood of spending. Financial Literacy also correlates with Financial Behavior at 0.7639, which means that financial literacy has a high influence on financial behavior. The coefficient between Financial Behavior and Spending is 0.7971, which shows that financial behavior has a significant positive effect on spending. The results reveal the fact that both financial literacy and financial behavior have an effective influence on spending behavior, where financial behavior acts as a key intermediary variable in relating financial literacy to spending behavior.

The structural equation model (SEM) that captures the relationships between Financial Literacy, Financial Behavior, and Spending is shown above. As illustrated, the path from Financial Literacy to Spending has a high, positive coefficient of 1.167, meaning high financial literacy will likely promote the behavior of spending. It also shows that the coefficient on the path from Financial Literacy to Financial Behavior is 0.764, thus meaning that financial literacy strongly influences financial behavior. The coefficient on the path from Financial Behavior to Spending is 0.797, meaning that good financial behavior also matters in spending. This means that both financial literacy and behavior inform the formation of spending behavior, and in this respect, financial behavior operates as a mediator between financial literacy and spending. In turn, this indicates that financial literacy indirectly leads to good spending through improving financial behavior.

Figure 4.

Structural Equation Model.

Discussion

Conclusions

Financial literacy has been shown to strongly influence direct and indirect expenditure behavior by illustrating financial behavior. Financial behavior has acted as a mediator that in turn goes on to influence the spending decisions between financial literacy and expenditure behavior. To this effect, underscored is the potential effect of the promotion of financial education to develop better financial behaviors that in turn can lead to more conscious and prudent spending habits. Therefore, there is a need to enhance the financial literacy and behavior of Generation Z toward better outcomes and more sustainable financial well-being in the long term.

Recommendation

Thus, financial education programs among the youth, especially this Generation Z generation, should be promoted to improve literacy and behavioral attitudes. The objective of these programs should be to build practical skills through budgeting, saving, and prudent spending. This should also tie in the digital aspects of understanding the new finance world through the grasping of financial literacy.

For future research, it would be interesting to find out how income levels, family influences, and other personality characteristics mediate between financial literacy and behavior and then spending. Longitudinal studies would be used in demonstrations of how relationships shift with time.

Author Contributions

The general planning of the study was taken care of by Joel Mark P. Rodriguez, such that preparation of the research instrument, report writing, and handling data processing and analysis all fell under his care. Ma. Del Carmen G. Labong assisted in sharing the effort necessary for the preparation and planning phase of the research. While this was going on, Lourdes Q. Palallos was curating data, significantly contributed to the planning, assisted in preparing the research instrument, and helped in writing the report. Of such teamwork the study ended up being completed excellently.

Funding

No Funding was granted for this study.

Availability of data and materials

The datasets used and/or analysed during the current study are available from the corresponding author upon reasonable request.

References

- Alysa, A., Muthia, F., & Andriana, I. (2023). Pengaruh Literasi Keuangan Digital terhadap Perilaku Menabung dan Perilaku Berbelanja pada Generasi Z. Al-Kharaj : Jurnal Ekonomi, Keuangan & Bisnis Syariah. https://doi.org/10.47467/alkharaj.v6i3.4706. [CrossRef]

- Andiani, D., & Maria, R. (2023). Pengaruh Financial Technology dan Literasi Keuangan terhadap Perilaku Keuangan pada Generasi Z. Jurnal Akuntansi Bisnis dan Ekonomi. https://doi.org/10.33197/jabe.vol9.iss2.2023.1226. [CrossRef]

- Anjani, C., & Darto, D. (2023). Financial Literacy, Income and Self-Control on Financial Management Behavior of Generation Z. BASKARA : Journal of Business and Entrepreneurship. https://doi.org/10.54268/baskara.5.2.152-164. [CrossRef]

- Azmi, N., & Ramakrishnan, S. (2018). Relationship between Financial Knowledge and Spending Habits among Faculty of Managements Staff. Journal of Economic Info. https://doi.org/10.31580/jei.v5i3.102. [CrossRef]

- Fachrudin, K., Pirzada, K., & Iman, M. (2021). The role of financial behavior in mediating the influence of socioeconomic characteristics and neurotic personality traits on financial satisfaction. Cogent Business & Management, 9. https://doi.org/10.1080/23311975.2022.2080152. [CrossRef]

- Mahendra, R., Nugroho, M., & Pristiana, U. (2023). The Influence of Economic Status, Financial Literacy, Financial Management on Z Generation’s Lifestyle using Consumptive Behavior as Moderation Variable. JOURNAL OF ECONOMICS, FINANCE AND MANAGEMENT STUDIES. https://doi.org/10.47191/jefms/v6-i1-32. [CrossRef]

- Mawad, J., Athari, S., Khalife, D., & Mawad, N. (2022). Examining the Impact of Financial Literacy, Financial Self-Control, and Demographic Determinants on Individual Financial Performance and Behavior: An Insight from the Lebanese Crisis Period. Sustainability. https://doi.org/10.3390/su142215129. [CrossRef]

- Mireku, K., Appiah, F., & Agana, J. (2023). Is there a link between financial literacy and financial behaviour?. Cogent Economics & Finance, 11. https://doi.org/10.1080/23322039.2023.2188712. [CrossRef]

- Purboningrum, S., & Fathoni, M. (2023). Determination Factors of Islamic Financial Management with Behavior of Financial as a Mediation Variable. Proceedings of the 3rd International Conference of Islamic Finance and Business, ICIFEB 2022, 19-20 July 2022, Jakarta, Indonesia. https://doi.org/10.4108/eai.19-7-2022.2328205. [CrossRef]

- Qamar, A., Rasheed, N., Kamal, A., Rauf, S., & Nizam, K. (2023). Factors Affecting Financial Behavior of Millennial Gen Z: Mediating Role of Digital Financial Literacy Integration. International Journal of Social Science & Entrepreneurship. https://doi.org/10.58661/ijsse.v3i3.207. [CrossRef]

- Rodriguez, J. M., Rodriguez, G. A., & Palallos, L. (2024). The Analysis of Financial Planning Activities of Grade-12 Students on their Financial Management in PCU: Basis for Financial Management Plan. International Journal of Research Publications, 153(1), 162–191. https://doi.org/10.47119/IJRP1001531720247007. [CrossRef]

- Shan, L., Cheah, K., & Leong, S. (2023). Leading Generation Z’s Financial Literacy Through Financial Education: Contemporary Bibliometric and Content Analysis in China. SAGE Open. https://doi.org/10.1177/21582440231188308. [CrossRef]

- Shankar, N., Vinod, S., & Kamath, R. (2022). Financial well-being – A Generation Z perspective using a Structural Equation Modeling approach. Investment Management and Financial Innovations. https://doi.org/10.21511/imfi.19(1).2022.03. [CrossRef]

- Ulfa, F., Supramono, S., & Sulistyawati, A. (2023). Influence of Financial Literacy, Risk Tolerance, Financial Efficacy on Investment Decisions and Financial Management Behavior. Kontigensi : Jurnal Ilmiah Manajemen. https://doi.org/10.56457/jimk.v11i2.449. [CrossRef]

- Ulumudiniati, M., & Asandimitra, N. (2022). Pengaruh Financial Literacy, Financial Self-Efficacy, Locus of Control, Parental Income, Love of Money terhadap Financial Management Behavior: Lifestyle sebagai Mediasi. Jurnal Ilmu Manajemen. https://doi.org/10.26740/jim.v10n1.p51-67. [CrossRef]

- Wuisang, J., Rooroh, A., & Christian, W. (2023). The Influence of Financial Literacy and Shopping Habits on The Financial Management of Economic Education Students. International Journal of Accounting & Finance in Asia Pasific. https://doi.org/10.32535/ijafap.v6i2.2317. [CrossRef]

Figure 3.

Q-Q Plot Standardized Residuals.

Table 1.

Correlation Analysis.

| Pearson’s r | p | Decision on Ho | Interpretation | ||||

| FINANCIAL LITERACY | - | SPENDING | 0.821 | < 0.001 | Reject | Significant | |

Table 2.

Direct effects.

| 95% Confidence Interval | ||||||||

| Estimate | Std. Error | z-value | p | Lower | Upper | |||

| FINANCIAL LITERACY | → | SPENDING | 0.642 | 0.044 | 14.536 | < 0.001 | 0.555 | 0.728 |

Table 3.

Indirect effects.

| 95% Confidence Interval | ||||||||||

| Estimate | Std. Error | z-value | p | Lower | Upper | |||||

| FINANCIAL LITERACY | → | FINANCIAL BEHAVIOR | → | SPENDING | 0.180 | 0.033 | 5.401 | < 0.001 | 0.114 | 0.245 |

Table 4.

Total effects.

| 95% Confidence Interval | ||||||||

| Estimate | Std. Error | z-value | p | Lower | Upper | |||

| FINANCIAL LITERACY | → | SPENDING | 0.821 | 0.032 | 25.581 | < 0.001 | 0.758 | 0.884 |

Table 5.

Path coefficients.

| 95% Confidence Interval | ||||||||

| Estimate | Std. Error | z-value | p | Lower | Upper | |||

| FINANCIAL BEHAVIOR | → | SPENDING | 0.249 | 0.044 | 5.648 | < 0.001 | 0.163 | 0.336 |

| FINANCIAL LITERACY | → | SPENDING | 0.642 | 0.044 | 14.536 | < 0.001 | 0.555 | 0.728 |

| FINANCIAL LITERACY | → | FINANCIAL BEHAVIOR | 0.721 | 0.039 | 18.481 | < 0.001 | 0.644 | 0.797 |

Table 6.

R-Model Summary – FINANCIAL BEHAVIOR.

| Model | R | R² | Adjusted R² | RMSE | |||||

| M₀ | 0.000 | 0.000 | 0.000 | 0.553 | |||||

| M₁ | 0.721 | 0.519 | 0.518 | 0.384 | |||||

Note. M₁ includes FINANCIAL LITERACY.

Table 7.

ANOVA.

| Model | Sum of Squares | df | Mean Square | F | p | ||

| M₁ | Regression | 50.115 | 1 | 50.115 | 340.478 | < 0.001 | |

| Residual | 46.365 | 315 | 0.147 | ||||

| Total | 96.479 | 316 | |||||

Note. M₁ includes FINANCIAL LITERACY.

Table 8.

Coefficients.

| Model | Unstandardized | Standard Error | Standardized | t | p | ||||||||

| M₀ | (Intercept) | 3.199 | 0.031 | 103.070 | < 0.001 | ||||||||

| M₁ | (Intercept) | 0.931 | 0.125 | 7.456 | < 0.001 | ||||||||

| FINANCIAL LITERACY | 0.707 | 0.038 | 0.721 | 18.452 | < 0.001 | ||||||||

Table 9.

Descriptive

| Indicator | Minimum | Maximum | Mean | Variance | Skewness | Kurtosis |

| SPEND1 | 1.0000 | 4.0000 | 3.3155 | 0.4192 | -0.6255 | 0.3680 |

| SPEND2 | 1.0000 | 4.0000 | 3.3312 | 0.3488 | -0.3408 | -0.1170 |

| SPEND3 | 1.0000 | 4.0000 | 3.1073 | 0.5581 | -0.4517 | -0.2829 |

| FINLIT1 | 1.0000 | 4.0000 | 3.1073 | 0.5581 | -0.4517 | -0.2829 |

| FINLIT2 | 1.0000 | 4.0000 | 3.3091 | 0.3788 | -0.6336 | 1.1029 |

| FINLIT3 | 1.0000 | 4.0000 | 3.0189 | 0.6958 | -0.5623 | -0.2358 |

| FINBEH1 | 1.0000 | 4.0000 | 3.2366 | 0.4090 | -0.4010 | 0.0126 |

| FINBEH2 | 1.0000 | 4.0000 | 3.1420 | 0.4323 | -0.2923 | -0.1785 |

| FINBEH3 | 1.0000 | 4.0000 | 3.1640 | 0.4603 | -0.3975 | -0.1087 |

Table 10.

Indicator Loadings.

| Indicator | SPENDING | FINANCIAL LITERACY | FINANCIAL BEHAVIOR |

| SPEND1 | 0.5116 | ||

| SPEND2 | 0.5945 | ||

| SPEND3 | 0.7937 | ||

| FINLIT1 | 0.7785 | ||

| FINLIT2 | 0.5507 | ||

| FINLIT3 | 0.5512 | ||

| FINBEH1 | 0.7323 | ||

| FINBEH2 | 0.7517 | ||

| FINBEH3 | 0.6312 |

Table 11.

Convergent Validity.

| Construct | Average variance extracted (AVE) |

| SPENDING | 0.4151 |

| FINANCIAL LITERACY | 0.4044 |

| FINANCIALBEHAVIOR | 0.4999 |

Table 12.

Construct Reliability.

| Construct | Dijkstra-Henseler’s rho (ρA) | Jöreskog’s rho (ρc) | Cronbach’s alpha(α) |

| SPENDING | 0.7031 | 0.6729 | 0.6805 |

| FINANCIAL LITERACY | 0.6899 | 0.6643 | 0.6568 |

| FINANCIAL BEHAVIOR | 0.7539 | 0.7489 | 0.7499 |

Table 13.

Structural Equation Model Table.

| Construct | SPENDING | FINANCIAL LITERACY | FINANCIAL BEHAVIOR |

| SPENDING | 1.0000 | ||

| FINANCIAL LITERACY | 1.1666 | 1.0000 | |

| FINANCIAL BEHAVIOR | 0.7971 | 0.7639 | 1.0000 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.