Submitted:

22 October 2024

Posted:

22 October 2024

You are already at the latest version

Abstract

Purpose – This paper aims to investigate the role of forensic accounting skills in enhancing auditor self-efficacy towards fraud detection in Indonesia. In addition, explores the moderating effect of the implementation of Generalized Audit Software (GAS) and whistleblowing system on the relationship between accounting and auditing skills and auditor self-efficacy, as well as its role in enhancing fraud detection. Methodology– A cross-sectional survey was developed and distributed to 537 external auditors working in Indonesia. This study uses a multiple linear regression analysis method with multiple linear moderation models using WarpPLS 8.0 software. Findings – The study results indicate a significant direct relationship between practical communication skills, psychosocial skills, accounting and auditing skills, and auditor self-efficacy. However, technical and analytical factors do not affect auditor self-efficacy. The study's results indicate a significant direct relationship between auditor self-efficacy and fraud detection. It is revealed that implementing GAS moderates the relationship between auditor self-efficacy and fraud detection. In contrast, the study's results do not show a significant relationship between technical and analytical skills and auditor self-efficacy. Novelty– This research paper's originality lies in exploring the role of forensic accounting skills by using GAS and Whistleblowing systems to enhance auditor self-efficacy toward fraud detection in Indonesia.

Keywords:

Forensic Accounting

; Fraud Detection

; Whistleblowing Systems

; Risk Management

; Generalized Audit Software

1. Introduction

Fraud is a global issue that is still very interesting to discuss. The implications in the business world are that this fraudulent act is very detrimental to the company (Rustiarini et al., 2021). Activities related to Fraud that are generally unknown in a company determine a series of deviations and prohibited actions characterized by deliberate Fraud carried out by a fraudster (Sánchez-Aguayo et al., 2021). Fraudulent activities can result in significant financial losses, weaken investor confidence, and hinder economic development growth (Al Natour et al., 2023). Therefore, Fraud must be detected as early as possible not to have an even more significant impact.

ACFE, (2022) has released the results of a survey on Fraud. The results showed that the Asia Pacific region was ranked third with 183 fraud cases. In the survey, the most common form of Fraud was corruption, with an average loss due to Fraud reaching $200,000. The number of corruption cases in Indonesia is still relatively high. In the last five years, the value of the Indonesian Corruption Perception Index has tended to decline. In 2019, Indonesia's Corruption Perception Index was 40/100. This value decreased in 2022 to 34/100. In early 2024, Transparency International released Indonesia's latest Corruption Perception Index with a score of 34/100. This indicates that the government's efforts to handle corruption cases have failed. Fraud is a rapidly increasing phenomenon worldwide, and organizations need to be firm in their fraud detection and prevention tools (Saluja, 2024). Fraud can be detected through the audit process. Determining fraudulent acts and providing appropriate recommendations for prevention can be done through comprehensive audit activities (Saragih & Dewayanto, 2023). This approach has proven to be very useful in identifying fraudulent financial reporting, which can significantly disrupt the reliability and efficiency of financial markets (Daraojimba et al., 2023).

Forensic accounting skills play a crucial role in fraud detection, particularly in Indonesia, where fraudulent activities continue to evolve. Forensic accounting involves the application of specialized knowledge and investigative skills to identify and analyze financial discrepancies and Fraud. However, the effectiveness of forensic accounting in fraud detection can be influenced by various factors, including the use of Generalized Audit Software (GAS) and the implementation of a whistleblowing system. Research indicates that forensic accounting alone may not significantly impact fraud detection unless complemented by other mechanisms. For example, a study found that forensic accounting did not directly affect fraud detection, suggesting that forensic accountants are not fully integrated into fraud detection efforts (Hassan et al., 2023). On the other hand, investigative audit capabilities and auditor experience significantly impact fraud detection, highlighting the importance of comprehensive audit skills and knowledge in identifying fraudulent activities. In fraud detection, an auditor needs to master forensic accounting. Forensic accounting services utilize the specialized skills of public accountants, auditing, tax economics, fraud detection, and other skills to conduct various types of investigations and communicate findings in a courtroom or administrative environment (Elisha et al., 2020). These specialized skills in forensic accounting include technical and analytical skills, practical communication skills, psychosocial skills, and accounting and auditing skills. Many organizations that conduct audits are computerized, creating new possibilities and risks for the auditor's work (Pathmasiri & Piyananda, 2021). Audit software is developed to automate processes and improve data analysis and audit work (Alotaibi & Alnesafi, 2023).

In recent years, audits have used computer-assisted audit techniques (CAATs). CAATs are the use of computers in audit activities to obtain audit evidence, making it easier for auditors to collect and analyze electronic-based information (Handoko et al., 2020). GAS is the most popular form of audit technology in the CAATs category (Pathmasiri & Piyananda, 2021). This approach allows auditors to access and retrieve various data files into a computer and perform tests as needed (Handoko et al., 2022). After Fraud is identified and detected, fraudulent actions can be disclosed through the Whistleblowing System. This Whistleblowing System has an important role that can be a medium for revealing illegal acts, unethical behavior, or other actions that occur in the company and are detrimental to the organization (Gaaya et al., 2017). The Whistleblowing System allows individuals to report fraudulent practices without fear or intimidation. Thus, the company can immediately stop fraudulent practices and maintain financial integrity (Oktaviany & Reskino, 2023). Research on auditor self-efficacy in detecting Fraud has previously been conducted. The results of the study Rustiarini et al., (2021); Atmadja et al., (2019); Milanie et al., (2019); Al Natour et al., (2023) stated that Auditor Self-Efficacy has a significant influence on fraud detection. Meanwhile, according to the study's results Azzahroh et al., (2020), auditor self-efficacy has no significant relationship with fraud detection. The difference in research results made researchers conduct further research on the relationship between auditor self-efficacy and fraud detection. Based on the existing phenomena and research results, this study aims to analyze and test the direct and indirect impacts between auditor self-efficacy and fraud detection. Therefore, this study focuses on testing the direct effect of auditor self-efficacy on fraud detection. At the same time, the impact of the indirect relationship is integrated from General Audit Software and Whistleblowing Systems as a moderating variable to measure the effect of auditor self-efficacy on fraud detection.

2. Literature Review

Technical and Analytical Skills (TAS), which involve the ability to analyze complex financial data, interpret financial transactions, and use specialized training tools to identify and analyze financial transactions, including anomalies that may indicate fraudulent activity, maintain a critical mindset in pursuing forensic excellence. According to Al Natour et al., (2023), TAS is a crucial component of the auditor's forensic investigation team, which requires extensive research to detect Fraud. The study conducted by McMullen & Sanchez, (2010) and S. C. Chukwu et al., (2019) highlights the importance of TAS in identifying the suspect in a financial transaction. It indicates that decreasing TAS can result in ineffective and short-lived forensic investigations.

Furthermore, having a more effective 'auditor's signature, a term used to describe an auditor's unique approach and style is linked to having a stronger TAS. According to Bandura, (1977), self-efficacy reduces an individual's ability to carry out tasks efficiently. A study reveals that auditors with strong analytical skills, such as TAS, consistently have higher self-efficacy, positively impacting their ability to create informative reports during audits. According to the study conducted by Rumondang et al., for example, auditors with high levels of personal effectiveness perform better when creating accurate audit reports. Research by Kharisma and Budiartha indicates that emotional intelligence as a moderator that strengthens this bond positively impacts audit quality. Furthermore, Plumlee et al. stress the importance of metacognitive training, including analytics tendency to diverge and converge, to increase auditor productivity at the required level in the analysis procedure.

Additionally, Suwandi et al. point out that emotional intelligence and task complexity, when combined with emotional intelligence, negatively impact auditor evaluations and highlight the need for emotional intelligence analysts to handle complex tasks and enhance audit quality. The study conducted by Masruroh indicates that professional expertise, including analysis, significantly affects an auditor's ability to detect and validate Fraud. Furthermore, research by Kristyanti reveals that emotional intelligence, whether in the form of emotional intelligence or self-efficacy, positively affects auditor work performance. It also indicates that the effectiveness of analysis can be increased if it is linked to emotional intelligence. Rohmawati said that self-efficacy also affects job satisfaction and turnover intentions. Auditors seek better job opportunities and challenges, which may be driven by their confidence in their analytical abilities and desire for professional growth. This study highlights the importance of 'analytic skills, a term used to describe the combination of analytical skills and expertise, in developing the auditor's effectiveness, improving work efficiency, the quality of putting in work, and the ability to adjust to changing circumstances in the auditing profession.

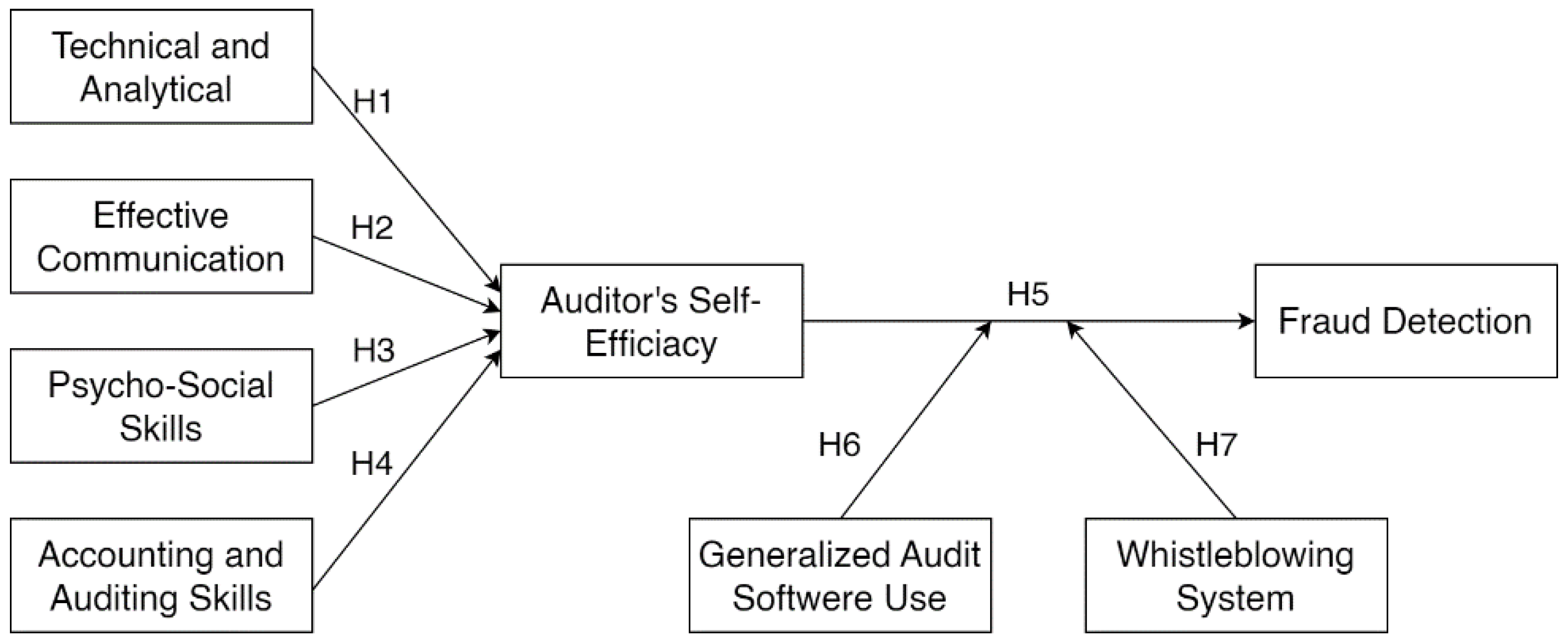

H1: There is an association between technical and analytical skills and auditor’s self-efficacy

Practical Communication Skills (ECS) are a critical competency every forensic accountant should possess. Clearly and concisely communicating ideas to various stakeholders—such as lawyers, law enforcement agencies, and other professionals—is crucial. Forensic experts must record incident reports, prepare presentations, and provide evidence in court. However, the actual value of ECS lies in its ability to ensure that research results are understood and empathetically considered from the client's perspective. S. C. Chukwu et al., (2019) conducted research highlighting the importance of communication skills for forensic experts to clearly and concisely report their findings. According to Smith, (2005), Effective communication skills are crucial for auditors to understand client perspectives, provide accurate and comprehensive information, and establish strong relationships with clients.

Practical communication skills also strongly relate to the auditor's effectiveness, which is their self-belief in carrying out the audit task. The Auditor Self-Efficacy Scale (ASE) is a sub-scale measuring technical proficiency, technological adaptation, and interpersonal communication. It emphasizes the importance of personal efficiency in auditing competence. Research indicates that communication skills training can improve auditors' efficiency and ability to collaborate and form bonds with coworkers and superiors (Rydzak et al., 2023). Effectiveness positively impacts audit quality, and emotional intelligence serves as a moderator to enhance this effect (Pinatik, 2021). High communication needs have been identified since the 1980s, with research indicating that these needs are frequently not met by the general public, indicating the need for intervention to increase communication efficiency (Rydzak et al., 2023).

Efficiency in self-reporting also affects audit results and employee quality; additionally, self-reporting efficiency, in conjunction with goal orientation, has a positive impact on the audit process (Salehi & Dastanpoor, 2021). During the COVID-19 pandemic, virtual audits and emotional assessments evaluated the auditor's effectiveness, leading to lower auditor effectiveness in unfavorable conditions (Pramana et al., 2019). Workplace performance, motivation, and daily life also impact auditor work, with self-efficacy as a mediating factor. Utilizing computer-assisted audit techniques (CAATs) and computer self-efficacy (CSE) also positively impacts auditor work processes by highlighting the relevance of technological advancements in contemporary auditing. More extensive literature on communication in auditing highlights the importance of effective communication in internal audit processes and how it affects organizational results (Handayani et al., 2020). Thus, research studies like this one indicate that improving auditor efficiency through targeted training in communication and other relevant areas can significantly enhance audit quality and overall work performance.

H2: There is an association between practical communication skills and an auditor's self-efficacy.

Another crucial skill that every forensic expert should possess is Psychosocial Skills (PSS). This training significantly increases the ability to understand human nature, human behavior, and motifs. It also helps to read body language and detect deception. Forensic experts must establish strong relationships with clients and interested parties to obtain accurate information. They also need to be able to work together with other professionals who are qualified for the research, as demonstrated by (Boyle et al., 2017). A strong PSS is not just a skill but a crucial tool for auditors to improve their ability to detect and minimize Fraud. This skill allows auditors to communicate effectively, establish connections with clients and other stakeholders, and identify warning signs that could indicate fraudulent activity. Investing in strong PSS and other essential skills like TAS (Technical and Analytical Skills) can increase auditors' ability to detect Fraud successfully and, eventually, their internal efficiency, thereby instilling confidence and security in the auditing profession. PSS maintains a rigorous approach to improving auditor efficiency, significantly impacting audit quality and workflow.

The effectiveness of the individual, or their ability to accomplish tasks with success, is a crucial factor in the auditing profession. The Auditor Self-Efficacy (ASE) scale, designed to measure auditor confidence in core competencies such as technical proficiency, technological adaptation, and interpersonal communication, emphasizes the importance of psychosocial competence in auditing (Bowering et al., 2020). Research indicates that emotional intelligence positively affects audit quality, which enhances the auditor's ability to communicate with clients and manage their emotions effectively. Psychological factors such as self-worth, trustworthiness, and spirituality can affect auditor efficiency, emphasizing the importance of social cognition in audit work (Lari Dashtbayaz et al., 2022). During the COVID-19 pandemic, auditor efficacy was strengthened through face-to-face interviews, verbal and social interactions, vicariate interviews, and virtual audits. This demonstrates auditors' ability to adjust to crisis psychosocial stressors. Practical communication skills are essential for auditors because they facilitate a more leisurely audit process and help clients develop pleasant relationships, which can result in more honest and straightforward interactions. In addition, emotional intelligence and emotional intelligence skills are critical in detecting Fraud since they increase the auditor's trustworthiness and ability to handle complex and stressful situations (Sari & Nugroho, 2021). Understanding and experience in auditing, mediated by personal efficacy, are also crucial in enhancing audit performance, particularly in relatively complex tasks (Allegrini et al., 2012). Weakened by self-efficacy, professional skepticism is essential for auditors to perform critical analysis and gather appropriate skepticism during an audit (Amlayasa & Riasning, 2022). Finally, emotional intelligence and social identity, combined with professional judgment and sensitivity, positively impact auditor work and highlight the importance of psychosocial skills in auditing (Dixon et al., 2005). The relationship between psychosocial skills and self-efficacy is essential to auditor effectiveness and efficiency since it enables them to handle complex professional tasks confidently and competently.

H3: There is an association between psychosocial skills and auditor's self-efficacy

Auditing and accounting skills are crucial for auditor effectiveness since they significantly impact their work environment, report writing quality, and ability to identify Fraud. Developing the Auditor Self-Efficacy (ASE) scale, a sub-scale for Technical Proficiency, Technological Adaptation, and Interpersonal Communication, emphasizes the importance of these competencies in enhancing auditor efficacy and self-confidence (Al Natour et al., 2023). The research conducted in Mesir indicates that effective communication, psychosocial, and silent auditing improve the auditor's efficiency and ability to detect Fraud. Computer-assisted audit techniques (CAATTs) strengthen this bond and increase the auditor's ability to detect Fraud (Purnamasari et al., 2022).

According to research conducted in Indonesia, practical communication skills are crucial in helping auditors create accurate audit reports, possibly even more so than professional skepticism and perseverance (N. Chukwu et al., 2019). The individual's effectiveness, combined with the auditor's experience and affected by emotional distress, positively impacts the audit quality and indicates that psychological factors are important in the audit process. This also suggests that virtual audits and emotional disorders significantly impair auditor efficacy (Hammersley, 2011).

In the education system, high-achieving students' audits and accountants with a high degree of personal effectiveness indicate higher levels of stress and anxiety in the classroom, indicating that personal effectiveness is crucial for professional development. Orientation goals also affect self-efficacy, performance appraisal and self-efficacy have a positive impact, and avoidance goals have a negative effect (Salehi & Dastanpoor, 2021). In the public sector, professional and personal efficacy are indicators of internal audit quality, while professional efficacy moderates the relationship between audit quality and personal efficacy (Fouziah et al., 2022). In the end, in small-scale audit firms, efficiency is achieved by balancing the objectives and auditors' attention to detail to detect Fraud. This highlights the importance of this approach in complex tasks and the necessity of professional and organizational alignment to reduce audit inspection errors. These studies demonstrate that auditing and accrediting practices are crucial for developing auditor efficacy, improving the auditor's productivity, ability to communicate their views, and detection skills in various situations and challenges.

H4: There is an association between accounting and auditing skills and auditor’s self-efficacy

According to the (ACFE, 2022), Fraud is defined as a kind of discreet negotiation using day-to-day tactics to obtain unfavorable benefits or to cause losses for other parties. Fraud can cause significant financial losses and harm an organization's reputation (Button et al., 2023). The fingerprint detection process (F.D.) uses data analysis, risk assessment, and investigation methods to identify the fingerprint's potential(Alkaabi et al., 2019). A strong sense of self-worth and motivation to complete audit tasks are related to high self-efficacy, potentially increasing Fraud. Effectiveness (Dalnial et al., 2014). Research indicates that higher levels of self-efficacy positively correlate with higher Fraud employee satisfaction (Amlayasa & Riasning, 2022). Consequently, improving efficiency can be a valuable strategy for raising audit quality overall and reducing financial difficulties.

In the context of the Industry 4.0 revolution, the General Audit System (GAS) aims to improve data anomaly detection performance in the audit process by increasing the frequency of anomalous data compared to manual or physical data collection (Bradford et al., 2020a). GAS, also known as Generalized Audit Software (GAS) and Computer Assisted Audit Tools and Techniques (CAATs), is designed to assist auditors in effectively examining and analyzing data to identify potential Fraud, such as anomalous data (Bradford et al., 2020a). In a significant way, using GAS improves internal auditor effectiveness by strengthening their ability to identify suspicious material, irregular control, and Fraud, hence comprehensively raising the quality of information (Sudirman et al., 2021). According to the Bradford et al., (2020b) information system success model, material data is the primary indicator of the quality of information for financial auditors. In contrast, material data is the primary indicator of control and payment irregularities for technical auditors. Integrating analytical data into the methodology for data detection in audits enables auditors to fully understand audit findings and exceptions by utilizing rigorous data collection procedures, which have now become industry standards. Specialized tools like SPSS and CaseWare IDEA and general tools like Microsoft Excel are used for data verification and fingerprint analysis; IDEA is exceptionally user-friendly and does not require a unique label for fingerprint data. CAATs have proven to be a reliable method for detecting Fraud, with auditor sentiment significantly indicating its impact on employee productivity and transparency in financial reporting (Hassan et al., 2023). However, issues such as implementation costs, required resources, and database system performance are related to the creation and use of CAATs.

Additionally, developing a flexible approach based on regulations to identify Fraud in e-commerce transactions highlights the necessity of meeting various customer needs. Utilizing observational data on a financial and operational basis, as demonstrated by research conducted on public companies in Brazil, increasingly highlights the importance of GAS in identifying problem or issue areas and highlighting areas that require attention. Although GAS offers several benefits for data analysis and fingerprint detection, it is essential to recognize the limitations and ensure that training materials and system quality are sufficient to maximize their usefulness. The evolution of audit methodology and software will be significant in assessing the integrity and observance of the increasingly digital financial transactions in the world.

H5: There is an association between auditor’s self-efficacy and fraud detection

The use of computer-assisted audit tools and techniques (CAATTs), such as generalized audit software (GAS), has been shown to strengthen the relationship between human efficiency (ASE) and fraud detection (F.D.). Improving computer literacy—the ability of individuals to use technology to their full potential—contributes to improving literacy, which raises F.D.'s efficiency. Increased efficiency and accuracy in data analysis by CAATTs help auditors identify more accurate Fraud. Increased forensic expertise associated with CAATTs improves auditor efficiency and yields better evidence detection results (Widnyana & Widyawati, 2022). However, other elements that affect F.D. efficacy include workload, professional skepticism, emotional intelligence, and whistleblowing reporting procedures. Self-efficacy substantially affects audit quality and fraud detection when combined with emotional intelligence; however, CAATTs, which offer advanced data analysis tools, attenuate this link. While GAS has numerous advantages, it's crucial to understand its limitations and keep up with professional growth to stay updated with fraud schemes and technical advancements.

Global adoption of GAS still needs to improve. In developed countries like Australia, only 17.4% of internal audit functions traditionally use GAS. In contrast, in developing countries like Nigeria and Tunisia, the adoption of GAS is hindered by issues with day-to-day management, training, and technological compatibility (Esily et al., 2023). Performance expectations and efforts hampered GAS adoption in Malaysia, and it soon needed more social influence (Yusuf et al., 2013). Moreover, GAS is helpful in specific audit contexts, such as Indonesian Syariah audits, and contributes to auditor quality, particularly in large enterprises like the Big Four. According to the DeLone and McLean models, the critical indicator of information quality for financial auditors is detecting suspicious activity, while the focus of technology integrity auditors is on monitoring irregularities in control and expenditure. Good training on GAS usage is essential to increase auditor productivity and usage. However, audit effectiveness is related to GAS, auditor fatigue, and organizational health. Within the educational environment, ease of use and the application of the software hurt students' performance, even though it does not negatively affect their grades silently (Sheldon & Jenkins, 2020).

The relationship between human efficiency and Fraud detection is complex and affected by various factors, the most notable of which is the existence of the whistleblower system. When individuals realize their shortcomings and ignorance, their self-efficacy, based on their ability to do tasks and meet goals, is positively correlated with detecting deception. However, a robust reporting system can significantly increase the effectiveness of facial recognition.

H6: The GAS moderates the association between self-efficacy and fraud detection

According to research findings, the whistleblowing system provides a safe, structured environment for reporting suspicious activity. It gives individuals the confidence to make decisions based on their judgment without fear of repercussions. This system not only assists employees in reporting non-etis cases but also improves the subject's sensitivity to fraud detection by providing the necessary shields and barriers (Al Natour et al., 2023). The study also shows that the whistleblower system's presence significantly affects the fraud detection process, with forensic and investigative audits acting as mediating variables and reducing the subject's level of efficacy in this process (Halbouni et al., 2016). However, while human efficiency is essential, it sometimes moderates the relationship between whistleblowing and fingerprint detection systems. A few studies indicate that the effectiveness of whistleblowing regulations, subjectivity norms, and the control of public opinion do not significantly influence whistleblowing. In addition, the effectiveness of the whistleblowing system in detecting theft is also affected by organizational barriers, employee privacy, and ethical workplace practices, all of which are crucial for enhancing employee efficiency (Nurcahyono et al., 2021). In the relevant industry, such as the food industry, training programs that increase work productivity and self-efficacy have been shown to improve whistleblowing (Prasetiyo et al., 2024). However, a few studies show that a weak and unreliable whistleblowing system, along with subpar ethics, can hinder the process of whistleblowing, indicating the need for a well-designed and reliable whistleblowing mechanism to maximize the benefits of human efficiency in whistleblowing detection (Nurcahyono et al., 2021). Overall, even if human efficiency plays a crucial role in leak detection, its effectiveness is greatly enhanced by a well-designed and user-friendly whistleblowing system. This system provides the necessary work experience to help applicants understand themselves and be honest, improving their communication ability to increase the fraud detection rate effectively.

H7: The whistleblowing system moderates the association between self-efficacy and fraud detection

Figure 1.

Theoretical framework.

3. Methodology

3.1. Survey and Data Collection

This study uses a cross-sectional design to describe the conditions studied. Data were collected over a predetermined period to obtain a comprehensive picture of the role of forensic accounting skills in detecting Fraud and the moderating effect of using GAS (Generalized Audit Software) and whistleblowing systems. The questionnaires were completed by external auditors from Indonesian public accounting firms within four months of data collection.

3.2. Measurement

The main instrument in this study was a questionnaire designed using the 5-Likert method to measure each variable described in Table 1. as follows:

3.3. Assessment of Partial Least Square Structural Equation Modeling

This study uses a multiple linear regression analysis method with multiple linear moderation models using WarpPLS 8.0 software. Multiple linear moderation models are intended to test and analyze how moderating variables affect the relationship between independent and dependent variables. The model in this study is precisely to determine whether using GAS (Generalized Audit Software) and whistleblowing systems as moderating variables will help external auditors in Indonesia disclose Fraud with their forensic accounting skills. The demographic profile of the respondents, including gender, age, educational background, and professional qualifications, is described in detail in Table 2.

4. Results

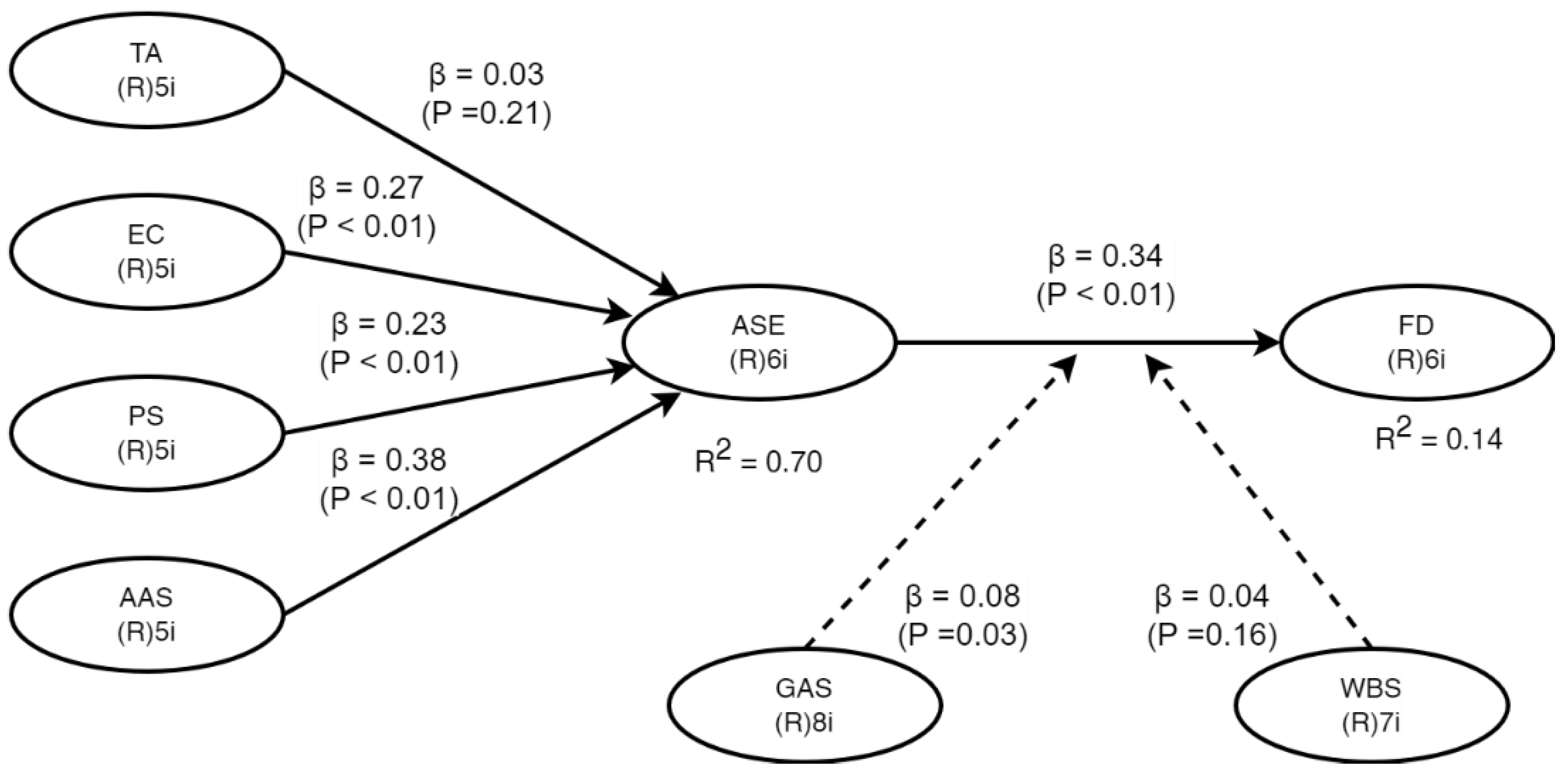

The 573 samples that could be analyzed in this study are described in Descriptive Statistics in Table 3. Next, Based on Table 4. the model fit analysis results, the developed model has performed very well in explaining the relationship between research variables.

This model can be relied on to make inferences and predictions with a significant APC value (p <0.001) and a moderate ARS (0.418), indicating a strong and relevant relationship between the variables in the model. Adjusted R-Squared Mean approaching ARS indicates that the model remains good even though it takes into account the number of variables. Furthermore, the AVIF and AFVIF values below the ideal threshold indicate no severe problems related to multicollinearity between independent variables. Then, the GoF value, which is far above the minimum threshold, and the SPR value, which does not show Simpson's paradox, confirm the overall model fit. RSCR approaching 1 indicates a solid contribution of independent variables in explaining the variance of the dependent variable. In addition, the SSR and NLBCDR values equal to 1 indicate the absence of a suppressor effect and the direction of causality by the hypothesis.

The analysis results show that respondents generally have a pretty good level of competence in various aspects of the auditor profession. The Forensic Accounting Skill variable tested with Technical and Analytical Skills, Effective Communication, Psychosocial Skills, Accounting, and Auditing has a relatively high average value (around 21-22) with a low standard deviation (around 2.5-2.8). This indicates that most respondents feel competent in these areas, although moderate individual variation exists. The auditor self-efficacy variable has the highest average (27.11) with a relatively low standard deviation (1.99), indicating a high confidence level among auditors in their ability to carry out audit tasks. In addition, the Generalized Audit Software Used variable shows a high average value (37.11) and a low standard deviation (2.33), indicating that respondents generally have a high level of familiarity with the use of audit software. In the Whistleblowing System variable, although the average is quite high (29.27), the relatively high standard deviation (2.75) indicates a significant variation in perception regarding the violation reporting system among respondents. In the Fraud Detection variable, the average value (30.02) indicates that auditors feel pretty competent in detecting Fraud. Still, the relatively high standard deviation (2.90) indicates a more significant difference in perception than other variables.

Measurement Model Assessment

Figure 2.

SEM Modeling Research Results.

5. Discussion

In the era of Industry 4.0, skills are very much needed, such as creativity in critical thinking, the ability to adapt, and the ability to face challenging situations. All of these abilities and skills can shape a person's self-efficacy. Increasing self-efficacy can be done along with growing experience and developing skills and skills in managing thoughts and emotions. In auditing, auditor self-efficacy emphasizes the auditor's belief in their ability to face and solve problems in certain conditions to achieve their desired goals. Auditors who have high self-efficacy do not guarantee that they also have high technical skills. This is because the development of technical skills is obtained through sufficient practical experience rather than confidence in their abilities. Technical skills are mandatory for an auditor, which includes the technical abilities and knowledge needed to conduct an effective and efficient audit. Auditors who have adequate technical skills can help detect Fraud. An act of Fraud can be motivated by pressure, opportunity, rationalization, and ability, as explained in the fraud diamond theory. The higher the technical skills of an auditor, the faster the Fraud can be detected, and the losses caused by the Fraud can be minimized. Research has been conducted on the relationship between technical skills and auditor self-efficacy in fraud detection. This study's results align with research conducted by Al Natour et al., (2023), which stated that technical skills do not significantly affect self-efficacy in fraud detection.

Practical communication skills can be vital to interacting with various stakeholders. An auditor with high communication skills tends to have high self-efficacy due to the ease of communicating and getting support from various related parties. In addition, an auditor will also have higher confidence in technical skills, technology adaptation, and better interpersonal communication. Communication during the audit process can make it easier for auditors to obtain information on the client's business processes for audit process planning. In the audit process, an auditor must be able to identify errors that occur in an organization, especially those that lead to Fraud. The auditor will use relevant audit procedures during the audit process. Practical communication skills can support the occurrence of Fraud because, without this ability, a fraudulent act may not occur. In the fraud diamond theory, capability can be indirectly linked to practical communication skills. Fraud perpetrators must have the ability and skills to effectively ignore internal controls and develop strategies to hide and carry out fraudulent acts. Auditors with high self-efficacy will find it easier to identify Fraud in an organization, as this is based on the information they get from related parties. Fraud is a very detrimental action. Therefore, awareness and vigilance in the organization must be increased to prevent Fraud. Research has been conducted on the relationship between practical communication skills and self-efficacy in detecting Fraud. This study's results align with research conducted by Al Natour et al., (2023); Atmadja et al., (2019); Rustiarini & Sunarsih, (2017), stating that practical communication skills are significantly related to auditor self-efficacy in detecting Fraud.

Psychosocial Skills (PSS) are vital for forensic accountants and auditors, significantly impacting their ability to detect and prevent Fraud. PSS encompasses a range of abilities, including understanding human behavior, motives, and intentions, reading body language, and detecting deception. These skills are crucial for forensic accountants, who must establish rapport with clients and interviewees to obtain accurate information. Furthermore, PSS enables them to collaborate effectively with other investigation professionals, as Khadim et al., (2021) highlighted. Thus, PSS are not just auxiliary skills but essential tools for enhancing an auditor's fraud detection (F.D.) ability.

Possessing strong PSS enables auditors to communicate effectively, build relationships with clients and stakeholders, and identify subtle cues that may indicate fraudulent behavior. These capabilities are crucial for developing trust and obtaining information to uncover fraudulent activities. Research suggests that emotional intelligence (a key component of PSS) positively affects audit quality by enhancing an auditor's ability to communicate with clients and manage emotions effectively. This is particularly relevant in stressful or high-stakes situations where auditors must maintain professionalism and accuracy.

The relationship between PSS and auditor self-efficacy (ASE) is critical in auditing. ASE refers to the auditor's confidence in their core competencies, such as technical proficiency, technological adaptation, and interpersonal communication. The ASE scale emphasizes the importance of psychosocial competence in auditing, highlighting that skills like emotional intelligence, trustworthiness, and effective communication can significantly impact audit quality and workflow. Strong PSS can also strengthen auditors' self-efficacy, enabling them to handle complex professional tasks with confidence and competence. For instance, during the COVID-19 pandemic, auditors demonstrated adaptability by conducting face-to-face interviews, virtual audits, and social interactions to manage crisis-related psychosocial stressors.

Moreover, emotional intelligence, social identity, professional judgment, and sensitivity significantly impact auditor effectiveness. Auditors with strong PSS can perform critical analysis and maintain professional skepticism during audits. This is crucial in identifying and mitigating risks associated with Fraud and ensuring a rigorous audit process.

Auditing and Accounting Skills (AAS) are critical for forensic accountants and auditors, as they provide a strong foundation for detecting fraudulent activity and ensuring the accuracy and completeness of financial reporting. These skills encompass a thorough understanding of accounting principles, auditing procedures, and the ability to apply these standards effectively in forensic investigations. Forensic accountants must identify financial irregularities, analyze financial statements, and use accounting and auditing standards during investigations. The study by Kaur et al., (2023) highlights that AAS are fundamental for detecting fraudulent activities and financial crimes, emphasizing the importance of these skills in forensic accounting.

AAS is essential for detecting Fraud and positively impacting the overall quality and effectiveness of financial reporting. According to Al Natour et al., (2023); Handoko et al., (2022); Hassan et al., (2023); Lois et al., (2020); Rezaee, (2005), potent AAS is associated with more accurate and complete financial reporting, which in turn enhances fraud detection (F.D.) efforts. This relationship is particularly significant given the increasing complexity of financial reporting standards and regulations, which demand high expertise and knowledge from auditors. Navigating these complexities and applying standards accurately is vital for auditors to maintain their professional integrity and effectiveness.

The potent AAS also enhances Auditor Self-Efficacy (ASE), which refers to an auditor's confidence in their ability to perform their duties effectively. A solid foundation in AAS allows auditors to gain a deeper understanding of a company's financial operations, thereby increasing their ability to identify potential areas of Fraud or misstatement. This confidence translates into better performance and more effective audits. Research indicates that ASE can be enhanced through competencies in technical proficiency, technological adaptation, and interpersonal communication, which are crucial components of AAS (ASE scale). Effective communication, psychosocial skills, and advanced tools like Computer-Assisted Audit Techniques (CAATTs) further improve auditor efficiency and fraud detection capabilities (Research in Indonesia).

Both technical skills and psychological factors influence the development of ASE. For example, research conducted in Indonesia found that practical communication skills can be more critical for creating accurate audit reports than professional skepticism and perseverance. The individual's effectiveness, combined with experience, impacts audit quality and highlights the role of psychological factors such as emotional intelligence in the audit process. During the COVID-19 pandemic, auditors with high emotional intelligence were better able to produce higher-quality work, especially when skilled in high-risk auditing techniques. However, virtual audits and emotional disorders posed significant challenges to auditor efficacy, underscoring the importance of technical and psychological preparedness in times of crisis.

In educational settings, high-achieving students in auditing and accounting programs have shown that personal effectiveness is essential for professional development. However, high levels of stress and anxiety indicate that personal efficacy plays a crucial role in managing complex and demanding environments. Similarly, in the public sector, professional and personal efficacy are critical indicators of internal audit quality. Professional efficacy moderates the relationship between audit quality and personal efficacy, suggesting that a balance between technical skills and psychological resilience is necessary for effective auditing practices.

Moreover, in small-scale audit firms, efficiency is often achieved by balancing objectives and paying attention to detail to detect Fraud. This approach highlights the importance of aligning professional and organizational goals to reduce errors in audit inspections. The alignment ensures auditors can handle complex tasks and challenges effectively, reinforcing the need for a holistic approach that integrates AAS with psychosocial competencies and professional skepticism.

An auditor's self-efficacy is the foundation for detecting Fraud in the industrial era 4.0. This industry faces various fraud schemes, such as Fraud in information technology, artificial intelligence, and big data. Technology was created initially to simplify work; on the other hand, industry players also take advantage of the development of this technology to commit Fraud with its sophistication so that it is difficult to detect (Rawat et al., 2023). Amid a massive ocean of data, auditors are required to be able to identify anomalies that indicate Fraud. Auditors with high self-efficacy tend to be more proactive, persistent, accurate, and innovative in detecting fraud schemes that are developing very rapidly. High self-efficacy makes auditors more selective in identifying and managing the risks of Fraud that occur in today's industry. A positive reinforcement cycle occurs when auditors with high self-efficacy successfully detect Fraud and are motivated to continue improving their performance quality (Amlayasa & Riasning, 2022; Khairi et al., 2020; Muterera, 2024; Prasasti & Sari, 2024). To improve auditor self-efficacy, organizations play a role in allocating adequate resources with training and professional development. In addition, it is essential to create a conducive work environment by providing trust for auditors in carrying out their duties. Close collaboration between auditors and information technology experts is also necessary in overcoming the challenges of Fraud in the digital era (Feliciano & Quick, 2022). By leveraging each other's expertise, organizations can improve fraud detection capabilities, strengthen oversight capabilities, and impact the reputation of the organization and the auditors themselves.

Generalized Audit Software (GAS) catalyzes improving auditor self-efficacy. GAS helps auditors concentrate on strategic elements in a systematic audit process to identify fraud risks and evaluate (Tragouda et al., 2024). The output of GAS is used as a basis for assessing fraud risks and formulating effective audit procedures. Auditors with high levels of self-efficacy utilize the advanced features provided by GAS to detect complex Fraud by conducting in-depth analysis. Using standardized GAS features makes it easier for auditors to prioritize critical analysis of audit results.

GAS's statistical analysis and data mining capabilities play an essential role in identifying anomalous patterns and fraud events at a high level of accuracy (Bhat et al., 2022; Mniai et al., 2023; Singh et al., 2024). Consistent use of GAS will encourage the development of technical capabilities and features that support the auditor's work effectively. Using GAS to carry out auditor duties increases time efficiency and focuses on comprehensive analysis. GAS implements consistent and standardized audit procedures, expanding auditors' confidence in their duties.

The whistleblowing system is designed as a channel for employees or external parties to report suspected violations or unethical actions within the organization (Achyarsyah, 2022). Although this system has great potential to encourage transparency and accountability, it does not directly moderate the relationship between auditor self-efficacy and fraud detection. The whistleblowing system focuses more on reporting mechanisms and whistleblower protection Meitasir et al., (2022) rather than improving an individual's ability to detect Fraud. Meanwhile, auditor self-efficacy is more related to an individual's confidence in carrying out their duties, including detecting Fraud.

The whistleblowing system is unable to moderate the relationship between self-efficacy and fraud detection because this system acts as a mechanism to confirm suspected Fraud that has occurred. The whistleblowing system is reactive and only functions after a party reports it. The success of this system is highly dependent on the awareness and courage of individuals to report. If employees fear retaliation or do not trust the system, they refuse to report. The time it takes to investigate reports of violations is quite long, allowing perpetrators of Fraud to cover their tracks or repeat their actions. Hypothesis Summary is presented in Table 5.

6. Conclusions

This paper highlights the role of enhancing auditor self-efficacy in detecting Fraud. In addition, this study further enhances the understanding of the potential benefits of using technological advancements in the audit process. The whistleblowing system cannot moderate the relationship between accounting and audit skills and auditor self-efficacy or its role in enhancing fraud detection. This paper provides insights for accounting professionals and regulatory bodies in Indonesia, highlighting the importance of leveraging forensic accounting skills and using Generalized Audit Software (GAS) to enhance fraud detection efforts. Forensic accounting skills play a nuanced role in fraud detection, particularly in the Indonesian context. While forensic accounting itself does not significantly impact fraud detection, as evidenced by the limited involvement of forensic accountants in such efforts, the integration of investigative audit capabilities and auditor experience significantly enhances fraud detection outcomes. Additionally, the competence and independence of auditors, bolstered by professional skepticism, are critical factors that enhance the auditor's ability to detect Fraud. However, the moderating effect of professional skepticism does not extend to the whistleblowing system's impact on fraud detection. Good governance and a robust whistleblowing system raise fraud awareness, although this awareness alone does not directly translate into fraud prevention. Generalized Audit Software (GAS) could further enhance these efforts by providing auditors with advanced tools to analyze large datasets and identify anomalies indicative of Fraud. While the specific impact of GAS is not directly addressed in the provided contexts, its potential to improve audit quality and efficiency is well-documented in the broader literature. Moreover, the complexity of related party transactions (RPTs) and their impact on taxable income highlights the need for comprehensive supervision and control, which advanced audit tools and robust whistleblowing mechanisms could facilitate. Overall, integrating forensic accounting skills, investigative audits, and a solid whistleblowing system, potentially augmented by Generalized Audit Software, forms a multifaceted approach to enhancing fraud detection and prevention in Indonesia.

Author Contributions

Conceptualization, T.A. ; methodology, M.A.P.; software, M.A.P..; validation, T.A., M.A.P and C.Y.H; formal analysis, T.A.; investigation, M.A.P.; resources, C.Y.H.; data curation, M.A.P.; writing—original draft preparation, T.A.; writing—review and editing, I.D.P; visualization, I.D.P; supervision, C.Y.H.; project administration, I.D.P.; funding acquisition, T.A. All authors have read and agreed to the published version of the manuscript.

Funding

"This research was funded by Kementerian Pendidikan, Kebudayaan, Riset dan Teknologi Universitas Diponegoro, Grant number: 357-03/UN7.D2/IV/2024.

Acknowledgments

We would like to thank you Kementerian Pendidikan, Kebudayaan, Riset dan Teknologi, Lembaga Penelitian dan Pengabdian Kepada Masyarakat Universitas Diponegoro who have supported and assisted the Research Team in the program World Class Research Universitas Diponegoro.

Conflicts of Interest

The authors declare no conflicts of interest.

References

- ACFE. (2022). Occupational Fraud 2022: A Report to the nations. Association of Certified Fraud Examiners, 1–96.

- Achyarsyah, P. (2022). Can investigative audit and whistleblowing systems prevent fraud? Atestasi: Jurnal Ilmiah Akuntansi, 5(1), 124–136.

- Al Natour, A. R., Al-Mawali, H., Zaidan, H., & Said, Y. H. Z. (2023). The role of forensic accounting skills in fraud detection and the moderating effect of CAATTs application: evidence from Egypt. Journal of Financial Reporting and Accounting.

- Alfordy, F. D. (2022). Effective Detection And Prevention Of Fraud: Perceptions Among Public And Private Sectors Accountants And Auditors In Saudi Arabia. E+M Ekonomie a Management, 25(3), 106–121. [CrossRef]

- Alkaabi, A., Karim, A. M., Hossain, M. I., & Nasiruzzaman, M. (2019). Assets Digitalization: Exploration of Prospects with Better Control Implementation. International Journal of Academic Research in Business and Social Sciences, 9(5), 960–970.

- Allegrini, M., Greco, G., Antonelli, G., Rivieccio, G., Moschera, L., Bachiller, P., Giorgino, M., Bettinelli, C., Bianchi, S., Full, M., Calabrò, A., Mussolino, D., Cerrato, D., Piva, M., Cronjé, C., Buys, P., Demartini, P., Demofonte, S., Di Pietra, R., … Zattoni, A. (2012). Board Diversity and Investments in Innovation : Empirical Evidence from Italian Context. Journal of Management and Governance, 17(1), 1–27. [CrossRef]

- Alotaibi, E. M., & Alnesafi, A. (2023). Assessing the impact of audit software on audit quality: Auditors’ perceptions. International Journal of Applied Economics, Finance and Accounting, 17(1), 97–108.

- Amlayasa, A. A. B., & Riasning, N. P. (2022). The role of emotional intelligence in moderating the relationship of self-efficacy and professional skepticism towards the auditor’s responsibility in detecting fraud. International Journal of Scientific and Management Research, 5(11), 1–14.

- Atmadja, A. T., Saputra, K. A. K., & Manurung, D. T. H. (2019). Proactive fraud audit, whistleblowing and cultural implementation of tri hita karana for fraud prevention.

- Azzahroh, F., Suhendro, S., & Fajri, R. N. (2020). The Effect of Self Efficacy and Fraud Diamond on Fraudulent Behavior Academic Accounting Students. Journal of Business Management and Accounting, 2(1), 322981.

- Bandura, A. (1977). Self-efficacy: toward a unifying theory of behavioral change. Psychological Review, 84(2), 191.

- Bandura, A. (1988). Self-efficacy conception of anxiety. Anxiety Research, 1(2), 77–98. [CrossRef]

- Bhat, M. Q., Alex, S. A., Nanda, S., & Goutham, S. (2022). Qualitative analysis of anomaly detection in time series. 2022 4th International Conference on Circuits, Control, Communication and Computing (I4C), 250–253.

- Bowering, E., Frigault, C., & Yue, A. R. (2020). Preparing Undergraduate Students for Tomorrow’s Workplace: Core Competency Development Through Experiential Learning Opportunities. Canadian Journal of Career Development, 19(1), 56–68.

- Boyle, D. M., Boyle, J. F., & Carpenter, B. W. (2017). Accounting Student Academic Dishonesty: What Accounting Faculty and Administrators Believe. Accounting Educators’ Journal, 26(2006), 39–61.

- Bradford, M., Henderson, D., Baxter, R. J., & Navarro, P. (2020a). Using generalized audit software to detect material misstatements, control deficiencies and fraud: How financial and IT auditors perceive net audit benefits. Managerial Auditing Journal, 35(4), 521–547.

- Bradford, M., Henderson, D., Baxter, R. J., & Navarro, P. (2020b). Using generalized audit software to detect material misstatements, control deficiencies and fraud: How financial and IT auditors perceive net audit benefits. Managerial Auditing Journal, 35(4), 521–547. [CrossRef]

- Button, M., Hock, B., Shepherd, D., & Gilmour, P. M. (2023). What really works in preventing fraud against organisations and do decision-makers really need to know? Security Journal, 1–19.

- Chukwu, N., Asaolu, T. O., Uwuigbe, O. R., Uwuigbe, U., Umukoro, O. E., Nassar, L., & Alabi, O. (2019). The impact of basic forensic accounting skills on financial reporting credibility among listed firms in Nigeria. IOP Conference Series: Earth and Environmental Science, 331(1), 012041. [CrossRef]

- Chukwu, S. C., Rafii, M. Y., Ramlee, S. I., Ismail, S. I., Hasan, M. M., Oladosu, Y. A., Magaji, U. G., Akos, I., & Olalekan, K. K. (2019). Bacterial leaf blight resistance in rice: a review of conventional breeding to molecular approach. Molecular Biology Reports, 46, 1519–1532.

- Dalnial, H., Kamaluddin, A., Sanusi, Z. M., & Khairuddin, K. S. (2014). Detecting Fraudulent Financial Reporting through Financial Statement Analysis. Journal of Advanced Management Science, 2(1), 17–22. [CrossRef]

- Daraojimba, C., Abioye, K. M., Bakare, A. D., Mhlongo, N. Z., Onunka, O., & Daraojimba, D. O. (2023). Technology and innovation to growth of entrepreneurship and financial boost: a decade in review (2013-2023). International Journal of Management & Entrepreneurship Research, 5(10), 769–792.

- Dixon, R., Mousa, G. A., & Woodhead, A. (2005). The role of environmental initiatives in encouraging companies to engage in environmental reporting. European Management Journal, 23(6), 702–716. [CrossRef]

- Elisha, O. S., Ubi, J. J., Olugbemi, K. O., Olugbemi, M. D., & Emefiele, C. C. (2020). Forensic accounting and fraud detection in Nigerian universities (a study of Cross River University of Technology). Journal of Accounting and Financial Management, 6(4), 61–72.

- Esily, R. R., Chi, Y., Ibrahiem, D. M., Houssam, N., & Chen, Y. (2023). Modelling natural gas, renewables-sourced electricity, and ICT trade on economic growth and environment: evidence from top natural gas producers in Africa. Environmental Science and Pollution Research, 30(19), 57086–57102. [CrossRef]

- Feliciano, C., & Quick, R. (2022). Innovative information technology in auditing: auditors’ perceptions of future importance and current auditor expertise. Accounting in Europe, 19(2), 311–331.

- Fouziah, S. N., Suratno, & Djaddang, S. (2022). Fraudulent Financial Statement Detection Based on Hexagen Fraud Theory ( Study on Banking Registered in IDX Period. Budapest International Research and Critics Institute-Journal (BIRCI-Journal), 5(3), 28251–28264.

- Gaaya, S., Lakhal, N., & Lakhal, F. (2017). Does family ownership reduce corporate tax avoidance? The moderating effect of audit quality. Managerial Auditing Journal, 32(7), 731–744. [CrossRef]

- Halbouni, S. S., Obeid, N., & Garbou, A. (2016). Corporate governance and information technology in fraud prevention and detection: Evidence from the UAE. Managerial Auditing Journal, 31(6–7), 589–628. [CrossRef]

- Hammersley, J. S. (2011). A review and model of auditor judgments in fraud-related planning tasks. Auditing, 30(4), 101–128. [CrossRef]

- Handayani, B. D., Rohman, A., Chariri, A., & Pamungkas, I. D. (2020). Corporate financial performance on corporate governance mechanism and corporate value: Evidence from Indonesia. Montenegrin Journal of Economics, 16(3), 161–171. [CrossRef]

- Handoko, B. L., Lindawati, A. S. L., & Mustapha, M. (2020). Application of computer assisted audit techniques in public accounting firm. International Journal of Management, 11(5).

- Handoko, B. L., Putri, R. N. A., & Wijaya, S. (2022). Analysis of Fraudulent Financial Reporting based on Fraud Heptagon Model in Transportation and Logistic Industry listed on IDX during Covid-19 Pandemic. ACM International Conference Proceeding Series, 56–63. [CrossRef]

- Hassan, S. W. U., Kiran, S., Gul, S., Khatatbeh, I. N., & Zainab, B. (2023). The perception of accountants/auditors on the role of corporate governance and information technology in fraud detection and prevention. Journal of Financial Reporting and Accounting. [CrossRef]

- Kaur, B., Sood, K., & Grima, S. (2023). A systematic review on forensic accounting and its contribution towards fraud detection and prevention. Journal of Financial Regulation and Compliance, 31(1), 60–95.

- Khadim, Z., Batool, I., Akbar, A., Poulova, P., & Akbar, M. (2021). Mapping the moderating role of logistics performance of logistics infrastructure on economic growth in developing countries. Economies, 9(4). [CrossRef]

- Khairi, K. F., Samat, M. S. A., Laili, N. H., Sabri, H., Basah, M. Y. A., Haris, A., & Mirza, A. A. I. (2020). Takaful protection for mental health illness from the perspective of Maqasid Shariah. International Journal of Financial Research, 11(3), 168–175. [CrossRef]

- KNKG, K. N. K. G. (2008). Pedoman sistem pelaporan pelanggaran-spp (whistleblowing system-WBS).

- Lari Dashtbayaz, M., Salehi, M., & Hedayatzadeh, M. (2022). Comparative analysis of the relationship between internal control weakness and different types of auditor opinions in fraudulent and non-fraudulent firms. Journal of Financial Crime, 29(1), 325–341. [CrossRef]

- Lois, P., Drogalas, G., Karagiorgos, A., & Tsikalakis, K. (2020). Internal audits in the digital era: opportunities risks and challenges. EuroMed Journal of Business, 15(2), 205–217.

- McMullen, D. A., & Sanchez, M. H. (2010). A preliminary investigation of the necessary skills, education requirements, and training requirements for forensic accountants. Journal of Forensic & Investigative Accounting, 2(2), 30–48.

- Meitasir, B. C., Komalasari, A., & Septiyanti, R. (2022). Whistleblowing System and Fraud Prevention: A Literature Review. Asian Journal of Economics, Business and Accounting, 22(18), 23–29.

- Milanie, F., Munandar, Saputra, J., Satria, I., Khaddafi, M., Iba, Z., & Muhammad, Z. (2019). The role of organizational justice in determining work satisfaction and commitment among civil servants in Aceh, Indonesia. International Journal of Innovation, Creativity and Change, 9(3), 181–192.

- Mniai, A., Tarik, M., & Jebari, K. (2023). A novel framework for credit card fraud detection. IEEE Access.

- Muterera, J. (2024). THE AUDITOR SELF-EFFICACY SCALE: MEASURING CONFIDENCE IN TECHNICAL SKILLS, TECHNOLOGICAL ADAPTATION, AND INTERPERSONAL COMMUNICATION. Finance & Accounting Research Journal, 6(3), 331–346.

- Nurcahyono, N., Hanum, A. N., Kristiana, I., & Pamungkas, I. D. (2021). Predicting fraudulent financial statement risk: The testing dechow f-score financial sector company inindonesia. Universal Journal of Accounting and Finance, 9(6), 1487–1494. [CrossRef]

- Oktaviany, F., & Reskino. (2023). Financial Statement Fraud: Pengujian Fraud Hexagon Dengan Moderasi Audit Committee. Jurnal Bisnis Dan Akuntansi, 25(1), 91–118. [CrossRef]

- Pathmasiri, B., & Piyananda, D. (2021). Key Determinants of Internal Auditors’ Usage of Computer Assisted Audit Techniques in Sri Lanka. International Journal of Accountancy, 1(2).

- Pinatik, S. (2021). The effect of auditor’s emotional intelligence, competence, and independence on audit quality. International Journal of Applied Business and International Management (IJABIM), 6(2), 55–67.

- Pramana, Y., Suprasto, H. B., Putri, I. G. A. M. D., & Budiasih, I. G. A. N. (2019). Fraud factors of financial statements on construction industry in Indonesia stock exchange. International Journal of Social Sciences and Humanities, 3(2), 187–196. [CrossRef]

- Prasasti, A. D., & Sari, Y. M. (2024). Professional Scepticism, Auditor Experience, and Self-efficacy on Audit Judgement. KnE Social Sciences, 33–46.

- Prasetiyo, Y., Riyani, E. I., & Nugraheni, N. (2024). Detection Accounting Fraud: Role Internal Auditor and Whistleblowing Data System in Study Literature. Indonesian Journal of Business Analytics, 4(2), 503–516.

- Purnamasari, P., Amran, N. A., & Hartanto, R. (2022). Modelling computer assisted audit techniques (CAATs) in enhancing the Indonesian public sector. F1000Research, 11.

- Rawat, R., Oki, O., Chakrawarti, R. K., Adekunle, T. S., Lukose, J. M., & Ajagbe, S. A. (2023). Autonomous artificial intelligence systems for fraud detection and forensics in dark web environments. Informatica, 47(9).

- Rezaee, Z. (2005). Causes, consequences, and deterence of financial statement fraud. Critical Perspectives on Accounting, 16(3), 277–298. [CrossRef]

- Rustiarini, N. W., & Sunarsih, N. M. (2017). Factors influencing the whistleblowing behaviour: A perspective from the theory of planned behaviour. Asian Journal of Business and Accounting, 10(2), 187–214.

- Rustiarini, N. W., Yuesti, A., & Gama, A. W. S. (2021). Public accounting profession and fraud detection responsibility. Journal of Financial Crime, 28(2), 613–627.

- Rydzak, W., Przybylska, J., Trębecki, J., & Sellitto, M. A. (2023). the Communication Gap and the Effect of Self-Perception on Assessment of Internal Auditors’ Communication Skills. Economics and Sociology, 16(2), 148–166. [CrossRef]

- Salehi, M., & Dastanpoor, Z. (2021). The effects of psychological factors on the performance of independent auditors in Iran. Current Psychology, 40(4), 1621–1630. [CrossRef]

- Saluja, S. (2024). Identity theft fraud-major loophole for FinTech industry in India. Journal of Financial Crime, 31(1), 146–157.

- Sánchez-Aguayo, M., Urquiza-Aguiar, L., & Estrada-Jiménez, J. (2021). Fraud detection using the fraud triangle theory and data mining techniques: A literature review. Computers, 10(10), 121.

- Saragih, A. D., & Dewayanto, T. (2023). Systematic Literature Review: Dampak Teknologi Big Data Analytics Dalam Mendeteksi Fraud Pada Bidang Audit. Diponegoro Journal of Accounting, 12(3).

- Sari, S. P., & Nugroho, N. K. (2021). Financial Statements Fraud dengan Pendekatan Vousinas Fraud Hexagon Model: Tinjauan pada Perusahaan Terbuka di Indonesia. Annual Conference of Ihtifaz: Islamic Economics, Finance, and Banking, 409–430.

- Sheldon, M. D., & Jenkins, J. G. (2020). The influence of firm performance and (level of) assurance on the believability of management’s environmental report. Accounting, Auditing and Accountability Journal, 33(3), 501–528. [CrossRef]

- Singh, P., Singla, K., Piyush, P., & Chugh, B. (2024). Anomaly Detection Classifiers for Detecting Credit Card Fraudulent Transactions. 2024 Fourth International Conference on Advances in Electrical, Computing, Communication and Sustainable Technologies (ICAECT), 1–6.

- Smith, G. (2005). Communication skills are critical for internal auditors. Managerial Auditing Journal, 20(5), 513–519.

- Sudirman, S., Sasmita, H., Djabir D, M., Krisnanto, B., & Muchsidin, F. F. (2021). Effectiveness of Internal Audit in Supporting Internal Control and Prevention of Fraud. Bongaya Journal for Research in Accounting (BJRA), 4(1), 8–15. [CrossRef]

- Tragouda, M., Doumpos, M., & Zopounidis, C. (2024). Identification of fraudulent financial statements through a multi-label classification approach. Intelligent Systems in Accounting, Finance and Management, 31(2), e1564.

- Widnyana, I. W., & Widyawati, S. R. (2022). Role of forensic accounting in the diamond model relationship to detect the financial statement fraud. International Journal of Research in Business and Social Science (2147- 4478), 11(6), 402–409. [CrossRef]

- Widuri, R., O’Connell, B., & Yapa, P. W. S. (2016). Adopting generalized audit software: an Indonesian perspective. Managerial Auditing Journal, 31(8/9), 821–847. [CrossRef]

- Yusuf, Y. Y., Gunasekaran, A., Musa, A., El-Berishy, N. M., Abubakar, T., & Ambursa, H. M. (2013). The UK oil and gas supply chains: An empirical analysis of adoption of sustainable measures and performance outcomes. International Journal of Production Economics, 146(2), 501–514. [CrossRef]

Table 1.

Measurement of variables.

| Variable | Measurement | Source |

|---|---|---|

| Forensic Accounting Skill | Analyzed by evaluating an auditor's ability to analyze financial data, communicate effectively, deal with pressure, and apply accounting and auditing knowledge to detect and investigate unauthorized actions. | (N. Chukwu et al., 2019) |

| Auditor's Self-Efficacy | It was analyzed by measuring three aspects: problem-solving ability, understanding of abilities, self-confidence, and perseverance. | (Bandura, 1988) |

| Generalized Audit Software Used | It is measured by considering several technological, organizational, accounting profession, client, personal, and external factors. | (Widuri et al., 2016) |

| Whistleblowing System | Includes policies, procedures, protection, follow-up, confidentiality, education, and evaluation to ensure effectiveness. | (KNKG, 2008) |

| Fraud Detection | Identifying potential fraud schemes through various methods such as data analysis, risk assessment, and investigation, as well as high levels of self-efficacy, are associated with increased confidence and motivation to perform audit tasks. | (Alfordy, 2022) |

Source: Results of secondary data processing, 2024.

Table 2.

Demographic characteristics of the respondents.

| Demographic characteristics | Demographic criteria | Frequency | % |

|---|---|---|---|

| Gender | 1 = Male 2 = Female |

370 203 |

64.5 35.5 |

| Age | 1 = <25 Years 2 = 25-35 years 3 = 36-45 years 4 = >45 Years |

51 127 209 186 |

8.8 22.2 36.5 32.5 |

| Certifications Held | 1 = CPA 2 = CIA 3 = CISA 4 = Other 5 = Non |

75 111 155 140 92 |

13.1 19.2 27.4 24.3 16.0 |

| Educational Level | 1 = Bachelor 2 = Masters 3 = PhD |

352 197 24 |

61.4 34.4 4.2 |

| Experience as an Auditor | 1 = <2 Years 2 = 2-5 years 3 = 6-10 years 4 = >10 Years |

32 167 251 123 |

5.6 29.1 43.8 21.5 |

Source: Results of secondary data processing, 2024.

Table 3.

Descriptive Statistics.

| Variable | N | Min | Max | Mean | Std. Deviation |

|---|---|---|---|---|---|

| TA | 573 | 10 | 29 | 21.3735 | 2.82412 |

| EC | 573 | 15 | 29 | 21.5201 | 2.65466 |

| PS | 573 | 15 | 31 | 21.6056 | 2.43045 |

| AAS | 573 | 14 | 31 | 21.5462 | 2.55226 |

| ASE | 573 | 21 | 32 | 27.1117 | 1.98722 |

| GAS | 573 | 23 | 40 | 37.1065 | 2.32894 |

| WBS | 572 | 21 | 35 | 29.2675 | 2.75315 |

| FD | 573 | 22 | 36 | 30.0227 | 2.89825 |

| Valid N (listwise) | 572 |

Source: Results of secondary data processing, 2024.

Table 4.

Results of model fit test.

| Model Fit and Quality Index | Index | Criteria | Results |

|---|---|---|---|

| Average Path Coefficient (APC) | 0.197 | P>0.001 | Fit model |

| Average R-Square (ARS) | 0.418 | P>0.001 | Fit model |

| Adjusted R-Squared Mean | 0.415 | P>0.001 | Fit model |

| Average Block Variance Inflation Factor (AVIF) | 3.013 | if <= 5, ideally <= 3.3 |

Fit model |

| Average Full Collinearity VIF (AFVIF) | 2.891 | if <= 5, ideally <= 3.4 |

Fit model |

| Tenenhaus GoF (GoF) | 0.505 | small >= 0.1, medium >= 0.25, large >= 0.36 |

Fit model |

| Simpson's Paradox Ratio (SPR) | 0.857 | acceptable if >= 0.7, ideally = 1 | Fit model |

| R-Squared Contribution Ratio (RSCR) | 0.972 | acceptable if >= 0.9, ideally = 1 | Fit model |

| Statistical Suppression Ratio (SSR) | 1.000 | acceptable if >= 0.7, ideally = 1 | Fit model |

| Nonlinear Bivariate Causality Direction Ratio (NLBCDR) | 1.000 | acceptable if >= 0.7, ideally = 1 | Fit model |

Source: Results of secondary data processing, 2024.

Table 5.

Hypothesis Summary.

| Hypothesis | Path coefficients | Criteria | P Value | Decision | |

|---|---|---|---|---|---|

| H1 | TA → ASE | - 0.033 | <0.05 | 0.211 | Rejected |

| H2 | EC → ASE | 0.272 | <0.05 | <0.001 | Accepted |

| H3 | PS → ASE | 0.228 | <0.05 | <0.001 | Accepted |

| H4 | AAS → ASE | 0.382 | <0.05 | <0.001 | Accepted |

| H5 | ASE → FD | -0.344 | <0.05 | <0.001 | Accepted |

| H6 | GAS → FD | -0.081 | <0.05 | 0.025 | Accepted |

| H7 | WBS → FD | 0.042 | <0.05 | 0.159 | Rejected |

Source: Results of secondary data processing, 2024.

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2024 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.