Submitted:

16 October 2024

Posted:

16 October 2024

You are already at the latest version

Abstract

This study empirically investigates the relationship between realized higher-order moments and the Fear and Greed Index as a measure of sentiments. We estimate daily realized moments for five different sentiment levels using 5-minute return data of the S&P 500 index from January 3, 2011, to September 18, 2020. We found that the Fear and Greed Index significantly impacts realized volatility during periods of extreme fear. Additionally, various sentiment indicators influence realized skewness and realized kurtosis. The VIX index significantly reduces realized skewness across all sentiment levels. Bearish and bullish sentiments have a significant negative relationship with negative realized skewness during periods of extreme fear and extreme greed. Conversely, the Fear and Greed index, bearish and bullish sentiments have a significant positive relationship with positive realized skewness. During extreme fear, the Fear and Greed index, bearish, and bullish sentiments have a significant negative relationship with realized kurtosis. These results remain consistent when considering the non-linear characteristics of the Fear and Greed Index during periods of extreme fear and extreme greed. These findings highlight the relevance of understanding sentiment in financial risk management and its significant relationship with asymmetric and extremity characteristics of asset returns.

Keywords:

Fear and Greed Index

; Realized Higher-Order Moments

; Market sentiment

; Asset Return Distribution

; VIX Index

1. Introduction

Recently, the global financial market has been marked by various turbulent events due to heightened levels of fear and greed among investors see, Albers [1], Yang [2]. These emotions, stemming from behavioural biases, have significantly impacted market dynamics and decision-making processes. For instance, the global financial crisis (2007–2008), the European debt crisis (2009–2010), and the COVID-19 pandemic-induced crash (2020) all highlighted the profound impact of investor sentiment on market outcomes Sarwar [3], Smales [4], Li et al. [5]. During these crises, fear spiked as investors grappled with uncertainty, leading to increased market volatility and risk aversion, while periods of optimism and greed triggered speculative behaviours that further destabilized markets Hollstein et al. [6], Elyasiani et al. [7].

The extant literature has predominantly focused on the relationship between investor sentiment and market returns, emphasizing metrics such as the CBOE Volatility Index (VIX) as a gauge of fear Sarwar [8], Smales [9]. However, these studies often ignore the critical role of higher-order moments such as skewness and kurtosis in capturing the full extent of sentiment-driven market behaviours. These moments are particularly relevant in assessing the asymmetric and extreme events that characterize financial markets during crises Tang and Shum [10], Amaya et al. [11]. Additionally, bullish and bearish sentiments, which represent market optimism and pessimism respectively, play a significant role in shaping investor behaviour and, consequently, market dynamics Smales [12]. While traditional analyses have focused on mean and volatility, the significance of skewness and kurtosis in understanding market dynamics cannot be ignored, particularly in explaining how fear, greed, and overall market sentiment (including bullish and bearish tendencies) influence market asymmetry and extremity Nieto et al. [13], Azimli and Kalmaz [14].

This study seeks to address these gaps by examining the impact of investor sentiment, as measured by the VIX, the CNN Fear-Greed Index, and bullish and bearish sentiment indices, on the realized volatility, realized skewness, and realized kurtosis of S&P 500 equity index. By utilizing high-frequency data, this study provides a granular understanding of how different levels of sentiment (extreme, normal, and neutral) drive market behaviour under varying conditions Elyasiani et al. [7], He and Hamori [15].

The results of this study show that in times of extreme fear, market volatility significantly increases. This is accompanied by a higher frequency of extreme negative returns, leading to more pronounced skewness and kurtosis. Conversely, periods of extreme greed and strong bullish sentiment are associated with increased positive skewness due to the price-driven capacity of investor confidence, resulting in a higher frequency of large positive outliers. When sentiment is neutral or bearish, volatility tends to stabilize volatility and the extremity and asymmetry in returns decreases. These findings offer valuable insights for investors and risk managers, highlighting the importance of accounting for higher-order moments in portfolio strategies, particularly in the context of persistent crises and uncertain market conditions Amaya et al. [11], Ahadzie and Jeyasreedharan [16].

This study contributes to the literature by extending the analysis beyond mean and volatility. It highlights the significant role skewness and kurtosis play in capturing the nuanced impact of investor sentiment on market behaviour. By utilizing indicators such as the VIX, CNN Fear-Greed Index, and sentiment indicators such as bullish and bearish indices, a more comprehensive assessment of how fear, greed, and overall market sentiment impact realized moments is provided. This offers new insights into the behavioural drivers of market dynamics Lo and Zhang [17], Kahneman [18].

The remainder of this study is organized as follows: Section 2 provides a theoretical and empirical review that aims to explain sentiment and realized moment relationships. Section 3 discusses the relevant theory for estimating higher-order moments. Section 4 presents the empirical data, the construction of higher-order moments, and the regression model used in this study. The empirical results are discussed in Section 5, and Section 6 concludes.

2. Literature Review

This section discusses the theories that explain the relationship between fear, greed, and the higher-order moments of equity markets, such as volatility, skewness, and kurtosis. The theoretical framework is grounded in key behavioural finance concepts, including prospect theory Kahneman [18], the optimal belief framework Ali et al. [19], the information asymmetry hypothesis Huang and Wang [20], and the adaptive market hypothesis Lo and Zhang [17]. These theories identify the primary drivers of market sentiment. Following the theoretical discussion, we review empirical studies that investigate the nexus between fear, greed, and market parameters, providing evidence of how these sentiments can be influenced by the mean, variance, and higher-order moments in the stock market.

2.1. Theoretical Review

The relationship between investor sentiments and realized moments of asset returns, specifically volatility, skewness, and kurtosis, can be explained by prospect theory. Prospect theory states that investors assign different weights to gains and losses, leading to deviations from rational expectations Kahneman [18]. Thus, during periods of uncertainty, cognitive biases and sentiments heavily influence investor decisions, resulting in suboptimal responses. Investors often adopt gambling strategies, driven by unrealistic optimism, high expectations, and overconfidence Jin and Zhou [21]. This behaviour manifests in market conditions where fear and greed significantly impact the realized moments, with fear leading to higher volatility and kurtosis, and greed increasing skewness through frequent extreme positive returns.

Similarly, the optimal belief framework developed by Brunnermeier and Parker [22] suggests that investors form beliefs based on a combination of neutral prospects and subjective sentiments. This framework shows that investors approach future utility optimistically, expecting gains due to their preference for skewed returns. Investors inherently hold biased likelihood assessments with imperfectly diversified portfolios, leading to a higher demand for more skewed assets, which typically yield lower returns. Brunnermeier et al. [23] observed over-investment in assets with skewed returns, while Ali et al. [19] noted that higher levels of fear correlate with higher expectations of future volatility. This implies that the attraction towards optimism coupled with poor decisions, drives investors’ preference for skewed equities. Consequently, the anticipation of returns is influenced by other factors, such as skewness and kurtosis, which are relevant in portfolio decision-making. For instance, overly optimistic beliefs based on high levels of greed can inflate asset prices, increasing skewness, while high levels of fear can depress prices, raising volatility and kurtosis.

Additionally, the information asymmetry hypothesis suggests that variations in investor-based news result in market inefficiencies, while the risk-averse nature of investors represents heightened risk levels Huang and Wang [20]. This inconsistency induces anxiety in risk-averse investors with limited evidence, causing them to make irrational choices that further affect levels of fear and greed, increasing asymmetries. Thus, higher fear levels increase asymmetry as investors refrain from trading, increasing volatility and kurtosis. However, extreme greed can mitigate asymmetry as more investors participate in the market and potentially reducing skewness.

The adaptive market hypothesis (AMH) integrates behavioural elements into conventional finance theory, suggesting that market efficiency evolves based on varying circumstances and the personal biases of individual investors. According to the AMH, human behaviour is a complex mix of multiple decision-based systems, with logical reasoning being just one component Lo and Zhang [17]. Through the fight-or-flight mechanism, individual investors respond to varying and extreme risks, influenced by the skewness and kurtosis within the financial market. In this study, this analogy highlights how investors’ fear and greed manifest under neutral or extreme conditions. Aggressive investors driven by greed optimistically respond to extreme market events, seeking higher returns by taking on more risk. However, fearful investors exhibit reserved behaviour during extreme events, recognizing that such situations often lead to significant losses.

Lo and Zhang [17] also argued that when collective wisdom outweighs mob mentality over prolonged periods, market returns reflect the former. However, diverse market conditions can trigger collective fear and greed, with the latter often leading to market bubbles and abrupt crashes. This phenomenon is reflected in the observed skewness and kurtosis in financial markets. We believe that AMH can help explain how investor fear and greed affect realized market moments under varying conditions. It is anticipated that during periods of extreme fear, market efficiency may deteriorate, leading to increased volatility and higher kurtosis. However, during neutral levels of sentiment, the market may exhibit traits closer to efficiency, with more stable volatility and lower skewness and kurtosis.

2.2. Empirical Review

This section discusses the empirical findings on how investor fear and greed may influence the financial market, with a focus on the analysis of mean, volatility, and higher-order moments.

2.2.1. Investor Fear and Greed: Mean & Volatility-Based Analysis

The extant literature documents the nexus between investor sentiment and financial market returns, consistently revealing an inverse pattern despite variations in sentiment metrics. Sarwar [3] found a robust adverse relationship between the peak volatility of the investor fear gauge (VIX) and U.S. equities, with a similar negative influence observed in the BRICS markets. This indicates that the VIX is an effective tool for assessing investor fear in the stock market. Further, Sarwar [8] observed a cross-asset influence of the VIX on U.S. and European equity markets in the post-market crisis period, suggesting market frictions and information processing limitations among European investors. Studies employing stochastic volatility and vector auto-regression models also suggest that fears of impending hurdles increase investor demand for hedges, which, in turn, affects equity returns Soydemir et al. [24], Todorov [25]. Additionally, Kumar and Rao [26] confirmed that the VIX adversely impacts all portfolios in the Indian equity market, with these effects showing persistent shocks. These findings are further supported by Shaikh and Padhi [27], who demonstrated that the VIX is a robust measure of investor fear in the Indian market, and by Smales [4], who found that increases in investor fear led to declining returns in the Australian equities, bonds, and currency markets.

Economou et al. [28] examined the relationship between equities in the U.S., U.K., and Germany and their respective VIX indices, finding an asymmetric reaction in the U.S. market. Sarwar and Khan [29] demonstrated that the VIX has an adverse predictive capacity on equities in emerging markets, with VIX shocks explaining a significant portion of equity variations. Chakraborty and Subramaniam [30] concluded that lower sentiment drives fear-based trading, leading to lower future returns, while Graham et al. [31] provided additional insights using web-based fear metrics. Studies conducted during the COVID-19 pandemic revealed that pandemic-related fear significantly impacted global equities. For instance, Li et al. [5] identified pandemic-based fear as a primary predictor of investor attention and volatility, and Duong et al. [32] showed the persistence of volatility in the Vietnam equity markets due to pandemic-induced fear. These findings highlight that volatility and fear from major markets, particularly the U.S., are significant drivers of global equity market volatility, with pronounced effects during crises Smales [9], Grima et al. [33], Narang et al. [34], Cupák et al. [35], Adekoya et al. [36].

2.2.2. Investor Fear & Greed and Higher-Order Moments

Given the dominance of risk and return-based analysis and the quest to validate the relevance of higher-order moments, Tang and Shum [10] examined the usefulness of global equity risk measures, particularly focusing on beta, skewness, and kurtosis under varying market conditions. Their study demonstrated that investors are compensated not only for systematic risk but also for unsystematic risk, indicating a preference for undiversified portfolios. It was found that investors tend to accept lower positive returns for positively skewed portfolios, with total risk positively related to realized returns in favourable conditions and negatively related in unfavorable conditions. Extending this work, Westerhoff [37] developed a behavioural stock market model driven by fear and greed, where optimistic beliefs lead to stock purchases and panic results in selling, causing alternating periods of low and high volatility.

Nieto et al. [13] showed that the variance risk premium responds to changes in the higher-order moments of market returns, linking investor fear with various economic and financial risk factors. In another study, Amaya et al. [11] analyzed weekly data from over 2,000 equity firms, finding that realized volatility decreases while skewness and kurtosis increase during periods of cross-sectional dispersion, indicating an inverse relationship between realized volatility and skewness. Meanwhile, Hollstein et al. [6] identified a highly integrated tail risk among emerging and developed markets, demonstrating the predictive power of the tail risk index in these markets.

Addressing limitations in the VIX, Elyasiani et al. [7] developed an Italian equity-based skewness index, which more accurately captures investor excitement (greed) than fear. Azimli and Kalmaz [14] found a link between RU-GPR and realized volatility, noting significant correlations in realized skewness and kurtosis across different markets. Additionally, Banerjee et al. [38] assessed the spillovers of higher moments between Shanghai International Energy and U.S. energy futures, highlighting substantial transmission during the pandemic and recent conflicts, underscoring the importance of higher-order moments in financial risk management.

Table 1 provides a comprehensive summary of the relationship between different sentiment levels ranging from Extreme Fear to Extreme Greed, and the observed volatility, skewness, and kurtosis in financial markets, based on both theoretical and empirical reviews.

The table shows that sentiment-driven emotions, particularly fear and greed, significantly influence market dynamics. During periods of Extreme Fear, volatility, negative skewness, and kurtosis are significantly heightened, reflecting an increase in uncertainty and adverse investor reactions. This period also shows a significant decrease in positive skewness, indicating a high frequency of extreme negative returns and market downturns. In states of Fear, volatility, negative skewness and kurtosis still increase, while positive skewness decreases. When sentiment is Neutral, the market shows stable or slightly decreasing volatility, with skewness and kurtosis also remaining stable or showing minor changes. This reflects balanced market conditions, with no strong bias toward either fear or greed, resulting in fewer extreme fluctuations. Conversely, during periods of Greed, volatility either slightly increases or remains stable, while negative skewness decreases and positive skewness increases. This shift reflects a market where investors are generally optimistic, often engaging in speculative behaviour that drives the frequency of extreme positive returns, with a minimal or stabilizing impact on overall volatility. In situations of Extreme Greed, volatility may slightly decrease or remain stable, negative skewness decreases further, and positive skewness increases significantly. Kurtosis remains stable or slightly increases, suggesting fewer extreme negative returns and a prevalence of positive outliers. Understanding these dynamics provides valuable insights into how fear and greed influence investor behaviour and market outcomes, revealing underlying emotional drivers that traditional risk measures might ignore.

2.3. Gaps in the Literature

This study contributes to the literature by investigating the relationship between investor sentiments, specifically fear and greed, and higher-order moments of asset returns, namely asymmetry (realized skewness) and extremity (realized kurtosis). Unlike previous studies that primarily focused on mean and volatility, our study emphasizes the importance of skewness and kurtosis in capturing the nuanced impacts of investor sentiments on market behaviour Tang and Shum [10], Amaya et al. [11], Hu and McInish [39]. By using high-frequency data, we capture relevant information that would otherwise have been ignored, providing a more granular understanding of how sentiments influence market dynamics Elyasiani et al. [7], He and Hamori [15].

Our approach diverges from prior research that predominantly focused on the VIX as a fear indicator, we employ the CNN Fear-Greed Index which allows us to capture both fear and greed. This approach shows that different sentiments have varying responses from market participants, especially during periods of significant stress Erdemlioglu and Gradojevic [40], John and Li [41]. By examining how extreme, normal, and neutral levels of fear and greed drive the realized volatility, skewness, and kurtosis of the S&P 500 index, this study provides comprehensive insights into the behavioural underpinnings of market movements Shaikh and Padhi [27], Dilmac et al. [42]. The results offer valuable insights for investors by highlighting how varying sentiments influence market asymmetry and extremity under different market conditions, thus advancing the understanding of investor decision-making in the presence of persistent crises and uncertainties Hollstein et al. [6], Adekoya et al. [36], Balcilar et al. [43].

3. Higher-Order Realized Moments

In this section, we discuss the theoretical framework for estimating realized higher-order moments. Suppose the observed price follows a semi-martingale process on a filtered probability space (, , , ) within a frictionless market where there is no arbitrage opportunities (see Back [44]). When accounting for jumps, the observed price can be described by a continuous-time semi-martingale jump-diffusion process:

where is the diffusive mean, denotes the diffusive volatility process, is the increments of a Brownian motion , is a counting process, and are the non-zero jump increments (see Fleming and Paye [45] for further details). The quadratic variation for the jump-diffusion process is defined as:

The first term on the right-hand side of Equation 2 is the integrated variance, and the second term is the sum of the squared jumps (variance of the jump component). In the absence of jumps, Equation 2 simplifies to a pure diffusion model with continuous sample paths, as the jump component becomes zero. For this jump-diffusion process, it is assumed that and are jointly independent of . The integrated variance (IV) for this process is defined as , equating to the quadratic variance (QV).

In high-frequency finance, realized variance (RV) is employed as a proxy for sample variance, replacing the traditional use of squared returns at low frequencies. It is well-documented that realized variance is a more robust estimator of volatility (see Andersen and Bollerslev [46], Andersen et al. [47], Hansen and Lunde [48], Hansen and Lunde [49], Barndorff-Nielsen and Shephard [50], Andersen et al. [51]). The discrete-time high-frequency returns over the holding-interval h is defined as:

where h is the holding-interval (trading day), is the i-th high-frequency log price for the holding-interval h, and N is the number of infill observations for each sampling-interval , partitioned into equal lengths such that and . The RV is defined as the sum of squared high-frequency returns:

The RV is an efficient estimator of the quadratic variation, converging to the QV as the number of observations (N) approaches infinity ( as ; see Andersen and Bollerslev [46], Barndorff-Nielsen and Shephard [52]). Notably, in the absence of jumps, RV converges to IV.

Following Amaya et al. [11], Ahadzie and Jeyasreedharan [53], and Ahadzie and Jeyasreedharan [54], the third and fourth realized moments are defined as:

According to Amaya et al. [11], the third realized moment converges to the sum of cubic jumps, and the fourth realized moment converges to the sum of quartic jumps. This implies that the realized third higher-order moment captures the sum of cubic jumps, while the realized fourth higher-order moment captures the sum of quartic jumps. For , only the magnitude of the jumps is relevant, not their direction. These jump-driven convergences align with the findings of Kim and White [55], who demonstrated that estimates of higher moments of high-frequency data distributions are significantly influenced by the presence of jumps.

Following Amaya et al. [11], Ahadzie and Jeyasreedharan [53], Ahadzie and Jeyasreedharan [54], RS is defined as the cubic intra-day returns normalized by the square root of RV cubed, and RK is the sum of the quartic high-frequency returns normalized by RV squared:

For negative realized skewness () and positive realized skewness (), the definitions are:

Amaya et al. [11] showed that realized skewness and realized kurtosis do not converge to the sample skewness and sample kurtosis. The sample skewness and kurtosis include diffusive skewness and diffusive kurtosis components. Thus, the normalized third realized moment (realized skewness) captures the normalized direction and magnitude of the cubic jumps, while the normalized fourth realized moment (realized kurtosis) captures the normalized magnitude of the quartic jumps. Consequently, the information contained in realized skewness and realized kurtosis differs from that of sample skewness and sample kurtosis, typically computed from long samples of low-frequency return data (e.g., daily, weekly, or monthly return series).

4. Data and Methodology

In high-frequency literature, it is common to use returns sampled at a 5-minute frequency as a proxy for unbiased high-frequency return data in the U.S. market Andersen et al. [51], Andersen and Bollerslev [56], Huang and Tauchen [57]. This approach balances microstructure noise and variance bias. According to Bandi and Russell [58], it is important to compute realized variance with unbiased intra-day return data, as using contaminated return data can significantly accumulate noise, resulting in biased estimates. Therefore, this study uses 5-minute last-traded prices of the S&P 500 index.

The high-frequency data was obtained from the DataScope Refinitiv database, covering the period from January 3, 2011, to September 18, 2020, and includes trading days between 9:30 am and 4 pm. This results in a sample of 78 intra-day prices per day. We exclude weekends and overnight returns from the data. Intra-day returns were computed as the change in the logarithm of the closing prices of successive days. Daily realized moments were computed from the 5-minute high-frequency returns data, yielding 2,535 daily observations. Daily data for the US stock market volatility index (VIX Index) were downloaded directly from the CBOE website1. The US AAII investor sentiment survey data for bearish and bullish sentiments and the US dollar index (USDX) were downloaded from DataStream, while the Fear and Greed index was downloaded from Medium2.

Table 2 reports the relationship between various sentiment levels (extreme fear, fear, neutral, greed, and extreme greed) and the dependent variables; realized volatility, realized skewness, negative realized skewness, positive realized skewness, and realized kurtosis. Using ANOVA and Bartlett’s tests, we test whether these variables’ means and variances differ significantly across sentiment levels.

The Hypotheses for ANOVA is defined as follows:

Null Hypothesis (H0): The means of the variable are equal across the different sentiment levels.

Alternative Hypothesis (H1): At least one of the means of the variable is different across the sentiment levels.

The Hypotheses for Bartlett’s Test is defined as follows:

Null Hypothesis (H0): The variances of the variable are equal across the different sentiment levels.

Alternative Hypothesis (H1): At least one of the variances of the variable is different across the sentiment levels.

The ANOVA results show significant differences in the means of each variable across sentiment levels, indicated by F-statistics and corresponding significant p-values. For instance, realized volatility shows an F-statistic of 17.300 (p-value = 0.000), realized skewness an F-statistic of 24.070 (p-value = 0.000), positive realized skewness an F-statistic of 25.440 (p-value = 0.000), negative realized skewness an F-statistic of 5.860 (p-value = 0.000), and realized kurtosis an F-statistic of 22.260 (p-value = 0.000). We reject the null hypothesis that the means of the variables are equal across sentiment levels, this suggests that fear and greed sentiment significantly impact realized moments.

Moreover, Bartlett’s tests show unequal variances across sentiment levels for all variables, as evidenced by chi-square statistics and significant p-values as well. Specifically, realized volatility has a chi-square value of 34.769 (p-value = 0.000), realized skewness a chi-square value of 268.447 (p-value = 0.000), positive realized skewness a chi-square value of 370.080 (p-value = 0.000), negative realized skewness a chi-square value of 32.461 (p-value = 0.000), and realized kurtosis a chi-square value of 379.005 (p-value = 0.000). We reject the null hypothesis of equal variances, implying significant heteroscedasticity.

The relevance of these results shows the influence of fear and greed sentiment on market behaviour, which aligns with the findings presented in Table 1. For example, higher sentiment levels such as extreme greed is associated with higher realized kurtosis, indicating more extreme returns. This variability and extremity in returns can significantly affect risk management and investment strategies. The rejection of the null hypothesis for both tests across all dependent variables suggests the need for financial models to account for sentiment-driven market dynamics, as these psychological factors can lead to significant deviations from traditional risk and return expectations. Hence, the results empirically support investigating fear and greed-driven realized moment relationships.

To investigate the relationships between realized moments and the Fear and Greed index, we estimate Equation 10 using the following quantile regression:

where the subscript t denotes time (t = 1,...,T), represents the quantile level, and is the error term. RM represents the realized moment (i.e., realized volatility (RV), realized skewness (RS), negative realized skewness (), positive realized skewness (), and realized kurtosis (RK)). X is a vector of predictors, including the Fear and Greed index (FGI), US dollar index (USDX), bearish and bullish sentiments, and return data. The coefficients and are estimated for each quantile .

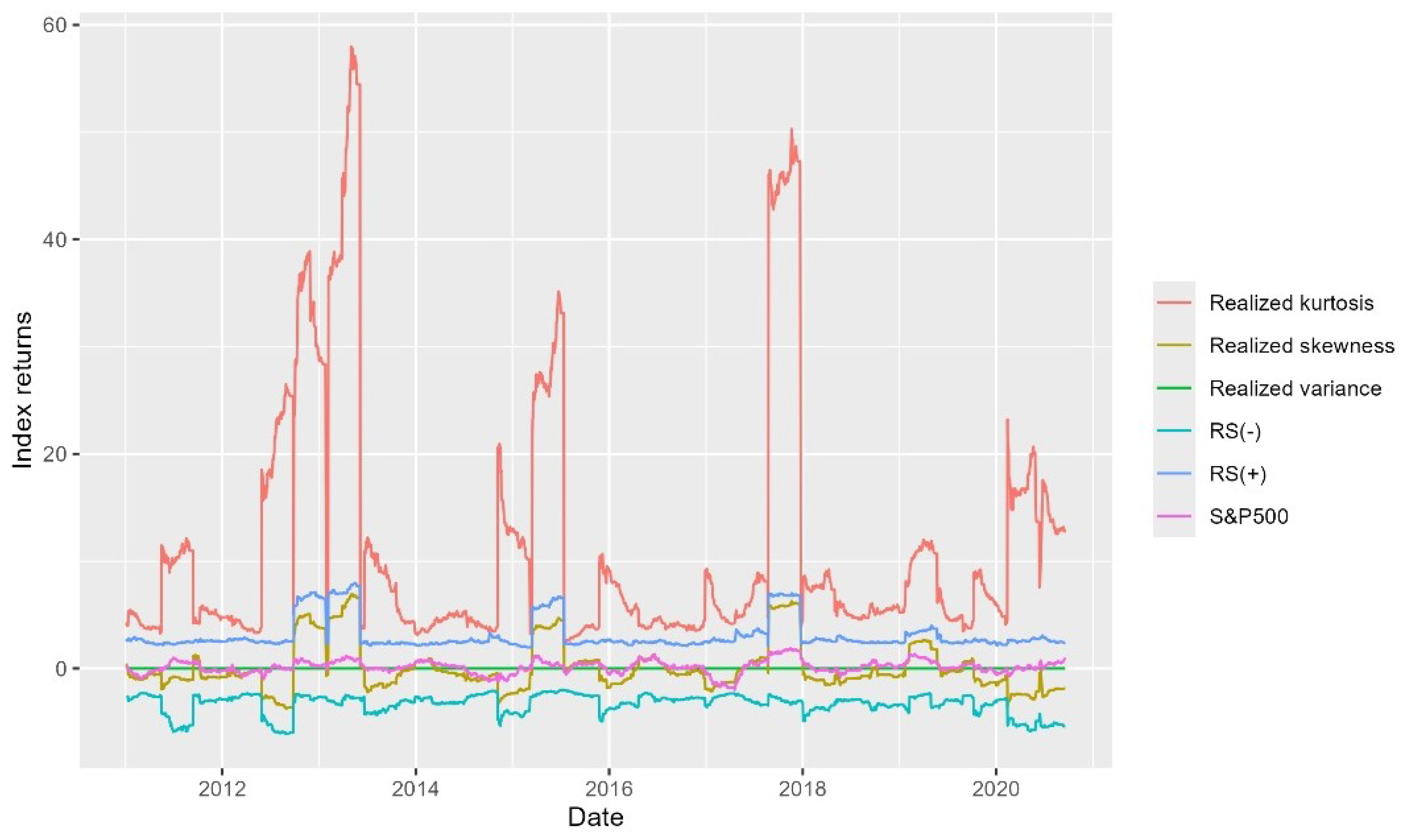

Figure 1 shows how higher-order moments, such as realized variance, realized skewness, and realized kurtosis, provide insights into the behaviour of financial markets, specifically the S&P 500 returns. We observe that realized kurtosis has sharp fluctuations, which indicates market stress. These fluctuations often coincide with extreme events or periods of heightened uncertainty, which can precede significant market movements. Realized skewness and its components, negative skewness and positive skewness, offer valuable perspectives on market sentiment. Negative skewness moves with the bearish sentiment, suggesting a tendency toward negative returns, while positive skewness indicates bullish sentiment, pointing to positive return tendencies. Lastly, realized variance is closely linked to market volatility.

5. Results

5.1. Fear and Greed-Realized Moment Relationship

In this section, we investigate the empirical relationship between realized moments and the Fear and Greed Index while controlling for other market sentiment indicators. Table 3 reports the quantile regression results across different sentiment levels and provides the relationships between various predictors and realized volatility.

At the extreme fear sentiment level, the results show significant relationships between several predictors. We note that the FGI index has a significant negative coefficient of -4.5E-07 at the 1% significance level, indicating that increased fear reduces realized volatility. This finding contrasts with the general understanding that fear typically increases volatility, suggesting a unique dynamic in extreme fear conditions. Typically, fear is associated with increased volatility as investors react to uncertainty and potential losses, leading to more volatile market conditions (see Smales [12], Whaley [59]). However, the unique dynamic relationship observed in the extreme fear conditions suggests that in rare scenarios, heightened fear may lead to more cautious behaviour and reduced volatility contrasting the typical reaction to fear. The USDX has a positive and significant coefficient of 3.06E-07 at the 1% significance level, suggesting that an increase in USDX increases realized volatility, likely due to increased market uncertainty, as suggested by Ehrmann et al. [60]. The VIX index has a significant positive coefficient of 3.04E-07 at the 1% significance level, indicating that higher market volatility (as measured by VIX) tends to increase realized volatility, consistent with studies Grima et al. [33], Whaley [59], Da et al. [61], Szczygielski et al. [62], who identified VIX as a reliable measure of market sentiment and volatility. The return variable has a significant negative coefficient of -2.3E-06 at the 1% significance level, suggesting that higher returns decrease realized volatility, contrasting with the general finding by studies Duong et al. [32], Narang et al. [34], Andersen et al. [63], Vasileiou [64], that noted that higher returns are usually associated with higher volatility due to increased speculative trading. The bearish and bullish sentiments are insignificant at this sentiment level, indicating that extreme fear sentiment may overshadow other sentiment influences.

For the fear sentiment level, the FGI index has a positive and significant coefficient of 2.01E-07 at the 5% significance level, indicating that increased fear is associated with increased realized volatility. The USDX has a positive but not statistically significant relationship with a coefficient of 1.01E-07. The bearish and bullish sentiments, the VIX, and return variables are insignificant in this quantile.

The FGI index is insignificant in the neutral sentiment level, with a coefficient of -1.5E-09. The USDX has a significant positive relationship with a coefficient of 7.54E-07 at the 1% significance level. The VIX index also shows a significant positive coefficient of 5.85E-07 at the 5% significance level, reinforcing the importance of market volatility in influencing realized volatility. The bearish sentiment, bullish sentiment, and return variables are insignificant in this sentiment level, suggesting a more stable market condition where these factors are less impactful.

At the greed sentiment level, the FGI index has a positive but insignificant coefficient of 5.12E-08. The USDX has a negative but insignificant relationship with a coefficient of -4.8E-08. The bearish sentiment has a significant negative coefficient of -8.9E-07 at the 5% significance level, indicating that increased bearish sentiment reduces realized volatility. This contrasts with the findings of Brown and Cliff [65], who note that bearish sentiment often increases volatility, likely due to panic selling and market pessimism. The VIX index has a significant negative coefficient of -5.1E-07 at the 1% significance level, suggesting that higher market volatility decreases realized volatility, which may appear contradictory but could indicate market stabilization mechanisms during greed sentiment periods. The return variable shows a significant positive relationship with realized volatility, with a coefficient of 9.01E-06 at the 1% significance level, aligning with the general understanding that higher returns can increase market activity and volatility, as noted by studies Narang et al. [34], Andersen et al. [63], Vasileiou [64].

For the extreme greed sentiment level, the FGI index has a positive but insignificant coefficient of 9.17E-08. The USDX has a positive but insignificant relationship with a coefficient of 7.79E-08. The VIX index shows a significant negative coefficient of -6.4E-07 at the 1% significance level, indicating that higher market volatility decreases realized volatility, which may reflect a market correction mechanism during extreme greed periods. The return variable has a significant positive coefficient of 7.21E-06 at the 5% significance level, suggesting that higher returns increase realized volatility. The bearish and bullish sentiments are insignificant at this sentiment level, implying that during extreme greed, other factors like market volatility and returns have more pronounced effects.

The results show how different economic indicators and sentiment indices uniquely influence realized volatility across various sentiment levels. The FGI index and sentiments significantly impact volatility during periods of extreme fear and fear, indicating investor sentiment strongly influences market behaviour. The USDX affects volatility during extreme fear and neutral sentiment levels, highlighting its critical role in market uncertainty. The VIX index consistently impacts volatility across sentiment levels, showing the importance of market volatility in shaping realized volatility. The return variable’s persistent relationship with volatility during extreme fear, greed, and extreme greed highlights its ongoing impact on market dynamics. These insights provide a deeper understanding of how various factors shape market behaviour in response to various sentiments.

Table 4 reports the quantile regression results across different sentiment levels and provides insights into the relationships between various predictors and realized skewness.

At the extreme fear sentiment level, we note that the FGI index has a positive and insignificant coefficient of 6.99E-05. The USDX has a positive and significant coefficient of 0.011 at the 1% significance level, suggesting that an increase in USDX increases realized skewness. The bearish sentiment has a significant negative coefficient of -0.056 at the 1% significance level, indicating that increased bearish sentiment reduces realized skewness. The VIX index has a significant negative coefficient of -0.030 at the 1% significance level, indicating that higher market volatility reduces realized skewness, consistent with the role of VIX as a fear gauge Whaley [59]. The return variable has a significant positive coefficient of 1.724 at the 1% significance level, suggesting that higher returns increase realized skewness. This contradicts the findings of [11], who revealed that assets with less (more) skewness are compensated with higher (lower) returns.

For the fear sentiment level, the FGI index has a negative and insignificant coefficient of -4.93E-04. The USDX has a positive but insignificant relationship with a coefficient of 0.004. The bearish sentiment has a negative coefficient of -0.025, which is insignificant. The bullish sentiment shows a positive coefficient of 0.028 at 10% significance level. The VIX index has a significant negative coefficient of -0.058 at the 1% significance level. The return variable shows a significant positive relationship with realized skewness, with a coefficient of 1.190 at the 1% significance level, supporting the relationship between returns and skewness as observed in broader market dynamics (see Boyer and Vorkink [66]).

In the neutral sentiment level, the FGI index is insignificant, with a coefficient of -0.005. The USDX has a positive but insignificant relationship with a coefficient of 0.001. The bearish sentiment has a significant positive coefficient of 0.079 at the 1% significance level, and the bullish sentiment also shows a significant positive coefficient of 0.071 at the 1% significance level. The VIX index has a significant negative coefficient of -0.083 at the 1% significance level. The return variable shows a significant positive relationship with realized skewness, with a coefficient of 1.684 at the 1% significance level.

At the greed sentiment level, the FGI index has a negative but insignificant coefficient of -0.022. The USDX has a significant negative relationship with a coefficient of -0.070 at the 1% significance level. The bearish sentiment has a significant negative coefficient of -0.072 at the 5% significance level, indicating that increased bearish sentiment reduces realized skewness. The VIX index has a significant negative coefficient of -0.031 at the 5% significance level. The return variable shows a significant positive relationship with realized skewness, with a coefficient of 3.312 at the 1% significance level.

For the extreme greed sentiment level, the FGI index has a negative but insignificant coefficient of -0.041. The USDX has a significant negative relationship with a coefficient of -0.189 at the 1% significance level. The bearish sentiment has a significant negative coefficient of -0.543 at the 1% significance level, indicating that increased bearish sentiment reduces realized skewness. The bullish sentiment also shows a significant negative coefficient of -0.183 at the 1% significance level. The VIX index has a significant negative coefficient of -0.055 at the 1% significance level. The return variable has a significant positive coefficient of 1.786 at the 1% significance level.

The results show that the VIX consistently reduces realized skewness across sentiment levels, highlighting its stabilizing role during market volatility. Bearish sentiment lowers skewness, especially during extreme greed, while USDX increases skewness under extreme fear but decreases it during extreme greed. Higher returns consistently increase realized skewness, suggesting asymmetry in positive returns.

In Table 5, we report the quantile regression results across different sentiment levels and discuss the relationships between various predictors and negative realized skewness.

At the extreme fear sentiment level, we observe that the FGI index has a negative coefficient of -0.002, but it is insignificant. The USDX has a positive and significant coefficient of 0.025 at the 1% significance level, suggesting that an increase in USDX increases negative realized skewness. The bearish sentiment has a significant negative coefficient of -0.074 at the 1% significance level, indicating that increased bearish sentiment reduces negative realized skewness. The VIX index has a significant negative coefficient of -0.056 at the 1% significance level, indicating that higher market volatility reduces negative realized skewness. The return variable has a significant positive coefficient of 0.272 at the 1% significance level, suggesting that higher returns increase negative realized skewness, which aligns with the concept that higher returns can lead to increased asymmetry in the distribution of returns (see Boyer et al. [67]).

For the fear sentiment level, the FGI index has a positive coefficient of 0.010, but it is insignificant. The USDX has a negative but insignificant relationship with a coefficient of -0.004. The bearish sentiment has a positive coefficient of 0.019, which is insignificant. The bullish sentiment shows a positive coefficient of 0.031, which is also insignificant. The VIX index has a significant negative coefficient of -0.121 at the 1% significance level. The return variable shows a significant negative relationship with negative realized skewness, with a coefficient of -0.368 at the 5% significance level.

In the neutral sentiment level, the FGI index is insignificant, with a coefficient of -0.012. The USDX has a negative but insignificant relationship with a coefficient of -0.004. The bearish sentiment has a significant positive coefficient of 0.037 at the 5% significance level, and the bullish sentiment also shows a significant positive coefficient of 0.029 at the 5% significance level. The VIX index has a significant negative coefficient of -0.094 at the 1% significance level. The return variable is insignificant.

At the greed sentiment level, the FGI index has a negative but insignificant coefficient of -0.004. The USDX has a significant positive relationship with a coefficient of 0.009 at the 1% significance level. The bearish sentiment has a negative coefficient of -0.009 at a 10% significance level. The bullish sentiment has a significant negative coefficient of -0.024 at the 1% significance level. The VIX index has a significant negative coefficient of -0.015 at the 1% significance level. The return variable is insignificant.

For the extreme greed sentiment level, the FGI index has a negative but insignificant coefficient of -0.003. The USDX has a significant positive relationship with a coefficient of 0.005 at the 1% significance level. The bearish sentiment has a significant negative coefficient of -0.015 at the 1% significance level, indicating that increased bearish sentiment reduces negative realized skewness. The bullish sentiment also shows a significant negative coefficient of -0.039 at the 1% significance level. The VIX index has a significant negative coefficient of -0.012 at the 1% significance level. The return variable has a significant negative coefficient of -0.077 at the 1% significance level, suggesting that higher returns reduce negative realized skewness.

The findings show that VIX consistently reduces negative realized skewness, mitigating downside risk during extreme fear and greed. Additionally, bearish and bullish sentiments reduce negative skewness during extreme fear and greed. This reflects a potential market correction mechanism, where extreme optimism is tempered by sentiment dynamics.

Table 6 reports the quantile regression results across different sentiment levels and discusses the relationships between various predictors and positive realized skewness.

At the extreme fear sentiment level, we note that the FGI index has a negative and significant coefficient of -0.005 at the 1% significance level, indicating that increased fear reduces positive realized skewness. The USDX has a positive but insignificant coefficient of 0.001. The bearish sentiment has a significant positive coefficient of 0.008 at the 1% significance level, and the bullish sentiment also shows a significant positive coefficient of 0.007 at the 1% significance level. This suggests that both bearish and bullish sentiments increase positive realized skewness. The VIX index is insignificant, while the return variable has a significant negative coefficient of -0.081 at the 1% significance level, indicating that higher returns reduce positive realized skewness.

For the fear sentiment level, the FGI index has a positive and significant coefficient of 0.004 at the 5% significance level. The USDX has a positive and significant relationship with a coefficient of 0.004 at the 1% significance level. Both the bearish and bullish sentiments exhibit significant positive coefficients of 0.010 and 0.004 at the 1% and 5% significance levels, respectively. The VIX index has a significant positive coefficient of 0.004 at the 5% significance level, indicating that higher market volatility increases positive realized skewness. The return variable shows a significant negative relationship with positive realized skewness, with a coefficient of -0.037 at the 1% significance level.

The FGI index is insignificant in the neutral sentiment level, with a coefficient of 0.007. The USDX has a positive but insignificant relationship with a coefficient of 0.008. The bearish sentiment has a positive coefficient of 0.015, which is insignificant. The bullish sentiment shows a positive coefficient of 0.021 at 10% significance level. The VIX index is insignificant, and the return variable is also insignificant. These results suggest that during neutral sentiment periods, the predictors do insignificantly impact positive realized skewness.

At the greed sentiment level, the FGI index has a negative but insignificant coefficient of -0.036. The USDX has a significant negative relationship with a coefficient of -0.058 at the 1% significance level. The bearish sentiment has a negative but insignificant coefficient of -0.057, and the bullish sentiment is insignificant. The VIX index has a negative but insignificant coefficient of -0.019. The return variable shows a significant positive relationship with positive realized skewness, with a coefficient of 1.471 at the 1% significance level, suggesting that higher returns increase positive realized skewness. This is supported by findings from Conrad et al. [68] on the relationship between returns and skewness.

For the extreme greed sentiment level, the FGI index has a negative but insignificant coefficient of -0.019. The USDX has a significant negative relationship with a coefficient of -0.181 at the 1% significance level. The bearish sentiment has a significant negative coefficient of -0.531 at the 1% significance level, indicating that increased bearish sentiment reduces positive realized skewness. The bullish sentiment also shows a significant negative coefficient of -0.220 at the 1% significance level. The VIX index has a significant negative coefficient of -0.036 at the 1% significance level. The return variable has a significant positive coefficient of 0.625 at the 1% significance level, suggesting that higher returns increase positive realized skewness.

The results show the asymmetry effects of bearish and bullish sentiments on positive realized skewness across sentiment levels. While both sentiments significantly increase positive realized skewness during periods of extreme fear and fear, they exhibit a negative effect during periods of extreme greed, where both bearish and bullish sentiments reduce positive realized skewness. This suggests that during periods of heightened market fear, investors’ actions driven by both negative and positive sentiment contribute to an increase in positive skewness, while in times of extreme greed, these sentiments suppress positive skewness, reflecting different market dynamics under varying emotional extremes.

Table 7 reports the quantile regression results across different sentiment levels and provides critical insights into the relationships between various predictors and realized kurtosis.

At the extreme fear sentiment level, we note that the FGI index has a significant negative coefficient of -0.051 at the 1% significance level, indicating that increased fear reduces the extremeness of return distributions. This is consistent with findings by Baker and Wurgler [69] who show that investor sentiment significantly impacts market returns and their distributions. The USDX has a positive and significant coefficient of 0.022 at the 5% significance level, suggesting that a stronger USDX increases realized kurtosis, likely due to increased market uncertainty. This finding is supported by Ehrmann et al. [60], who explore the international financial transmission mechanisms and suggest that fluctuations in the US DOLLAR can significantly affect market conditions and uncertainty. In the cases of bearish and bullish sentiments, we observe significant positive coefficients of 0.119 and 0.112 at the 1% significance level, respectively, indicating that these sentiments contribute to higher realized kurtosis. The VIX index has a significant negative coefficient of -0.045 at the 1% significance level, suggesting that higher market volatility tends to reduce realized kurtosis. Andersen et al. [63] provide evidence of the impact of volatility on the return distribution’s higher moments, which is consistent with this finding. The return variable has a significant positive coefficient of 0.333 at the 5% significance level, indicating that returns increase the extremeness of the distribution during extreme fear.

For the fear sentiment level, the FGI index has a positive but not statistically significant coefficient of 0.010. The USDX has a significant positive relationship with a coefficient of 0.036 at the 1% significance level. Both the bearish and bullish sentiments exhibit significant positive coefficients of 0.041 and 0.062 at the 5% and 1% significance levels, respectively, suggesting that these sentiments increase realized kurtosis. The VIX index is insignificant in this quantile. The return variable shows a significant positive relationship with realized kurtosis, with a coefficient of 0.394 at the 1% significance level.

In the neutral sentiment level, the FGI index is insignificant, with a coefficient of -0.133. Similarly, the USDX is insignificant. The bearish sentiment has a negative coefficient of -0.388 and the bullish sentiment has a negative coefficient of -0.283, both not statistically significant. The VIX index shows a significant positive coefficient of 0.357 at the 1% significance level, indicating that market volatility increases realized kurtosis. The return variable is insignificant.

At the greed sentiment level, the FGI index has a negative but insignificant coefficient of -0.244. The USDX has a significant negative relationship with a coefficient of -0.607 at the 1% significance level. The bearish sentiment has a significant negative coefficient of -0.982 at the 5% significance level, indicating that increased bearish sentiment reduces realized kurtosis. The bullish sentiment and VIX are insignificant. The return variable shows a significant positive relationship with realized kurtosis, with a coefficient of 11.558 at the 1% significance level.

For the extreme greed sentiment level, the FGI index has a negative and insignificant coefficient of -0.172. The USDX has a highly significant negative relationship with realized kurtosis, with a coefficient of -1.314 at the 1% significance level. The bearish sentiment has a significant negative coefficient of -4.075, and the bullish sentiment also shows a significant negative coefficient of -1.602 at the 1% significance level, respectively. The VIX index shows a significant negative coefficient of -0.287 at the 5% significance level, indicating that higher market volatility reduces realized kurtosis. The return variable has a significant positive coefficient of 7.629 at the 1% significance level, suggesting that returns increase the extremeness of the distribution during extreme greed.

In summary, the results show how different sentiment indices uniquely influence realized kurtosis across various conditions. During periods of extreme fear and fear, the FGI index and sentiments (bearish and bullish) significantly impact realized kurtosis, indicating changes in the extremeness of return distributions. The USDX has a significant effect, particularly during extreme fear and extreme greed, highlighting its crucial role in market uncertainty. The VIX index consistently influences kurtosis across sentiment levels, this highlights the importance of market volatility in shaping return distributions. The return variable maintains a significant positive relationship with realized kurtosis, emphasizing its persistent impact on return extremeness across different sentiment conditions. The results suggest that understanding the influence of investor sentiment on return distributions leads to more precise risk assessments and enhances the accuracy of predictive models.

5.2. Robustness Test: Quantile Regressions with Non-Linear Effects

In Table 8, we report the result for the quantile regressions with non-linear effects of Fear and Greed Index (FGI) during periods of extreme fear and extreme greed. The analysis focuses on realized volatility (RV), realized skewness (RS), negative realized skewness (RS(-)), positive realized skewness (RS(+)), and realized kurtosis (RK) as the dependent variables. The non-linear effect is captured by including the squared term of the FGI in the regression model of Equation 10.

For the extreme fear sentiment level, with realized volatility as the dependent variable, we observe that the coefficients of FGI and its squared term are statistically insignificant. This indicates that the non-linear effects of FGI do not impact realized volatility under extreme fear conditions. The USDX index, has a positive and significant effect at the 1% level, suggesting that a stronger USDX index increases realized volatility, consistent with the results discussed in Table 3. The bearish and bullish indices have a positive but insignificant relationship with realized volatility. The VIX index shows a positive and significant relationship with realized volatility at the 1% level, indicating that higher market volatility increases realized volatility. The return variable has a significant negative coefficient, suggesting that higher levels of return tend to reduce realized volatility, possibly due to the stabilizing effect of high returns on market expectations.

For the extreme greed sentiment level, with realized volatility as the dependent variable, the coefficients for the FGI and its squared term are insignificant. This suggests that the non-linear effects of FGI do not impact realized volatility under extreme greed conditions. The USDX index is also insignificant. The bearish and bullish indices have a negative but insignificant relationship with realized volatility. The VIX index has a significant negative coefficient, suggesting that higher market volatility decreases realized volatility during extreme greed. This finding shows the unique market reaction to volatility in periods of extreme fear and extreme greed. The return variable shows a significant positive relationship, indicating that higher returns increase realized volatility.

With realized skewness as the dependent variable under extreme fear, the FGI and its squared term are insignificant. However, the USDX index is positively significant, suggesting that a stronger USDX index increases realized skewness. Bearish sentiment has a significant negative effect, indicating that increased bearish sentiment reduces realized skewness. The bullish index, on the other hand, has a negative but insignificant relationship with realized skewness. The VIX index shows a negative and significant relationship, indicating that higher market volatility reduces realized skewness. The return variable has a significant positive relationship with realized skewness, indicating that higher returns increase realized skewness.

For realized skewness under extreme greed, the FGI and its squared term are insignificant. The USDX index is significant and negative, indicating that a stronger USDX index decreases realized skewness. Both bearish and bullish sentiments have significant negative effects, indicating that these sentiments reduce realized skewness during extreme greed. The VIX index is also negative and significant. The return variable shows a significant positive relationship, suggesting that higher returns increase realized skewness. This shows that in periods of extreme greed, investors experience significant positive returns while periods of extreme fear lead to significant negative returns.

For negative realized skewness under extreme fear, the FGI and its squared term are insignificant. The USDX index is positive and significant, indicating that a stronger USDX index increases negative realized skewness. Both bearish and bullish sentiments have significant negative effects, suggesting that these sentiments reduce negative realized skewness. The VIX index is negative and significant, and the return variable shows a significant positive relationship, suggesting that higher returns increase negative realized skewness.

For negative realized skewness under extreme greed, the FGI and its squared term are also insignificant. The USDX index is positive and significant, indicating that a stronger USDX index increases negative realized skewness. Both bearish and bullish sentiments have significant negative effects. The VIX index is negative and significant. The return variable shows a significant negative relationship, suggesting that higher returns reduce negative realized skewness.

With positive realized skewness under extreme fear, the FGI and its squared term are insignificant. The USDX index is insignificant as well. While both bearish and bullish sentiments have significant positive effects, indicating that these sentiments increase positive realized skewness. The VIX index is insignificant. The return variable shows a significant negative relationship, suggesting that higher returns reduce positive realized skewness.

For positive realized skewness under extreme greed, the FGI and its squared term are insignificant. The USDX index is significant and negative. Both bearish and bullish sentiments have significant negative effects. The VIX index is negative and significant. The return variable shows a significant positive relationship, suggesting that higher returns increase positive realized skewness.

For realized kurtosis under extreme fear, the FGI is significant and negative, indicating that increased fear reduces realized kurtosis. The FGI squared term is positive and significant. This shows the significant non-linear dynamic effect FGI has with realized kurtosis, suggesting a threshold effect, where extreme fear first stabilizes return distributions (lower kurtosis), but beyond a certain point, it amplifies tail risks, leading to a fatter-tailed distribution (higher kurtosis). The USDX index is significant at a 10% level. Both bearish and bullish sentiments have significant positive effects. The VIX index is negative and significant. The return variable shows a significant positive relationship, suggesting that higher returns increase realized kurtosis.

For realized kurtosis under extreme greed, the FGI and its squared term are insignificant. The USDX index is significant and negative. Both bearish and bullish sentiments have a significant negative relationship with realized kurtosis. The VIX index is negative and significant. The return variable shows a significant positive relationship, suggesting that higher returns increase realized kurtosis.

In summary, the results show that during periods of extreme greed, higher market volatility (VIX) reduces realized volatility, skewness, and kurtosis, suggesting that extreme optimism dampens market distortions and stabilizes the distribution of returns, contrary to typical expectations of heightened volatility and risk during such periods. This implies that investor sentiment can significantly alter market dynamics, leading to unexpected stabilization even when volatility is perceived to be high.

6. Conclusion

This study investigates the relationship between realized higher-order moments and the Fear and Greed Index. Using 5-minute return data from January 3, 2011, to September 18, 2020, we estimate daily realized moments for the US stock market index (S&P 500 index).

Our findings show how different economic indicators and sentiment indices influence market behaviour under varying conditions. We note that the Fear and Greed index significantly impacts realized volatility during periods of extreme fear and fear, reflecting the strong impact of investor sentiment on market dynamics. The USDX index plays a critical role in market uncertainty, particularly, affecting volatility during extreme fear and neutral sentiment levels. Additionally, the VIX index consistently impacts volatility across all sentiment levels, this suggests the relevance of market volatility in shaping realized volatility. The return variable has a persistent relationship with volatility during extreme fear, greed, and extreme greed which highlights its ongoing impact on market dynamics.

For realized skewness, we note that the USDX index and returns consistently impact skewness across various sentiment levels, while bearish and bullish sentiments tend to reduce skewness during periods of greed. We observe that during periods of extreme fear and fear, the Fear and Greed index, bearish, and bullish sentiments significantly increase positive realized skewness. Also, during extreme greed, the bearish and bullish sentiments tend to reduce positive skewness. The VIX index generally reduces skewness across most sentiment levels but increases positive realized skewness during fear sentiment and reduces it during greed sentiment. These relationships highlight the complex role market sentiment plays in shaping the asymmetric nature of asset return distributions.

Our results also reveal significant variations for realized kurtosis across different sentiment conditions. We note that the Fear and Greed index, and the bearish and bullish sentiments significantly impact realized kurtosis during extreme fear and fear periods, this shows changes in the extremeness of return distributions. The USDX index significantly affects kurtosis positively and negatively during extreme fear and extreme greed periods, respectively. The VIX index has a significant negative relationship with realized kurtosis during extreme fear and extreme greed periods. The return variable has a significant positive relationship with realized kurtosis across all sentiment levels, highlighting its persistent impact on return extremeness. The results remain consistent when controlling for the non-linear attributes of the Fear and Greed index during periods of extreme fear and extreme greed. These relationships show the significant and unique role market sentiment plays in shaping the extremity nature of asset return distributions.

The findings are important for financial risk management and modeling, as they show that varying sentiment levels significantly affect the relationship between market sentiments and realized moments. This suggests that understanding these dynamics allows investors and risk managers to better anticipate market behaviour and adjust their strategies accordingly.

The limitations of this study include: (i) the focus on the US index rather than individual stocks was determined by the availability of high-frequency data for the estimation of higher-order moments in the considered period, and (ii) the availability of the Fear and Greed index.

Author Contributions

R.M.A.:Data curation, Formal analysis, Investigation, Methodology, Resources, Software, Validation, Visualization, Writing (original draft), Writing (review & editing); P.O. Jr.: Supervision, Validation, Visualization, Writing (review & editing); J.K.W.: Validation, Visualization, Writing (review & editing).

Funding

This research received no external funding.

Data Availability Statement

The article makes use of existing (secondary) data.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Albers, S. The fear of fear in the US stock market: Changing characteristics of the VVIX. Finance Research Letters 2023, 55, 103926. [Google Scholar]

- Yang, S. Pandemic, policy, and markets: insights and learning from COVID-19’s impact on global stock behavior. Empirical Economics, 2024; 1–29. [Google Scholar]

- Sarwar, G. Is VIX an investor fear gauge in BRIC equity markets? Journal of Multinational Financial Management 2012, 22, 55–65. [Google Scholar]

- Smales, L.A. Risk-on/Risk-off: Financial market response to investor fear. Finance Research Letters 2016, 17, 125–134. [Google Scholar]

- Li, W.; Chien, F.; Waqas Kamran, H.; Aldeehani, T.M.; Sadiq, M.; Nguyen, V.C.; Taghizadeh-Hesary, F. The nexus between COVID-19 fear and stock market volatility. Economic research-Ekonomska istraživanja 2022, 35, 1765–1785. [Google Scholar]

- Hollstein, F.; Nguyen, D.B.B.; Prokopczuk, M.; Simen, C.W. International tail risk and world fear. Journal of International Money and Finance 2019, 93, 244–259. [Google Scholar]

- Elyasiani, E.; Gambarelli, L.; Muzzioli, S. The skewness index: uncovering the relationship with volatility and market returns. Applied Economics 2021, 53, 3619–3635. [Google Scholar]

- Sarwar, G. US stock market uncertainty and cross-market European stock returns. Journal of Multinational Financial Management 2014, 28, 1–14. [Google Scholar]

- Smales, L.A. Spreading the fear: The central role of CBOE VIX in global stock market uncertainty. Global Finance Journal 2022, 51, 100679. [Google Scholar]

- Tang, G.Y.; Shum, W.C. The relationships between unsystematic risk, skewness and stock returns during up and down markets. International Business Review 2003, 12, 523–541. [Google Scholar]

- Amaya, D.; Christoffersen, P.; Jacobs, K.; Vasquez, A. Does realized skewness predict the cross-section of equity returns? Journal of Financial Economics 2015, 118, 135–167. [Google Scholar]

- Smales, L.A. Effect of investor fear on Australian financial markets. Applied Economics Letters 2017, 24, 1148–1153. [Google Scholar] [CrossRef]

- Nieto, B.; Novales, A.; Rubio, G. Variance swaps, non-normality and macroeconomic and financial risks. The Quarterly Review of Economics and Finance 2014, 54, 257–270. [Google Scholar]

- Azimli, A.; Kalmaz, D.B. The impact of Russia’s Geopolitical Risk on stock markets’ high-moment risk. Economic Systems, 2024; 101242. [Google Scholar]

- He, X.; Hamori, S. The higher the better? Hedging and investment strategies in cryptocurrency markets: Insights from higher moment spillovers. International Review of Financial Analysis 2024, 95, 103359. [Google Scholar]

- Ahadzie, R.M.; Jeyasreedharan, N. Higher-order moments and asset pricing in the Australian stock market. Accounting & Finance 2024, 64, 75–128. [Google Scholar]

- Lo, A.W.; Zhang, R. The Adaptive Markets Hypothesis: An Evolutionary Approach to Understanding Financial System Dynamics; Oxford University Press, 2024.

- Kahneman, T. D. kahneman, a. tversky. Prospect theory: An analysis of decisions under risk, 1979; 263–291. [Google Scholar]

- Ali, S.R.M.; Ahmed, S.; Östermark, R. Extreme returns and the investor’s expectation for future volatility: Evidence from the Finnish stock market. The Quarterly Review of Economics and Finance 2020, 76, 260–269. [Google Scholar]

- Huang, T.C.; Wang, K.Y. Investors’ fear and herding behavior: evidence from the taiwan stock market. Emerging Markets Finance and Trade 2017, 53, 2259–2278. [Google Scholar]

- Jin, H.; Zhou, X.Y. Greed, leverage, and potential losses: A prospect theory perspective. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics 2013, 23, 122–142. [Google Scholar]

- Brunnermeier, M.K.; Parker, J.A. Optimal expectations. American Economic Review 2005, 95, 1092–1118. [Google Scholar]

- Brunnermeier, M.K.; Gollier, C.; Parker, J.A. Optimal beliefs, asset prices, and the preference for skewed returns. American Economic Review 2007, 97, 159–165. [Google Scholar]

- Soydemir, G.; Verma, R.; Wagner, A. The asymmetric impact of rational and irrational components of fear index on S&P 500 index returns. Review of Behavioral Finance 2017, 9, 278–291. [Google Scholar]

- Todorov, V. Variance risk-premium dynamics: The role of jumps. The Review of Financial Studies 2010, 23, 345–383. [Google Scholar]

- Kumar, S.; Rao, K.N. Is Fear (VIX) a Priced Factor in Multi Factor Asset Price Modeling? 2014.

- Shaikh, I.; Padhi, P. The implied volatility index: Is ‘investor fear gauge’or ‘forward-looking’? Borsa Istanbul Review 2015, 15, 44–52. [Google Scholar]

- Economou, F.; Panagopoulos, Y.; Tsouma, E. Uncovering asymmetries in the relationship between fear and the stock market using a hidden co-integration approach. Research in International Business and Finance 2018, 44, 459–470. [Google Scholar]

- Sarwar, G.; Khan, W. Interrelations of US market fears and emerging markets returns: Global evidence. International Journal of Finance & Economics 2019, 24, 527–539. [Google Scholar]

- Chakraborty, M.; Subramaniam, S. Asymmetric relationship of investor sentiment with stock return and volatility: evidence from India. Review of Behavioral Finance 2020, 12, 435–454. [Google Scholar]

- Graham, M.; Nikkinen, J.; Peltomäki, J. Web-based investor fear gauge and stock market volatility: An emerging market perspective. Journal of Emerging Market Finance 2020, 19, 127–153. [Google Scholar]

- Duong, K.D.; Tran, M.M.; Nguyen, D.V.; Le, H.T.P. How fears index and liquidity affect returns of ivol puzzle before and during the Covid-19 pandemic. Cogent Economics & Finance 2022, 10, 2114175. [Google Scholar]

- Grima, S.; Özdemir, L.; Özen, E.; Romānova, I. The interactions between COVID-19 cases in the USA, the VIX index and major stock markets. International Journal of Financial Studies 2021, 9, 26. [Google Scholar]

- Narang, S.; Pradhan, R.P.; Singh, B.; others. COVID-19 PANDEMIC AND STOCK MARKET RESPONSE: THE ROLE OF COVID-INDUCED FEAR, INVESTOR ATTENTION, AND FIRM-SPECIFIC CHARACTERISTICS. Asian Academy of Management Journal 2023, 28. [Google Scholar]

- Cupák, A.; Fessler, P.; Hsu, J.W.; Paradowski, P.R. Investor confidence and high financial literacy jointly shape investments in risky assets. Economic Modelling 2022, 116, 106033. [Google Scholar]

- Adekoya, O.B.; Oliyide, J.A.; Akinseye, A.B.; Ogunbowale, G.O. Oil and multinational technology stocks: Predicting fear with fear at the first and higher order moments. Finance Research Letters 2022, 46, 102210. [Google Scholar]

- Westerhoff, F.H. Greed, fear and stock market dynamics. Physica A: Statistical Mechanics and its Applications 2004, 343, 635–642. [Google Scholar]

- Banerjee, A.K.; Dionisio, A.; Sensoy, A.; Goodell, J.W. Extant linkages between Shanghai crude oil and US energy futures: Insights from spillovers of higher-order moments. Energy Economics, 2024; 107683. [Google Scholar]

- Hu, B.; McInish, T. Greed and fear in financial markets: the case of stock spam e-mails. Journal of Behavioral Finance 2013, 14, 83–93. [Google Scholar]

- Erdemlioglu, D.; Gradojevic, N. Heterogeneous investment horizons, risk regimes, and realized jumps. International Journal of Finance & Economics 2021, 26, 617–643. [Google Scholar]

- John, K.; Li, J. COVID-19, volatility dynamics, and sentiment trading. Journal of Banking & Finance 2021, 133, 106162. [Google Scholar]

- Dilmac, M.; Sumer, S.; Mola, H.; Altinkaynak, F. The effect of the fear index, dollar index and bitcoin on volatility: An example from Borsa Istanbul. Asian Economic and Financial Review 2023, 13, 970–980. [Google Scholar]

- Balcilar, M.; Bonato, M.; Demirer, R.; Gupta, R. The effect of investor sentiment on gold market return dynamics: Evidence from a nonparametric causality-in-quantiles approach. Resources Policy 2017, 51, 77–84. [Google Scholar]

- Back, K. Asset pricing for general processes. Journal of Mathematical Economics 1991, 20, 371–395. [Google Scholar]

- Fleming, J.; Paye, B.S. High-frequency returns, jumps and the mixture of normals hypothesis. Journal of Econometrics 2011, 160, 119–128. [Google Scholar]

- Andersen, T.G.; Bollerslev, T. Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. International economic review, 1998; 885–905. [Google Scholar]

- Andersen, T.G.; Bollerslev, T.; Diebold, F.X.; Labys, P. Modeling and forecasting realized volatility. Econometrica 2003, 71, 579–625. [Google Scholar]

- Hansen, P.R.; Lunde, A. An unbiased measure of realized variance. Available at SSRN 524602, 2024; Available at: http://www.ims.nus.edu.sg/Programs/econometrics/files/al_paper1.pdf. [Google Scholar]

- Hansen, P.R.; Lunde, A. An optimal and unbiased measure of realized variance based on intermittent high-frequency data. Unpublished paper, Department of Economics, Stanford University, 2023; Available at: http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.199.5381&rep=rep1&type=pdf. [Google Scholar]

- Barndorff-Nielsen, O.E.; Shephard, N. Power and bipower variation with stochastic volatility and jumps. Journal of financial econometrics 2004, 2, 1–37. [Google Scholar]

- Andersen, T.G.; Bollerslev, T.; Diebold, F.X. Roughing it up: Including jump components in the measurement, modeling, and forecasting of return volatility. The review of economics and statistics 2007, 89, 701–720. [Google Scholar]

- Barndorff-Nielsen, O.E.; Shephard, N. Estimating quadratic variation using realized variance. Journal of Applied econometrics 2002, 17, 457–477. [Google Scholar]

- Ahadzie, R.M.; Jeyasreedharan, N. Effects of intervaling on high-frequency realized higher-order moments. Quantitative Finance 2020, 20, 1169–1184. [Google Scholar]

- Ahadzie, R.M.; Jeyasreedharan, N. Trading volume and realized higher-order moments in the Australian stock market. Journal of Behavioral and Experimental Finance 2020, 28, 100413. [Google Scholar]

- Kim, T.H.; White, H. On more robust estimation of skewness and kurtosis. Finance Research Letters 2004, 1, 56–73. [Google Scholar]

- Andersen, T.G.; Bollerslev, T. Intraday periodicity and volatility persistence in financial markets. Journal of empirical finance 1997, 4, 115–158. [Google Scholar]

- Huang, X.; Tauchen, G. The relative contribution of jumps to total price variance. Journal of financial econometrics 2005, 3, 456–499. [Google Scholar]

- Bandi, F.M.; Russell, J.R. Microstructure noise, realized variance, and optimal sampling. The Review of Economic Studies 2008, 75, 339–369. [Google Scholar]

- Whaley, R.E. The investor fear gauge. Journal of portfolio management 2000, 26, 12. [Google Scholar]

- Ehrmann, M.; Fratzscher, M.; Rigobon, R. Stocks, bonds, money markets and exchange rates: measuring international financial transmission. Journal of Applied Econometrics 2011, 26, 948–974. [Google Scholar]

- Da, Z.; Engelberg, J.; Gao, P. The sum of all FEARS investor sentiment and asset prices. The Review of Financial Studies 2015, 28, 1–32. [Google Scholar]

- Szczygielski, J.J.; Charteris, A.; Obojska, L.; Brzeszczyński, J. Recession fears and stock markets: An application of directional wavelet coherence and a machine learning-based economic agent-determined Google fear index. Research in International Business and Finance, 2024; 102448. [Google Scholar]

- Andersen, T.G.; Bollerslev, T.; Diebold, F.X.; Ebens, H. The distribution of realized stock return volatility. Journal of financial economics 2001, 61, 43–76. [Google Scholar]

- Vasileiou, E. Behavioral finance and market efficiency in the time of the COVID-19 pandemic: does fear drive the market? In The Political Economy of Covid-19; Routledge, 2022; pp. 116–133.

- Brown, G.W.; Cliff, M.T. Investor sentiment and the near-term stock market. Journal of empirical finance 2004, 11, 1–27. [Google Scholar]

- Boyer, B.H.; Vorkink, K. Stock options as lotteries. The Journal of Finance 2014, 69, 1485–1527. [Google Scholar]

- Boyer, B.; Mitton, T.; Vorkink, K. Expected idiosyncratic skewness. The Review of Financial Studies 2010, 23, 169–202. [Google Scholar]

- Conrad, J.; Dittmar, R.F.; Ghysels, E. Ex ante skewness and expected stock returns. The Journal of Finance 2013, 68, 85–124. [Google Scholar]

- Baker, M.; Wurgler, J. Investor sentiment and the cross-section of stock returns. The journal of Finance 2006, 61, 1645–1680. [Google Scholar]

| 1 | |

| 2 |

Figure 1.

This graph reports the relationship between S&P 500 index and realized higher-order moments across time. The moments realized variance, realized skewness (both positive and negative), and realized kurtosis.

Figure 1.

This graph reports the relationship between S&P 500 index and realized higher-order moments across time. The moments realized variance, realized skewness (both positive and negative), and realized kurtosis.

Table 1.

Impact of investor sentiment on moments.

| Sentiment Level | Volatility | Negative Skewness | Positive Skewness | Kurtosis |

|---|---|---|---|---|

| Extreme Fear | Significantly increases | Significantly increases | Significantly decreases | Significantly increases |

| Fear | Increases | Increases | Decreases | Increases |