Submitted:

14 November 2024

Posted:

15 November 2024

You are already at the latest version

Abstract

This study investigates whether a model combining financial ratios and non-financial variables can predict audit opinions (qualified or unqualified) for firms listed on the Athens Exchange (ATHEX) from 2018 to 2022. Using 450 firm-year observations from 90 non-financial firms, we applied a probit regression model to examine the impact of 11 financial ratios and non-financial factors such as auditor quality, auditor turnover, and corporate performance. Our findings reveal that financial ratios and auditor characteristics, particularly auditor quality, have significant explanatory power in determining audit opinions. The model offers practical benefits for auditors, enabling them to predict audit opinion types, assess client risks, define audit scope, and reduce litigation risks. These insights are particularly relevant in emerging economies like Greece, where audit risk and firm failures are heightened. The study highlights the importance of financial and non-financial variables in identifying material misstatement risks, consistent with International Standards on Auditing (ISA 520). However, its findings are limited by the small sample size and Greece's specific economic and regulatory context. Future research should explore the model’s applicability to larger and more developed markets.

Keywords:

Audit

; Accounting

; Governance

; Greece

; Going-concern

; Athens Exchange

1. Introduction

Auditing is the accumulation and evaluation of evidence about (financial mainly) information to determine and report on the degree of “similarity” between this information and specific “criteria” [1,2,3]. Audit companies reduce information asymmetry and, therefore, agency costs; Hellas is a code-law country criticized for the inadequate quality of financial and auditor reporting, especially before the implementation of International Financial Reporting Standards (IFRS) on 1 January 2005 listed in the Athens Exchange (www.athexgroup.gr) companies.

The increasing incidence of audit failure increased the need for transparency in exercising professional judgment and communication of audit findings. After each audit, the external auditor issues a report that includes her/his independent professional opinion on whether or not the financial statements show “a true and fair view” for the specific period following the International Financial Reporting Standards (IFRS). The audit report, therefore, serves as a tool that a) increases financial statements’ users’ confidence and b) enhances the reliability of financial statements. The auditor’s report is short and standardized; the external auditor has inside and better financial information, and he/she has the professional experience to evaluate the company's financial position.

Auditors’ reputations are in danger if several material misstatements in their clients’ (mainly financial) data are undetected and/or misreported; in addition, they face the stress of litigation and its material costs [4,5,6].

The global financial crisis has significantly increased firm failures (accounting/auditing scandals), increasing interest in auditor reporting. In addition, the firm’s directors and the auditing profession have been subject to increased scrutiny because of litigations [7]. Specifically, auditors’ incentives “to detect insider expropriation vary across jurisdictions, particularly those incentives related to the penalties for failure to detect expropriation” [8]. Lastly, as larger or minor firms continue to collapse in various parts of the world and the Hellenic capital market (i.e., Folli Follie in Greece), research has shown that major financial reporting scandals cannot be eliminated [9], p. 504.

In this direction, the International Auditing and Assurance Standards Board (IAASB) issued International Standards on Auditing No. 701 (ISA 701), effective from the 2016 audits. An important feature of this standard is the mandatory requirement for every external auditor to select and disclose Key Audit Matters (KAM). The main objective of the disclosure of KAM is to increase the communicative value of the audit report, reduce information asymmetry between the auditor and users of audited financial statements, and increase investors’ understanding of the auditor’s role and responsibility. In addition, investors, knowing “the risk of expropriation, penalize firms in less protective environments …. without detection of expropriation by insiders, the degree of investor protection provided in other forms is significantly weakened” [8].

ISA 701 defines key audit matters as “those that, in the auditor’s professional judgment, were of most significance in the audit of financial statements of the current period” [10].

This study differs from similar ones [11,12], for Brazil as it focuses on analyzing data from Greek companies listed on the Athens Exchange (www.athexgroup.gr).

In general, users of financial statements demand more qualifications in auditor reports as warning signals of business failure; auditors’ reports are generally regarded as “insufficient” in giving early warnings about the bankruptcy/involuntary delisting of many listed companies in the Athens Exchange from 2004 to 2018 [13].

External users (i.e., investors, creditors, and governments) rely heavily on financial information provided by the firm’s management to make reasonable decisions. However, there exists a “conflict” (according to agency theory) between A) users’ needs and B) management’s purposes. For that reason, external auditing is used as an instrument to increase the quality, reliability, and credibility of a firm’s financial reporting.

Specifically, an unqualified auditor report means that financial statements (provided by the firm’s accounting environment): A) have been prepared following International Financial Reporting Standards (that comply with Greek Accounting Standards) and B) “give a true and fair view” for the company’s activities. In addition, issuing a wrong audit opinion because the auditor cannot identify Falsified Financial Statements (FFS) can have serious negative consequences for the auditors’ reputations.

In particular, given the specific attributes of the Hellenic capital market, we emphasize the theoretical premises of Agency Theory and the potential relationship costs arising from the conflicts of interest between agents and principals, which are defined as the sum of A) monitoring expenditures incurred by principals (i.e., owners, shareholders) to reduce the “opportunistic” behavior of the agent (including incentive systems and costs to monitor agent’s behavior), B) bonding and motivation costs incurred by agents-management (i.e., obligation or commitment costs to get principal’s trust) and C) the residual loss incurred by the principal.

This paper aims to develop a model, which could identify the specific financial ratios that could predict audit opinions using a logit model.

Several characteristics of the Greek market should be taken into consideration. Specifically, Hellas is considered “a low-trust society marked with a strong preference for state regulation” [14], p. 53. In addition, A) financial reporting is closely related to taxation, B) there is low Corporate Governance (C.G.) performance and weak investor protection, C) under-developed capital market and low market for corporate control (in which firms have low ownership dispersion and there is no clear distinction between management and ownership) and D) low quality of external auditing [15,16,17,18] and f) periods of “hot”/”cold” Initial Public Offering (I.P.O.) activity [19].

The financial scandals in Hellas and the huge number of (involuntary, mainly) delistings due to financial problems increased public worries regarding the quality of audit work and the independence of auditors from company management.

The results of this research can be useful for auditors to predict which audit opinion should be issued for each specific company and to control for audit quality to reduce possible lawsuits to auditors [20].

According to International Standards of Audit (ISA) 700, the main purpose of auditing is to certify that the financial statements produced by the company’s management are: A) following the applied International Financial Reporting Standards (IFRS) and B) free from material misinterpretation because of either fraud or error.

The rest of the paper is organized as follows: in the next section, we provide and analyze the theoretical framework regarding financial ratios (“analytical procedures” in auditing methodology) and auditors’ opinions. The third section examines the related research regarding qualified auditor reports and their financial indicators. The fourth section describes our methodology, model, and variables. In the fifth section, we express our findings, and in the sixth section, we conclude.

2. Materials and Methods

2.1. Theoretical Framework—Analytical Procedures—Financial Ratios

According to [9], p. 505, “an audit failure or audit scandal is either a failure to comply with auditing standards or a mismatch between auditing standards and what the stakeholders expect auditors to do or be able to do.” Financial reporting is used to reduce information asymmetry, but as there are cost and benefit considerations information asymmetry cannot be fully reduced [21].

Reliable information disclosure is one of the major accounting principles, based on which all information related to business activities should be available appropriately and timely for financial statement users to make specific investment decisions. Financial statement users utilize this (mainly financial) information for different purposes, including comparing business firms' operations from the same or different sectors or firms’ performance with previous years.

The statutory auditor bases his/her opinion on A) completeness, B) consistency, and C) reliability of the financial data (produced by the company) and then describes the findings that are not in line with i) faithful representation and ii) compliance to accounting standards. In addition, the auditor examines the “qualitative” characteristics of the auditee’s internal control procedures and whether management implements sound financial estimates.

According to the signaling theory, firms try to send financial statement users positive signals (e.g., profits) to prevent the publication of bad news. The analysis of the auditor report's influence on capital markets is based on two factors: A) the analysis of the audit opinion Key Audit Matters (KAM) and B) the analysis of audit quality (auditor from Big-4 or not) [22,23,24,25,26,27].

According to agency theory, [28] proposed that in the industrial world, in big companies, there is a divergence of interests between owners (i.e., principals) and their agents (i.e., management). Both the principals and agents are assumed to be motivated by self-interest and economically rational; under these circumstances, management (i.e., agents) tries to maximize the firm’s (short-term mainly) financial performance, which may not be beneficial to the long-term strategy of owners.

Therefore, auditors, as independent third parties safeguarding owners-shareholders’ best interests, examine the financial statements (produced by management) and provide an opinion regarding their fairness. In addition, they issue a going-concern audit opinion if they find major errors in financial statements that could jeopardize the company’s ability to survive.

The problem of readability of an auditor’s report has focused on a) the evidence of its determinants, b) observing its implications concerning audit quality, c) the effect on the cost of capital, and d) the adoption of IFRS. In this view, [29] found a strong negative relationship between a firm’s size and its financial statements’ readability; in addition, [30] shows that firms with weak performance (low profitability) should present “lengthy” financial reports that may reduce their readability.

Analytical procedures include A) ratio analysis, B) reasonableness test, and C) trend analysis (a form of ratio analysis); the first one is a form of financial statement analysis and is widely used to quickly examine a company’s financial performance in terms of profitability, debt, and asset management, among other things.

Another use of ratio analysis is to compare a firm’s financial performance with the industry average; in addition, ratios are used by external users of financial information (for example, investors) to evaluate a company’s financial health [31,32,33].

Profitability ratios are the main indicators of a company’s economic success. Profitability is the main goal for all companies, and financial analysts need to measure and compare past and current profitability to predict future profitability.

This paper analyzes the effect of liquidity, profitability, and financial leverage ratios in predicting auditor opinion. For example, high financial leverage ratios indicate high financial risk, as the company will have to pay (from its profits) the interest on the debt. In addition, failure to meet a (strict) debt covenant will risk the company's existence.

In our sample, we included firms with going-concern audit qualifications, financially stressed companies, and companies with other Key Audit Matters (KAM) (such as depreciation and bad debts provision). In Athens Exchange, only a few listed companies received going-concern qualification (less than 15%).

2.2. Previous Research Regarding Qualified Auditor Reports and Their Indicators

2.2.1. Internationally

Using discriminant analysis, [34] was among the first to examine the relationship between auditor opinion and publicly available information. Specifically, based on accounting ratios, he concluded that accounting ratios help auditors to issue a relevant audit opinion. Similarly, [35] examined the association between audit report qualifications and financial failure using a log-linear approach and univariate and two multivariate models. The univariate model shows a significant association between bankruptcy and going concern and other auditors’ qualifications for the year before bankruptcy. Similarly, multivariate models, which use combined auditor report variables, show a link between business failure for going concern and other subject-to-qualifications. Finally, when they test audit report variables with a set of ratios comprising a bankruptcy-prediction model, consistency and going-concern qualifications are strongly associated with bankruptcy.

In the same research path, [36] examined the information content included in auditors’ qualified opinions (with going-concern qualification) by using abnormal stock returns (measured as the market model residuals) near the release of auditors’ reports, using a sample (for the period 1979-1988): A) 68 qualified and B) 86 unqualified audit reports. The results of the ordinary least squares method showed that mean abnormal returns are negative, surrounding the release of going-concern qualifications auditor reports. At the same time, they are positive for distressed firms that receive an unqualified auditor report. This shows, in practice, that auditors’ going-concern qualification includes information for market participants, as there are abnormal stock returns in the period that surrounds the auditor’s opinion. Specifically, the study examines the stock market reaction to auditors’ qualified report (with going-concern qualification) by using investors’ expectations that a firm will receive a going-concern qualification. A logit model that used accounting and market data and other information available to market participants (i.e., investors, banks, stock market supervisory bodies) estimated their expectations.

Using multivariate logistic regression in the UK, [37] examined financial, organizational, and auditor variables to explain small companies’ audit qualifications. Their results showed that companies audited by a) Big-4 audit firms, b) have prior year qualification, c) earnings reduction, and d) few non-director shareholders have a higher likelihood to receive a qualified audit opinion.

According to [38], 37 companies were listed on the Helsinki Stock Exchange (HeSE) for the period between 1999 and 1994 (111 audit reports). From their sample, only 11 auditor reports had qualification(s), which refer to three companies. They used univariate analysis and multivariate logistic model; the first showed that a qualified auditor report is associated with low profitability, negative growth, and a high debt ratio. Regarding the multivariate model, the likelihood of a qualified auditor report is negatively linked with the firm’s growth, the amount of share capital in the balance sheet, and the firm’s employee number.

Similarly, [39] examined how models based on market and financial variables can predict auditors’ decisions and issue qualified audit reports in specific situations. They applied a probit model with a dependent variable, the possibility of a firm receiving a qualified or not opinion. Their model is between A) unqualified and first-time qualifications and B) qualifications (i.e., going concerned, multiple qualifications). Their results showed that current-year losses, stock minus industry returns, and the change in the ratio of receivables to total sales are the most important variables that predict auditors’ qualifications. In addition, their model has the highest accuracy rate in predicting going concern opinions.

In addition, [40] examining firms with financial distress found that they are likely to receive adverse audit opinions, and smaller audit firms do not use a lower rate of adverse audit opinions than larger ones. [41] examined the specific financial characteristics of firms listed on the Singapore Stock Exchange that received audit qualifications for the first time, using a matched pair analysis as a control. Their results showed that these firms are significantly less liquid, less profitable, and have more debt than the control firms have in the qualification year. In addition, auditor’s report qualification is highly associated with the firm’s ownership and auditor type; regarding accounting data, there is a significant link between qualification and change in accounting methods or assets’ revaluation.

[42] summarized the main techniques for business failure prediction used in around 50 of the 160 most important articles published from 1932 until 1994 in various accounting and finance journals. They found that the main methods used were A) discriminant and B) logit analyses.

[43] tested the effectiveness of A) artificial neural networks, B) expert systems, and C) multiple discriminant analysis in predicting the type of audit opinion in ninety firms listed in the American and New York Stock Exchanges. They found that artificial neural networks are more useful in determining auditors’ opinions.

[44], Using a sample of 144 US firms for up to five years before failure, MultiCriteria Decision Aid (MCDA) and linear discriminant and logit analyses were examined. Their MCDA models were significantly efficient in predicting business failure (the error rate was around 20% for up to five years before failure). In a similar vein, [45] examined a sample of around 1.000 small UK firms, half of which failed between 1997 and 2004 and using discriminant and logit analyses (UTilities Additives Discriminates-UTADIS and Multigroup Hierarchical DIScrimination-MHDIS), as well as Support Vector Machines (SVM).

In another research type, [46] used a Support Vector Machine (SVM) to develop linear and non-linear models for a sample of 5,189 unqualified and 859 qualified audit reports from the UK from 1988-2003. They found that non-linear (i.e., Radial Basic Functions-RBF) models did not provide improved results compared to simpler linear models. In contrast, all SVM models could distinguish between qualified and unqualified audit reports with significant accuracy.

[47] examined whether, using multicriteria decision aid models, we can predict, as accurately as possible, auditors’ opinions (i.e., qualified or not). Their sample included 625 qualified and 625 non-qualified audit reports from UK-listed manufacturing firms from 1998 until 2003. Τhis study was the first with UK data that examined various ownership types of listed firms; they used two multicriteria methods (UTilities Additives Discriminates-UTADIS and Multigroup Hierarchical DIScrimination-MHDIS), and four financial variables were included in these models, based on a combination of auditor’s opinion, a correlation analysis, and a univariate statistical test. They found that these two models could, successfully and accurately, distinguish which companies will receive unqualified or not opinions.

[48] used data mining techniques (i.e., C4.5 Decision Tree, Multilayer Perception Neural Network, and Bayesian Belief Network) in a sample of 450 publicly listed, non-financial UK and Irish firms. They selected 26 financial ratios and found that profitability and Z-score explain the type of audit opinion (qualified or not).

[49] used a sample of A) 264 financial statements that received qualified and B) 3.069 financial statements that received unqualified auditor opinions over 1997-2004 from 881 firms listed on the London Stock Exchange. Their analysis was based on financial and non-financial variables (27 in total). It used principal component analysis to construct a solid set of independent variables that could interpret qualified financial statements. They found that Probabilistic Neural Networks had significant explanatory power in predicting qualified audit reports.

Another article [50] used a sample of 1.455 private and public UK companies and 5.276 financial statements, from which 980 received qualified audit opinions. They developed two industry-specific models (one without financial variables and the other with financial variables) and a general one using data from 1998 until 2001, which were tested during the period 2002 to 2003. Their results were inconclusive regarding the development of industry-specific models, as opposed to general models.

[51] used the logit model and discriminant analysis to identify the main factors related to audit opinion. Their sample was 275 listed firms, and their model included eleven accounting ratios. They concluded that the logit model is more relevant and could predict financially troubled firms.

[52], examining the Iranian stock market (Tehran Stock Exchange-TSE), using data mining procedures (i.e., Support Vector Machine) with a decision tree, and trying to predict and identify the specific auditor opinion type. Their sample included the period 2001-2007, and their results, obtained from 30 rules with 20 variables, could assist auditors in issuing the appropriate audit opinion (i.e., qualified or not). In the same stock market, [53] focused on the cash flow statement, examining five cash flow ratios, to predict audit opinion; they used data from 2003-2010. They asserted a positive relationship between unqualified audit reports and cash flow amounts.

[20], using a sample of 110 firm-year observations (including 55 qualified and 55 non-qualified) from the Istanbul Stock Exchange for the period 2010-2013, together with discriminant, logit, and C5.0 decision tree, based on 12 financial ratios, found that: A) retained earnings to total assets, B) equity to total liabilities, C) net income to total assets are the most significant indicators to identify the specific audit opinion (qualified or not).

[54], used annual reports for 2015-2019 from a sample of 33 firms listed in the Indonesian Stock Exchange to determine the factors affecting the auditors’ going-concern opinion. Their results showed that profitability and liquidity negatively affect the going-concern audit opinion, whereas leverage positively does; firm size and audit report lag do not have a material effect on going-concern audit opinion.

2.2.2. Research in the Hellenic Context

Hellas industrialized after World War II, and although it had very rapid growth in the first decade, it faced structural economic problems and stagnation; this was the case until 2002 when Hellas entered the European Monetary Union (E.M.U.). After that, it had a stable macroeconomic environment with low currency risk; in addition, the Athens Stock Exchange (A.S.E.), from 1996 till the beginning of 2000, showed the highest growth of any capital market in the developed world. In addition, the number of listed companies increased substantially, and A.S.E. was upgraded to a mature capital market in 2001.

The development of accounting, auditing, and corporate environment in Hellas can be linked to A) cultural factors, B) the family structure of business, C) law, D) political, and E) institutional factors [55]. Regarding the Accounting Plan, the influence of the French legal code was significant in Greek laws (from 1835 till 2005, when International Financial Reporting Standards were introduced) [56]. In addition, Hellas/Greece has many socio-political features that distinguish this country from other European countries; for example, Hellas presented one of the lowest ownership dispersion percentages among civil law countries, with more than 60% ownership concentration [57].

In most small and medium-sized listed companies, the decision-making and administration processes are mainly controlled by big (mainly family) shareholders. At the same time, larger firms have higher dispersion in market capitalization. Additionally, Corporate Governance in Hellas follows the insider model, which is characterized by A) high (mainly family) concentration of ownership, B) few independent committees, C) limited disclosure, and D) weak minority investor protection [15,58,59,60,61,62].

As owners are actively involved in management and banks mainly provide (external) finance, reliable financial information is less needed to make important investment and financial decisions. Therefore, regarding earnings management, [63,64] found that Hellenic-listed companies manipulate their accounting numbers more than other European countries.

Surprisingly, the number of listed firms in Athens Exchange (www.athexgroup.gr) has been diminishing yearly since 2000; specifically, from 350 listed companies in 2000 to around 170 at the end of 2022).

[65] examined whether financial and non-financial information can be used to predict the qualifications in auditors’ reports; the sample consisted of 100 Greek-listed companies, and using logistic and ordinary least squares regression models, he assessed the effect of company litigation and financial information on audit qualification opinions. The model showed around 80% accuracy in predicting qualified auditor reports, while its main significant variables are financial (i.e., financial distress) and non-financial (i.e., company litigation). Additionally, [66], to explain the audit qualifications listed in the Athens Exchange firms, developed a model with multicriteria decision aid classification method (UTADIS-UTilities Additives Discriminates) and compared its results with other multivariate statistical techniques (i.e., discriminant and logit models). Specifically, their results showed that high receivables, low net profit to total sales, and low working capital to total sales play the most significant part in explaining auditors’ qualified reports.

[67] tested financial and non-financial variables that could affect audit qualifications; they used a logistic model in a sample of 185 listed firms. Their results showed that the current ratio and the operating margin to total assets relate significantly to audit opinion. In a similar vein, [68] examined the relationship between earnings management, as measured by signed discretionary accruals, and A) auditor reporting, measured by audit firm size (Big-4 or not), and B) audit opinion (unqualified vs qualified).

3. Methodology

3.1. Sample

The total population included all non-financial firms listed in Athens Exchange (https://www.athexgroup.gr/el/web/guest/companies-map) during the period 2017 -2022; from those firms, we included firms that:

- Had Fiscal year-end 31 December

- Were not listed in another capital market (dual listing)

- Were not in the real estate, holding, and in surveillance categories/sectors

- Had all variables examined for all years (non-missing data)

- Had annual reports on their websites for all years

- The sample included 90 companies from 2018 to 2022, a total of 450 observations.

3.2. Model—Logistic Regression

As the dependent variable (qualified or not audit opinion) is categorical and binary (i.e., zero for qualified opinion and one otherwise) and the independent variables are financial (i.e., ratios) and non-financial, the appropriate research method is logistic regression.

3.3. Variables

- Independent variables

Three financial variables (gross profit to sales ratio, debt ratio, and current ratio) and three non-financial/binary variables (audit firm type, auditor turnover, and corporate performance/profitability).

Audit firm type (audit quality) indicates the auditor report's reliability; big-4 international audit firms are expected to provide higher-quality audits [71,72,73]. In our analysis, we consider the following high-quality audit firms: A) big-4, B) Grant Thornton, and C) SOL-Crowe (a local audit firm).

Regarding profitability, companies that show lower profitability are more likely to receive a going-concern audit opinion, as poor financial conditions can raise doubts about their business continuity [38,74].

As far as liquidity is concerned, firms with better liquidity can meet their short-term financial obligations by using their current assets; in contrast, companies with poor liquidity may have financial difficulties paying their short-term debts, which is highly regarded as a critical point for a going-concern opinion [65,75,76].

Firms facing financial problems (usually having a high ratio of debt to total assets) are typically motivated to engage in fraudulent activities; for example, research has shown that there is a positive relationship between the level of debt and the probability of Falsified Financial Statements (FFS) [48,77,78,79,80,81].

- 2.

- Dependent variable

The dependent variable divides the total sample group into two categories according to the type of auditor opinion; specifically, the dependent variable is zero when the opinion is qualified and one when it is not qualified.

- 3.

- Control variables

To measure more accurately the specific relationship between financial and non-financial variables and auditor opinion, we control using a set of eight other variables (i.e., quick ratio, inventory turnover ratio, fixed asset turnover ratio, total asset turnover ratio, Return On Assets-ROA, Return On Equity-ROE, net profit ratio, and market value to book value ratio).

4. Research Findings

Table 1 presents the frequency distribution of qualitative independent and dependent variables (i.e., qualified opinion, auditor turnover, audit firm type, and corporate performance) from 2017 to 2022 (90 companies per year for 6 years, meaning 540 audit reports).

In our research, we find that the six-year qualification rate in Hellenic listed companies of the sample is around 5%; in Table A, we show the rates from similar research internationally.

Table A.

Qualification rates in similar research articles

| Author(s) | Year | Country | Sample – (years) – Total sample | Qualification rate |

| [85] | 2017 | Tunisia | 76 firms – (2005-2015) – 545 audit reports | 30% |

| [20] | 2015 | Turkey | 55 qualified & 55 unqualified – (2010-2013) | Matching sample |

| [1] | 2017 | Turkey | 263 firms audit reports – 2016 | 10% |

| [67] | 2006 | Hellas | 185 firms – 2001 – 162 received a qualified opinion | 90% |

| [68] | 2012 | Hellas | 322 firms – (2005-2009) – 978 audit reports | 38% |

| [22] | 2015 | Romania | 55 firms – 2012 | 35% |

| [88] | 2016 | Turkey | 90 qualified & 90 unqualified (2005-2014) | Matching sample |

Table 1.

Distribution of the sample (90 listed firms)

| Industry | No. of listed companies | % |

| Construction & Construction Materials | 10 | 11.1% |

| Consumer products | 5 | 5.6% |

| Energy/Refineries & Oil Trading | 4 | 4.4% |

| Food, Drinks, Tobacco | 8 | 8.9% |

| Health | 3 | 3.3% |

| Industrial Products | 7 | 7.8% |

| Industrial Products & Services | 13 | 14.4% |

| IT | 7 | 7.8% |

| Media/Publications | 1 | 1.1% |

| Personal Care, Medicines | 3 | 3.3% |

| Raw materials | 14 | 15.6% |

| Telecommunications | 1 | 1.1% |

| Trade | 5 | 5.6% |

| Travel & Leisure | 6 | 6.7% |

| Utilities | 3 | 3.3% |

| All industries | 100.0% |

The descriptive statistics of qualitative independent and dependent variables (i.e., qualified opinion, auditor turnover, audit firm type, and corporate performance) from 2017-2022 (90 companies per year for 6 years, meaning 540 audit reports) are presented in Table 2. Specifically, Table 2 reports the mean, median, max, min, and std. deviation, skewness, kurtosis, as well as the statistic-value and p-value of the Jarque-Bera of the dependent variable, independent variables and control variables.

Audit quality is less than half of the sample, with high variability within the Athens Exchange. Regarding explanatory (independent) variables, there are binary (D, E, and F) and non-binary (A, B and C) variables. The highest and lowest non-binary explanatory variables (i.e., ratios) are current (A) and debt (B) ratios, respectively. Audit firm (D) has the highest frequency of occurrence and variability among all binary explanatory variables. The inventory turnover ratio (H) has the highest value and variability among all control variables ratios. The average Ben and Altman scores are close to but higher than 2. Skewness and excess kurtosis values reveal close to normal distribution for all variables (dependent, independent, and control). Such results are also evident from the Jarque-Bera test. The null hypothesis of the normal distribution is not rejected for all variables (dependent, independent, and control).

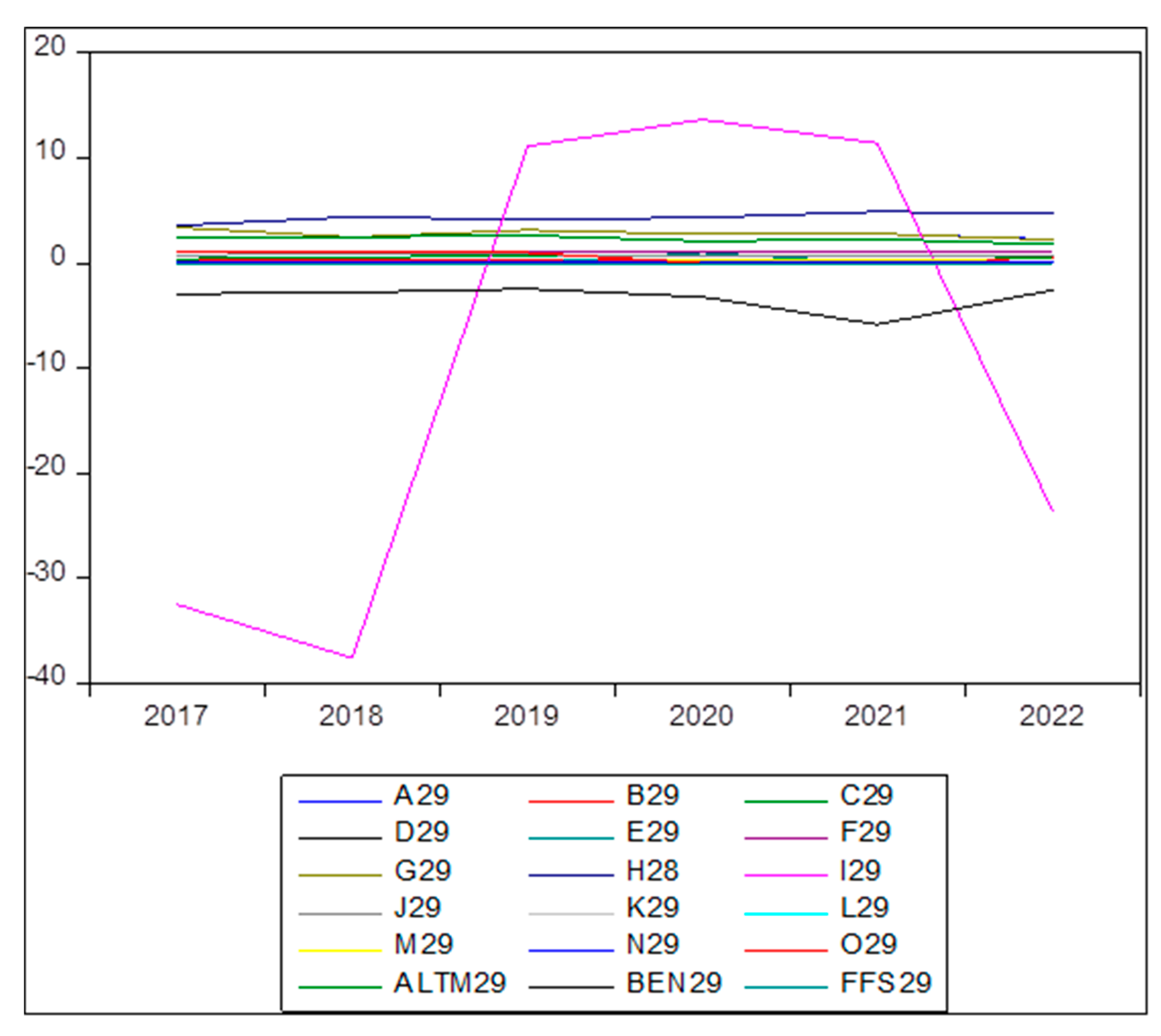

Figure 1.

The time evolution of the dependent variable, independent variables, and control variables across the sample. Notes. The figure graphs the average values of each variable across the most important (in terms of audit quality) firms (in number: twenty-nine).

Figure 1.

The time evolution of the dependent variable, independent variables, and control variables across the sample. Notes. The figure graphs the average values of each variable across the most important (in terms of audit quality) firms (in number: twenty-nine).

Only the fixed asset turnover ratio (I29) has extreme values. The audit quality (FFS29) has a significant slowdown for 2021, with getting back to average next year, 2022, however. Analyzing the relation between audit quality and independent and control variables starts with hypothesis testing. Two hypotheses are tested. The null hypothesis for each of the two, follows:

H1:

The Audit quality (dependent) variable Granger causes each of the independent or control variables.

H2:

Each of the independent or control variables Granger cause the Audit quality (dependent) variable.

Table 3 reports the F-statistic and p-value for each of the above hypotheses.

The first hypothesis is rejected only for debt ratio (B) from independent variables; and, quick ratio, market value to book value ratio and Altman score (G, N and Altm) from control variables. Statistical significance is answered in either 5% or 10% level. The second hypothesis is rejected for none of independent variables and two control variables: ROA and ROE (K and L). The role of independent variables is not to Granger cause audit quality; moreover, there is only one of them (B) which is Granger caused by audit quality. Furthermore, the role of control variables is more important in audit quality; in terms of hypothesis testing. Audit quality Grange cause three control variables (G, N and Altm); while, two control variables Granger cause audit quality (K and L).

Table 4 reports the average pairwise correlations and the respective p-values of significance t-testing in correlations between Audit quality and each independent (variables A to F) or control (variables G to N; as well as Ben and Altm scores) variables, across all firms.

Most of variables, are negatively correlated with audit quality; as expected. There is no statistically significant correlation between any independent variable and audit quality. In terms of control variables, total asset turnover, ROE, net profit, and MV/BV ratios are significantly correlated with audit quality (J, L, M and N). Regarding the significant correlations, total asset turnover and net profit ratios (J and N) are positively correlated with audit quality; while, ROE and MV/BV ratios (L and M) are negatively correlated.

The final way to examine the in-sample prediction of audit quality from independent and control variables is regression. We experimented with OLS and logit regressions. The results are reported in Table 5. These, average across all firms, results are the best (with the most significant coefficients) among the two estimation methods. In most of firms, the OLS estimation method gave us the most significant results.

Most of the variables negatively explain audit quality, as expected. In terms of independent variables, only the gross profit margin ratio (C) statistically significantly explains audit quality. It also explains it negatively, as expected. In terms of control variables, inventory turnover, total asset turnover, Return On Assets (ROA), Return On Equity (ROE), and net profit ratios, as well as Altman score, most of those negatively explain audit quality, as expected.

5. Conclusions

This study provides valuable insights into the factors influencing audit opinions for companies listed on the Athens Exchange, focusing on the relationship between financial ratios, non-financial variables, and the likelihood of receiving a qualified audit opinion. Our findings offer a nuanced understanding of how these elements interact in an emerging market context by analyzing key indicators such as profitability, liquidity, leverage, and auditor quality.

One of the central findings is the significance of audit quality, with Big-4 firms and other high-reputation auditors associated with more reliable and transparent audit opinions. At the same time, companies facing financial distress—evidenced by high leverage or low liquidity—are more likely to receive qualified opinions. These results align with global trends while also reflecting the unique characteristics of the Greek audit environment, such as its smaller market size and concentrated ownership structures.

The study has practical implications for both auditors and regulators. Auditors can use the model developed here to evaluate potential clients, better plan engagements, and anticipate litigation risks. Regulators, on the other hand, can draw on these findings to strengthen auditing standards and governance practices, particularly in markets prone to higher audit risks.

However, the study’s scope is not without limitations. The relatively small sample size, reflective of the limited scale of the Athens Exchange, means the findings may not fully generalize to larger, more complex markets. Additionally, the research focuses on specific financial and non-financial variables; future studies could expand the scope to include broader governance factors or macroeconomic influences.

Ultimately, this research enhances our understanding of how financial and non-financial factors shape audit opinions in a challenging environment. Bridging gaps in the literature and offering actionable insights underscores the importance of robust auditing and governance practices in Greece and other emerging markets seeking to strengthen their financial ecosystems.

Author Contributions

Conceptualization Y.Y, D.V., and I.P.; methodology, D.V.; software, D.V.; validation, Y.Y, D.V., and I.P.; formal analysis, Y.Y, D.V. and I.P.; investigation, Y.Y.; resources, Y.Y.; data curation, D.V.; writing—original draft preparation, Y.Y, D.V. and I.P.; writing—review and editing, Y.Y, D.V. and I.P.; visualization, Y.Y.; supervision, I.P.; project administration, I.P.; funding acquisition, I.P. All authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Institutional Review Board Statement

Not applicable.

Informed Consent Statement

Not applicable.

Data Availability Statement

No new data were created or analyzed in this study. Data sharing is not applicable to this article.

Conflicts of Interest

The authors declare no conflicts of interest.

Appendix A

Table A1.

Previous research on audit opinion characteristics and audit quality. (in alphabetical order of the author).

Table A1.

Previous research on audit opinion characteristics and audit quality. (in alphabetical order of the author).

| Author(s) | Year | Country | Sample | Years | Result - Variables |

| [4] | 2022 | North Macedonia | 99 listed firms | 2014-2017 | Profitability, leverage and report timeliness are related to audit modifications |

| [89] | 2008 | Spain | 533 listed firms | 1992-2002 | Discretionary accruals differ significantly between Going-Concern and non-Going Concern firms |

| [25] | 2010 | U.S. | 12.276 client-years | 2003-2006 | Big-4 and second-tier auditors are equally effective in reducing earnings management |

| [90] | 2004 | U.S. | 4.205 modified audit opinions | 1980-1999 | Modified opinions are related to companies with Going-Concern opinions; such companies have negative abnormal accruals |

| [91] | 2006 | Australia | 1.021 firms in ASX (Australia Stock Exchange) | 1995 | Auditor’s modified opinions tend to reduce over the audit partner’s tenure; this decrease is associated to non-Big 6 firms |

| [92] | 2006 | China (Shenzhen & Shanghai) | 6.531 firm-year observations | 1996-2002 | Local (China-based) audit firms tend to give unqualified audit opinions to government-owned companies |

| [93] | 2013 | US | 12.329 firm-years | 2000-2007 | Abnormal insider sales are negatively associated with the likelihood of receiving a first-time going-concern opinion |

| [94] | 2004 | U.S. | 143.157 client year observations | 1975-1999 | Big-6 clienteles underwent a definite risk improvement in 1990-1994 and a definite to moderate risk deterioration in the prost-1994 (post-reform) period |

| [95] | 2015 | U.S. | 26.428 firm-year observations | 2001-2009 | Examined whether small audit firms (with less than 100 clients) showed higher audit quality compared to Big-4 or mid-tier auditors. The authors used propensity score matching and obtained a propensity score matched sample of 3.048 firm-year observations, of which 1.524 are clients of small audit firms; they found that small audit firms are less stable in order to constrain managers’ opportunistic use of discretionary accruals. |

| [96] | 2015 | Italia | 1.583 firm-year observations | 1998-2011 | Audit quality (proxied by abnormal accruals) improves following audit firm rotation (mandatory and involuntary) only for companies audited by non-Big 4 audit firms. |

| [97] | 2002 | Australia | 1994 (1.062 firms) & 1996 (1.045 firms) | 1994 & 1996 | Audit firms use mechanisms (review partners and peer review) to protect their audit independence |

| [98] | 2014 | Audit Analytics, Compustat & CRSP databases | 30.825 | 2000-2009 | Examining unqualified audit reports, they find that financial statements with unqualified audit reports that include some types of explanatory language are more likely to be subsequently restated than unqualified audit reports without this type of language |

| [99] | 2011 | U.S. | 1.233 small audit firms (with less than 100 clients) | 2001-2008 | After SOX, the number of small audit firms falls by 50%; the small audit firms that exit the market are more likely to receive unfavorable peer review or inspection reports, which implies that these firms are “low quality” suppliers. |

| [100] | 2002 | U.S. | 4.105 firms with audit fee information | 2001 (fiscal year 2000) | There is no evidence that non-audit service fees adversely affect the auditor’s opinion-formulation process, which is consistent with market-based incentives |

| [39] | 1987 | U.S. | 275 first-time subject-to qualifications & 441 unqualified opinions | 1969-1980 | There is an association between auditor’s qualifications for contingencies and firms’ financial and non-financial variables. |

| [101] | 2017 | U.S. | 8.581 financially distressed firms | 2005-2011 | Client fee pressure is negatively associated with auditor propensity to issue a going concern opinion in 2008 (great recession period in 2007-2009). |

| [102] | 2017 | Germany Italy Belgium Finland |

2.879 firm-year observations | 2007-2010 | In the years after an audit switch, auditors increase their fees in order to compensate for the initially low audit fees (fee cutting upon an auditor change). |

| [103] | 2008 | Belgium | 200 client-firm observations in financial distress | 1997 | The size of the audit an audit-firm portfolio has no effect in explaining the variation in financial reporting quality amongst companies; only long-term financial risk of the client portfolio affects reporting quality |

| [104] | 2015 | Spain | 652 firm-year observations of 83 listed firms | 2002-2009 | Long audit firm tenures have negative effect on the independence of external auditors; this shows that litigation risk is an appropriate framework for addressing the auditor reporting decision. |

| [105] | 2006 | U.S. | 1.042 companies with first-time going-concern modified reports & 710 bankrupt companies |

1990-2001 | Big-4 audit firms show higher audit reporting quality; this is inconsistent with the argument that Big-4 audit firms would protect against possible litigations by simply adopting a conservative reporting strategy (i.e., issuing going-concern opinions more often than necessary) |

| [106] | 2003 | U.K. | 9.304 companies, of which 7.125 received a clean report, 431 received going-concern, while 1.748 had non-going-concern modifications | 1998 | Large companies with good liquidity are less likely to receive going-concern modifications, whereas those with high gearing, contingent liabilities, making recent losses and receiving prior year audit modifications, are more likely to receive such modifications. In addition, companies paying high audit fees are also more likely to receive going-concern related modifications. |

| [107] | 2015 | China | 557 listed in Shanghai & Shenzhen stock exchanges | 2001-2011 | High quality audit reduces the restatements’ likelihood; especially in firms with earnings-induced restatements (as opposed to cash flow management-induced restatements. |

| [108] | 2020 | U.S. | 4.539 firm-year observations | 2001-2004 | Controlling the interaction effect of auditor size and industry specialization, analysts are more likely to follow firms audited by Big-5 because their audits are of higher quality. |

| [36] | 1996 | U.S. | 68 audit opinions which disclosed going-concern Uncertainties & 86 Clean Opinions |

1979-1988 | The independent auditor’s going-concern evaluation had a serious effect in the stock market’s reaction; specifically, the results showed negative mean abnormal returns over the three- and five-day periods around the release of the auditor’s going-concern opinion. |

| [109] | 2003 | Compustat | 33.163 firm-year observations | 1994-1998 | Big-6 auditors have incentives to be more conservative in determining reported earnings, because possible litigation costs associated with lawsuits against audit failure are likely to be greater for them. |

| [38] | 1998 | Finland | 111 audit reports from 33 firms listed in Helsinki Stock Exchange (HSE) | 1992-1994 | The qualification of an audit report is mainly associated with low profitability, high indebtedness and negative growth (Univariate model). In addition, they found a negative relation between receiving a qualification and: A) firm’s growth, B) share of equity in the balance sheet and C) number of employees (Multivariate model). |

| [110] | 1999 | U.K. | 1.036 listed firms | 1987-1994 | The author finds evidence that supports the “deep pockets” hypothesis. |

| [111] | 2010 | U.S. | 162.804 firm years | 1981-2001 | Big 5 audit firm consistently provide better audit quality (i.e., they are associated with lower incidences of accounting fraud. |

| [112] | 2015 | Spain | 1.236 audit reports of NOT listed firms (located in the Region of Galicia (in northern Spain) |

2004-2007 | The type of audit opinion and the type of auditor strongly influence the mean number of insignificant and significant errors in the audit report. In addition, irrespective of the type of the audit opinion, individual auditors have a higher propensity to issue audit reports with errors, both insignificant and significant than audit companies or multinationals. |

| [113] | 2017 | Spain | 2.935 audit reports of NOT listed firms | 2007-2009 | During the 2008-2010 financial crisis the proportion of audit reports that include going-concern opinions increased (compared to 2007, a pre-crisis year). |

| [114] | 1995 | U.S. | 103 Firms with Fraudulent Financial Statements (FFS) | 1970-1990 | The sample consisted of 20 listed firms and 83 from over-the-counter (OTC) market matched with similar non-fraud firms. The author finds that financial leverage, capital turnover, asset composition and firm size significantly influence the likelihood of FFS. |

| [75] | 2000 | U.S. | 6.747 | 1996 | The fear of litigation as well as auditor’s reputation override the possible impairment of objectivity due to economic fee dependence inherent in auditor-client contracting. |

| [115] | 2007 | U.S. | 1.332 listed firms that were non-bankrupt but financially distressed | 1997-1999 | Non-Big-6 auditors are more likely to issue going-concern opinions than Big-6, as they have lower materiality thresholds. In addition, non-Big-6 auditors are more likely to find firms that ultimately survive as failing. |

| [78] | 2002 | Greece | 38 manufacturing firms with FFS matched with 38 manufacturing firms with non-FFS | The author used 10 financial ratios in order to find which of these can successfully predict FFS. His model was accurate in detecting FFS more than 80%. | |

| [66] | 2003 | Greece | 50 listed manufacturing firms with audit qualifications and 50 listed manufacturing firms without audit qualifications | 1997-1999 | Firm litigation (dummy variable coded as 1 if company had litigation in the year before the audit opinion and 0 otherwise), financial distress (proxied by Z-Score) and current year losses are variables that can detect, with more than 75% accuracy) FFS (qualified audit reports). |

| [116] | 1998 | U.S. | 51 companies with FFS matched with control companies | 1980-1987 | The authors find differences in insider trading activity variables and important financial statement control variables between the two samples. In addition, fraud companies have significantly more inventory relative to sales, are growing faster and have a higher return on assets than no-fraud companies in the year before the occurrence of the fraud. |

| [117] | 1998 | Finland | Random sample of 304 non-bankrupt firms & 118 bankrupt | 1991-1995 | The data showed that modified audit reports are more common in unprofitable, leveraged and failing firms, but there are no significant differences in the propensity to modify the report between auditors with the higher and lower professional qualification. |

| [118] | 2014 | Sweden | 93 Small companies receiving first-time going-concern audit opinion & control sample of companies in financial distress that had not received going-concern audit opinion | 2009 | The authors find evidence that the issuance of first-time going-concern opinions is positively related to auditor switching; in addition, there exist higher failure rates among companies receiving first-time going-concern than among equally financially stressed companies that do not receive going-concern opinions. Lastly, regarding auditors, the authors suggest that auditors issuing first-time going-concern opinions lose proportionally more fees (due to both auditor switching and client bankruptcy) than do auditors who do not issue going-concern audit opinions. |

| [6] | 2008 | U.S. | 8-K reports filed by Fortune 500 companies (using the list of 2001) | 2001-2002 | Material misstatements due to error lowered rather than raised income; in addition, companies reporting misstatements that materially reduced income were more likely to change auditors. |

| [119] | 2016 | U.K. | 116 Failed firms listed in London Stock Exchange (LSE) | 1997-2010 | Investigated the relationship between audit committee independence, auditor-provided non-audit services (NAS) fees and the likelihood of going concern modifications prior to a corporate failure event. They found that that failed firms with higher proportions of independent non-executive directors (NEDs) and financial experts on the audit committee are more likely to receive auditor going-concern modifications prior to failure. |

| [120] | 2011 | Australia | 8.382 listed companies in the total sample period | 2005-2009 | Examined the frequency of going-concern audit reports before and after the Global Financial Crisis (GFC); modification rates in audit reports increased from 12% in 2005-2007 to 18% in 2008 and to 22% in 2009. |

References

- Adiloglu, B.; Vuran, B. Identification of key performance indicators of auditor’s reports: Evidence from Borsa Istanbul (BIST). J. Econ. Financ. Account. 2017, 4, 256–261. [Google Scholar] [CrossRef]

- Anderson, R.C.; Mansi, S.A.; Reeb, D.M. Board characteristics, accounting integrity and the cost of debt. J. Account. Econ. 2004, 37, 315–342. [Google Scholar] [CrossRef]

- Durendez, A.G.-G. The usefulness of the audit report in investment and financing decisions. Manag. Audit. J. 2003, 18, 549–559. [Google Scholar] [CrossRef]

- Srbinoska, S. Audit modifications in emerging markets: The Macedonian Stock Exchange. Rom. J. Econ. Inst. Natl. Econ. 2022, 55, 43–69. [Google Scholar]

- Dechow, P.; Ge, W.; Schrand, C. Understanding earnings quality: A review of the proxies, their determinants and their consequences. J. Account. Econ. 2010, 50, 344–401. [Google Scholar] [CrossRef]

- Thompson, J.H.; McCoy, T.L. An analysis of restatements due to errors and auditor changes by Fortune 500 companies. J. Leg. Ethical Regul. Issues 2008, 11, 45–57. [Google Scholar]

- Carson, E.; Fargher, N.; Zhang, Y. Explaining auditors’ propensity to issue going-concern opinions in Australia after the global financial crisis. Account. Financ. 2019, 59, 2415–2453. [Google Scholar] [CrossRef]

- Newman, D.P.; Patterson, E.R.; Smith, J.R. The role of auditing in investor protection. Account. Rev. 2005, 80, 289–313. [Google Scholar] [CrossRef]

- Camfferman, K.; Wielhower, J.L. 21st century scandals: Towards a risk approach to financial reporting scandals. Account. Bus. Res. 2019, 49, 503–535. [Google Scholar] [CrossRef]

- International Auditing and Assurance Standards Board (IAASB). (2015). 2015 Handbook of international quality control, auditing, review, other assurance, and related services pronouncements. Available online: https://www.iaasb.org/publications/2015-handbook-international-quality-control-auditing-review-other-assurance-and-related-services-0 (accessed on 22 October 2024).

- Zarei, H.; Yazdifar, H.; Ghaleno, M.D.; Azmaneh, R. Predicting auditors’ opinions using financial ratios and non-financial metrics: Evidence from Iran. J. Account. Emerg. Econ. 2020, 10, 425–446. [Google Scholar] [CrossRef]

- Marques, V.A.; Pereira, L.N.; de Aquino, I.F.; Freitag, V.d.C. Has it become more readable? Empirical evidence of key audit matters in independent audit reports. Rev. Contab. Finanças 2021, 32, 444–460. [Google Scholar] [CrossRef]

- Makrominas, M.; Yiannoulis, Y.K. IPO determinants of delisting risk: Lessons from the Athens Stock Exchange. Account. Forum 2021, 45, 307–331. [Google Scholar] [CrossRef]

- Ballas, A.A.; Chalevas, C.; Tzovas, C. Market reaction to valuation adjustments for financial instruments: Evidence from Greece. J. Int. Account. Audit. Tax. 2012, 21, 52–61. [Google Scholar] [CrossRef]

- Neratzidis, M.; Tsamis, A. Going back to go forward: On studying the determinants of corporate governance disclosure. Corp. Gov. Int. J. Bus. Soc. 2017, 17, 365–402. [Google Scholar] [CrossRef]

- Dimitropoulos, P.E.; Asteriou, D. The effect of board composition on the informativeness and quality of earnings: Empirical evidence from Greece. Res. Int. Bus. Financ. 2010, 24, 190–205. [Google Scholar] [CrossRef]

- Tzovas, C. Factors influencing a firm’s accounting policy when tax accounting and financial accounting coincide. Manag. Audit. J. 2006, 21, 372–386. [Google Scholar] [CrossRef]

- Baralexis, S. Creative accounting in small advancing countries: The Greek case. Manag. Audit. J. 2004, 19, 440–461. [Google Scholar] [CrossRef]

- Dimitropoulos, P.E.; Asteriou, D. The value relevance of financial statements and their impact on stock prices: Evidence from Greece. Manag. Audit. J. 2009, 24, 514–530. [Google Scholar] [CrossRef]

- Yaşar, A.; Yakut, E.; Gutnu, M.M. Predicting qualified audit opinions using financial ratios: Evidence from the Istanbul Stock Exchange. Int. J. Bus. Soc. Sci. 2015, 6, 57–67. [Google Scholar]

- Hölmstrom, B. Moral hazard and observability. Bell J. Econ. 1979, 10, 74–91. [Google Scholar] [CrossRef]

- Robu, M.A.; Robu, I.B. The influence of the audit report on the relevance of accounting information reported by listed Romanian companies. Procedia Econ. Financ. 2015, 20, 562–570. [Google Scholar] [CrossRef]

- Lee, H.-L.; Lee, H. Do big 4 audit firms improve the value relevance of earnings and equity? Manag. Audit. J. 2013, 28, 628–646. [Google Scholar] [CrossRef]

- Ittonen, K. Market reactions to qualified audit reports: Research approaches. Account. Res. J. 2012, 25, 8–24. [Google Scholar] [CrossRef]

- Boone, J.P.; Khurana, I.K.; Raman, K.K. Do the Big 54 and the second-tier firms provide audits of similar quality? J. Account. Public Policy 2010, 29, 330–352. [Google Scholar] [CrossRef]

- Gómez-Guillmón, A.D. The usefulness of the audit report in investment and financing decisions. Manag. Audit. J. 2008, 18, 549–559. [Google Scholar] [CrossRef]

- Martinez MC, P.; Martinez, A.V.; Benau MA, G. Reactions of the Spanish capital market to qualified audit reports. Eur. Account. Rev. 2004, 13, 689–711. [Google Scholar] [CrossRef]

- Jensen, M.C.; Meckling, W. Theory of the firm: Managerial behavior, agency cost and ownership structure. J. Financ. Econ. 1976, 3, 305–360. [Google Scholar] [CrossRef]

- Seifzadeh, M.; Salehi, M.; Abedini, B.; Ranjbar, M.H. The relationship between management characteristics and financial statement readability. EuroMed J. Bus. 2020, 16, 108–126. [Google Scholar] [CrossRef]

- Bloomfield, J. Discussion of annual report readability, current earnings and earnings persistence. J. Account. Econ. 2008, 45, 248–252. [Google Scholar] [CrossRef]

- Altman, E.I. Financial ratios, discriminant analysis and the prediction of corporate bankruptcy. J. Financ. 1968, 23, 589–609. [Google Scholar] [CrossRef]

- Cornett, M.M.; Adair, T.A.; John, N. (2008). Finance: Applications and Theory, 1st edition, McGraw Hill.

- Kanapickienè, R.; Grunienè, Z. The model of fraud detection in financial statements by means of financial ratios. Procedia-Soc. Behav. Sci. 2015, 213, 321–327. [Google Scholar] [CrossRef]

- Mutchler, J.F. A multivariate analysis of the auditor’s going-concern opinion decision. Journal of Accounting Research 1985, 23, 668–682. [Google Scholar] [CrossRef]

- Hopwood, W.; McKeow, J.; Mutchler, J. A test of the incremental explanatory power of opinions qualified for consistency and uncertainty. Account. Rev. 1989, 64, 28–47. [Google Scholar]

- Jones, F.L. The information content of the auditor’s going concern evaluation. J. Account. Public Policy 1996, 1, 1–27. [Google Scholar] [CrossRef]

- Keasey, K.; Watson, R.; Wynarzcyk, P. The small company audit qualifications: A preliminary investigation. Account. Bus. Res. 1988, 18, 323–333. [Google Scholar] [CrossRef]

- Laitinen, E.K.; Laitinen, T. Qualified audit reports in Finland: Evidence from large companies. Eur. Account. Rev. 1998, 7, 639–653. [Google Scholar] [CrossRef]

- Dopuch, N.; Holthausen, R.; Leftwich, R. Predicting audit qualifications with financial and market variables. Account. Rev. 1987, 62, 431–454. [Google Scholar]

- Citron, D.B.; Taffler, R.J. The audit report under going concern uncertainties: An empirical analysis. Account. Bus. Res. 1992, 22, 337–345. [Google Scholar] [CrossRef]

- Chan, Y.K.; Walter, T.S. Qualified audit reports and costly contracting. Asia Pac. J. Manag. 1996, 13, 37–63. [Google Scholar] [CrossRef]

- Dimitras, A.I.; Zanakis, S.H.; Zopounidis, C. A survey of business failures with an emphasis on prediction models and industrial applications. Eur. J. Oper. Res. 1996, 90, 487–513. [Google Scholar] [CrossRef]

- Anandarajan, M.; Anandarajan, A. A comparison of machine learning techniques with a qualitative response model for auditor’s going concern reporting. Expert Syst. Appl. 1999, 16, 385–392. [Google Scholar] [CrossRef]

- Doumpos, M.; Zopounidis, C. Business failure prediction: A comparison of classification methods. Oper. Res. Int. J. 2002, 2, 303–319. [Google Scholar] [CrossRef]

- Gaganis, C.; Pasiouras, F.; Tzanetoulakos, A. A comparison and integration of techniques for the prediction of small UK firms’ failure. J. Financ. Decis. Mak. 2005, 1, 55–69. [Google Scholar]

- Doumpos, M.; Gaganis, C.; Pasiouras, F. Explaining qualifications in audit reports using a SVM methodology. Intell. Syst. Account. Financ. Manag. 2005, 13, 197–215. [Google Scholar] [CrossRef]

- Pasiouras, F.; Gaganis, C.; Zopounidis, C. Multicriteria decision support methodologies for auditing decisions: The case of qualified audit reports in the UK. Eur. J. Oper. Res. 2007, 180, 1317–1330. [Google Scholar] [CrossRef]

- Kirkos, E.; Spathis, C.; Nanopoulos, A.; Manolopoulos, Y. Identifying qualified auditors opinions: A data mining approach. J. Emerg. Technol. Account. 2007, 4, 183–197. [Google Scholar] [CrossRef]

- Gaganis, C.; Pasiouras, F.; Doumpos, M. Probabilistic neural networks for the identification of qualified audit reports. Expert Syst. Appl. 2007, 32, 114–124. [Google Scholar] [CrossRef]

- Gaganis, C.; Pasiouras, F.; Spathis, C.; Zopounidis, C. A comparison of nearest neighbours, discriminant and logit models for auditing decisions. Intell. Syst. Account. Financ. Manag. 2007, 15, 23–40. [Google Scholar] [CrossRef]

- Maggina, A.; Tsaklaganos, A.A. Predicting audit opinions: Evidence from the Athens Stock Exchange. J. Appl. Bus. Res. 2011, 27, 53–68. [Google Scholar] [CrossRef]

- Saif, S.M.; Sarikhani, M.; Ebrahimi, F. Finding rules for audit opinions predictions through data mining methods. Eur. Online J. Nat. Soc. Sci. 2012, 1, 28–36. [Google Scholar] [CrossRef]

- Nahandi, Y.B.; Sarokolaei, M.A.; Ghasemi, S. Evaluating the ability of cash flow ratios in predicting auditor’s opinion. Int. J. Adv. Stud. Humanit. Soc. Sci. 2013, 1, 328–343. [Google Scholar]

- Averio, T. The analysis of influencing factors on the going concern audit opinion—A study in manufacturing firms in Indonesia. Asian J. Account. Res. 2021, 6, 152–164. [Google Scholar] [CrossRef]

- Ballas, A. Accounting in Greece. Eur. Account. Rev. 1994, 3, 107–121. [Google Scholar] [CrossRef]

- Ballas, A.; Hevas, D.; Neal, D. The state of the Accounting and the state of the State. J. Manag. Gov. 1998, 2, 267–285. [Google Scholar] [CrossRef]

- LaPorta, R.; Lopez-de-Silanes, F.; Shleifer, A. Corporate ownership around the world. J. Financ. 1999, 54, 471–517. [Google Scholar] [CrossRef]

- Baboukardos, D.; Rimmel, G. Goodwill under IFRS: Relevance and disclosures in an unfavorable environment. Account. Forum 2014, 38, 1–17. [Google Scholar] [CrossRef]

- Lazarides, T. Duality of roles and corporate governance in Greece. Corp. Board Role Duties Compos. 2009, 5, 15–21. [Google Scholar] [CrossRef]

- Tsalavoutas, I. (2009). Adoption of IFRS by Greek listed companies: Financial statement effects, level of compliance and value relevance. Thesis, University of Edinburgh. Available online: https://era.ed.ac.uk/bitstream/handle/1842/4060/Tsalavoutas2009.pdf?sequence=1&isAllowed=y (accessed on 22 October 2024).

- Nobes, C. Accounting classification in the IFRS era. Aust. Account. Rev. 2008, 18, 191–198. [Google Scholar] [CrossRef]

- Tsipouri, L.; Xanthakis, M. Can corporate governance be rated? Ideas based on the Greek experience. Corp. Gov. Int. Rev. 2004, 12, 16–28. [Google Scholar] [CrossRef]

- Leuz, C.; Nanda, D.; Wysocki, P.D. Earnings management and investor protection: An international comparison. J. Financ. Econ. 2003, 69, 505–527. [Google Scholar] [CrossRef]

- Bhattacharya, U.; Daouk, K.; Welker, M. The world price of opacity. Account. Rev. 2003, 78, 641–678. [Google Scholar] [CrossRef]

- Spathis, C. Audit qualification, firm litigation and financial information: An empirical analysis in Greece. Int. J. Audit. 2003, 7, 71–85. [Google Scholar] [CrossRef]

- Spathis, C.; Doumpos, M.; Zopounidis, C. Using client performance measures to identify pre-engagement factors associated with qualified audit reports in Greece. Int. J. Account. 2003, 38, 267–284. [Google Scholar] [CrossRef]

- Caramanis, C.; Spathis, C. Auditee and audit firm characteristics as determinants of audit qualifications: Evidence from the Athens stock exchange. Manag. Audit. J. 2006, 21, 905–920. [Google Scholar] [CrossRef]

- Tsipouridou, M.; Spathis, C. Earnings management and the role of auditors in an unusual IFRS context: The case of Greece. J. Int. Account. Audit. Tax. 2012, 21, 62–78. [Google Scholar] [CrossRef]

- Junaidi Hartono, J. Non-financial factors in the going-concern opinion. J. Indones. Econ. Bus. 2010, 25, 369–378. [Google Scholar]

- Ballesta JP, S.; Garcia, E. Audit qualifications and corporate governance in Spanish listed firms. Manag. Audit. J. 2005, 20, 725–738. [Google Scholar] [CrossRef]

- DeAngelo, L.E. Auditor size and audit quality. J. Account. Econ. 1981, 3, 183–199. [Google Scholar] [CrossRef]

- Khaddafi, M. Effect of debt default, audit quality and acceptance of audit opinion going concern in manufacturing company in Indonesia stock exchange. Int. J. Acad. Res. Account. Financ. Manag. Sci. 2015, 5, 801–891. [Google Scholar] [CrossRef]

- Mukhtaruddin, P.; Handri, P.; Meutia, I. Financial condition, growth, audit quality and going concern opinion: A study on manufacturing companies listed on Indonesia Stock Exchange. J. Account. Bus. Financ. Res. 2018, 2, 16–25. [Google Scholar]

- Loebbecke, J.K.; Eining, M.M.; Willingham, J.J. Auditors’ experience with material irregularities: Frequency, nature and detectability. Audit. A J. Pract. Theory 1989, 9, 1–28. [Google Scholar]

- Reynolds, J.K.; Jere, R. Does size matter? The influence of large clients on office-level auditor reporting decisions. J. Account. Econ. 2001, 30, 375–400. [Google Scholar] [CrossRef]

- Simamora, R.A. ; Hendarjatno, The effects of audit client tenure, audit lag, opinion shopping, liquidity ratio and leverage to the going concern audit opinion. Asian J. Account. Res. 2019, 4, 145–156. [Google Scholar] [CrossRef]

- Fanning, K.M.; Cogger, K.O. Neural network detection of management fraud using published financial data. Intell. Syst. Account. Financ. Manag. 1998, 7, 21–41. [Google Scholar] [CrossRef]

- Spathis, C.; Doumpos, M.; Zopounidis, C. Detecting falsified financial statements: A comparative study using multicriteria analysis and multivariate statistical techniques. Eur. Account. Rev. 2002, 11, 509–535. [Google Scholar] [CrossRef]

- Gaganis, C. Classification techniques for the identification of falsified financial statements: A comparative analysis. Intell. Syst. Account. Financ. Manag. 2009, 16, 207–229. [Google Scholar] [CrossRef]

- Ravisankar, P.; Ravi, V.; Raghava, R.G.; Bose, I. Detection of financial statement fraud and feature selection using data mining techniques. Decis. Support Syst. 2011, 50, 491–500. [Google Scholar] [CrossRef]

- Dalnial, H.; Kamaluddin, A.; Sanusi, Z.M.; Khairuddin, K.S. Accountability in financial reporting: Detecting fraudulent firms. Procedia-Soc. Behav. Sci. 2014, 145, 61–69. [Google Scholar] [CrossRef]

- Beaver, W.H. Financial ratios as predictors of failure. J. Account. Res. 1996, 71–111. [Google Scholar] [CrossRef]

- Carson, E.; Fargher, N.L.; Geiger, M.A.; Lennox, C.S.; Raghunandan, K.; Willekens, M. Audit reporting for going-concern uncertainty: A research synthesis. Audit. A J. Pract. Theory 2012, 32, 353–384. [Google Scholar] [CrossRef]

- Ghale Rudkhani, T.M.; Jabbari, H. The effect of financial ratios on auditor opinion in the companies listed on TSE. Eur. Online J. Nat. Soc. Sci. Proc. 2014, 2, 1363–1373. [Google Scholar]

- Moalla, H. Audit report qualification/modification: Impact of financial variables in Tunisia. J. Account. Emerg. Econ. 2017, 7, 468–485. [Google Scholar] [CrossRef]

- Moalla, H.; Baili, R. Credit ratings and audit opinion: Evidence from Tunisia. J. Account. Emerg. Econ. 2019, 9, 103–125. [Google Scholar] [CrossRef]

- Maldonado, I.; Pinho, C.; Lobo, C.A. (2019). Determinant factors of external audit opinion modification in Portuguese municipalities”, in 2019 14th Iberian Conference on Information Systems and Technologies, 1-6. Available online: https://repositorio.uportu.pt/jspui/bitstream/11328/2794/4/Determinant%20factors%20of%20external%20audit%20opinion.pdf (accessed on 22 October 2024).

- Özcan, A. Determining factors affecting audit opinion: Evidence from Turkey. Int. J. Account. Financ. Report. 2016, 6, 45–62. [Google Scholar] [CrossRef]

- Arnedo, L.; Lizarraga, F.; Sánchez, S. Going-concern uncertainties in pre-bankrupt audit reports: New evidence regarding discretionary accruals and wording ambiguity. Int. J. Audit. 2008, 12, 25–44. [Google Scholar] [CrossRef]

- Butler, M.; Leone, A.J.; Willenborg, M. An empirical analysis of auditor reporting and its association with abnormal accruals. J. Account. Econ. 2004, 37, 139–165. [Google Scholar] [CrossRef]

- Carey, P.; Simnett, R. Audit partner tenure and audit quality. Account. Rev. 2006, 81, 653–676. [Google Scholar] [CrossRef]

- Chan, K.H.; Lin, K.Z.; Mo PI, I. A political-economic analysis of auditor reporting and auditor switches. Rev. Account. Stud. 2006, 11, 21–48. [Google Scholar] [CrossRef]

- Chen, C.; Martin, X.; Wang, X. Insider trading, litigation concerns and auditor going-concern opinions. Account. Rev. 2013, 88, 365–393. [Google Scholar] [CrossRef]

- Choi, J.H.; Doogar, R.; Ganguly, A.R. The riskness of large audit firm client portfolios and changes in audit reliability regimes: Evidence from the U.S. audit market. Contemp. Account. Res. 2004, 21, 747–785. [Google Scholar] [CrossRef]

- Comprix, J.; Huang, H. Does auditor size matter? Evidence from small audit firms. Adv. Account. Inc. Adv. Int. Account. 2015, 31, 11–20. [Google Scholar] [CrossRef]

- Corbella, S.; Florio, C.; Gotti, G.; Mastrolia, S.A. Audit firm rotation, audit fees and audit quality: The experience of Italian public companies. J. Int. Account. Audit. Tax. 2015, 25, 46–66. [Google Scholar] [CrossRef]

- Craswell, A.; Stokes, D.J.; Laughton, J. Auditor independence and fee dependence. J. Account. Econ. 2002, 33, 253–275. [Google Scholar] [CrossRef]

- Czerney, K.; Schmidt, J.J.; Thompson, A.M. Does auditor explanatory language in unqualified audit opinions indicate increased financial misstatement risk? Account. Rev. 2014, 89, 2115–2149. [Google Scholar] [CrossRef]

- DeFond, M.L.; Lennox, C. The effect of SOX on small auditor exits and audit quality. J. Account. Econ. 2011, 52, 21–40. [Google Scholar] [CrossRef]

- DeFond, M.L.; Raghunandan, K.; Subramanyam, K.R. Do non-audit service fees impair auditor independence? Evidence from going concern opinions. J. Account. Res. 2002, 40, 1247–1274. [Google Scholar] [CrossRef]

- Ettredge, M.; Fuerherm, E.; Guo, F.; Li, C. Client pressure and auditor independence: Evidence from the “Great Recession” of 2007-2009. J. Account. Public Policy 2017, 36, 262–283. [Google Scholar] [CrossRef]

- Fleischer, R.; Goettsche, M.; Schauer, M. The Big 4 premium: Does it survive an auditor change? Evidence from Europe. J. Int. Account. Tax. 2017, 29, 103–117. [Google Scholar] [CrossRef]

- Gaeremynck, A.; Van der Meulen, S.; Willekens, M. Audit-firm portfolio characteristics and client financial reporting quality. Eur. Account. Rev. 2008, 1, 1–28. [Google Scholar] [CrossRef]

- Garcia-Blandon, J.; Argiles, J.M. Audit firm tenure and independence: A comprehensive investigation of audit qualifications in Spain. J. Int. Account. Audit. Tax. 2015, 24, 82–93. [Google Scholar] [CrossRef]

- Geiger, M.A.; Rama, D.V. Audit firm size and going-concern reporting accuracy. Account. Horiz. 2006, 20, 1–17. [Google Scholar] [CrossRef]

- Ireland, J. An empirical investigation of determinants of audit reports in the UK. J. Bus. Financ. Account. 2003, 30, 975–1015. [Google Scholar] [CrossRef]

- Jiang, H.; Habib, A.; Zhou, D. Accounting restatements and audit quality in China. Adv. Account. Inc. Adv. Int. Account. 2015, 31, 125–135. [Google Scholar] [CrossRef]

- Jeong, K. The effect of audit quality on analyst following. Cogent Bus. Manag. 2020, 7, 1–11. [Google Scholar] [CrossRef]

- Kim, J.B.; Chung, R.; Firth, M. Auditor conservatism, asymmetric monitoring and earnings management. Contemp. Account. Res. 2003, 20, 323–359. [Google Scholar] [CrossRef]

- Lennox, C. Audit quality and auditor size: An evaluation of reputation and deep pockets hypothesis. J. Bus. Financ. Account. 1999, 26, 779–805. [Google Scholar] [CrossRef]

- Lennox, C.; Pitman, J. Big Five audits and accounting fraud. Contemp. Account. Res. 2010, 27, 209–247. [Google Scholar] [CrossRef]

- Mareque, M.; López-Corrales, F.J.; Fiestras, G. Do auditors make mistakes when they write audit reports? An empirical study applied to Spanish non-listed firms. Econ. Res. -Ekon. Istraživanja 2015, 30, 154–183. [Google Scholar] [CrossRef]

- Mareque, M.; López-Corrales, F.J.; Pedrosa, A. Audit reporting for going concern in Spain during the global financial crisis. Econ. Res. -Ekon. Istraživanja 2017, 30, 154–183. [Google Scholar] [CrossRef]

- Persons, O.S. Using financial statement data to identify factors associated with fraudulent financial reporting. J. Appl. Bus. Res. 1995, 11, 38–46. [Google Scholar] [CrossRef]

- Ryu, T.G.; Roh, C.-Y. The auditor’s going-concern opinion decision. Int. J. Bus. Econ. 2007, 6, 89–101. [Google Scholar]

- Summers, S.L.; Sweeney, J.T. Fraudulently misstated financial statements and insider trading: An empirical analysis. Account. Rev. 1998, 73, 131–146. [Google Scholar]

- Sundgren, S. Auditor choices and reporting practices: Evidence from Finnish small firms. Eur. Account. Rev. 1998, 7, 441–465. [Google Scholar] [CrossRef]

- Svanberg, J.; Öhman, P. Lost revenues associated with going-concern modified opinions in the Swedish audit market. J. Appl. Account. Res. 2014, 15, 197–214. [Google Scholar] [CrossRef]

- Wu, C.Y.; Hsu, H.; Haslam, J. Audit committees, non-audit services and auditor reporting decisions prior to failure. Br. Account. Rev. 2016, 48, 240–256. [Google Scholar] [CrossRef]

- Xu, Y.; Jiang, A.; Fargher, N.; Carson, E. Audit reports in Australia during the Global Financial Crisis. Aust. Account. Rev. 2011, 21, 22–31. [Google Scholar] [CrossRef]

Table 2.

Descriptive statistics

| Dependent | Independent variables | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| AQ | A | B | C | D | E | F | |||||

| Mean | 0 | 2.56 | 0.3632 | 0.5666 | 1 | 0.0833 | 1 | ||||

| Median | 0 | 2.63 | 0.3577 | 0.5766 | 1 | 0 | 1 | ||||

| Maximum | 0 | 3.26 | 0.4800 | 0.6643 | 1 | 0.5000 | 1 | ||||

| Minimum | 0 | 1.88 | 0.2676 | 0.4283 | 1 | 0 | 1 | ||||

| Std. Dev. | 0 | 0.5221 | 0.0807 | 0.0886 | 0 | 0.2041 | 0 | ||||

| Skewness | - | -0.0451 | 0.4886 | -0.5046 | - | 1.79 | - | ||||

| Kurtosis | - | 1.77 | 2.26 | 2.83 | - | 4.20 | - | ||||

| Jarque-Bera | - | 0.4095 | 0.9308 | 1.51 | - | 3.56 | - | ||||

| Probability | - | 0.8153 | 0.6303 | 0.5253 | - | 0.1686 | - | ||||

| Control variables | |||||||||||

| G | H | I | J | K | L | M | N | O | Βen | Altm | |

| Mean | 2.56 | 118.81 | 1,058 | 0.6470 | 0.1063 | 0.1403 | 0.1732 | 0.1456 | 0.5000 | -2.98 | 2.02 |

| Median | 2.63 | 108.50 | 26.29 | 0.6600 | 0.0854 | 0.1302 | 0.1342 | 0.1437 | 0.5000 | -2.75 | 2.05 |

| Maximum | 3.25 | 147.77 | 6,369 | 0.7498 | 0.1988 | 0.2340 | 0.3338 | 0.2164 | 1 | -2.31 | 2.36 |

| Minimum | 1.88 | 100.17 | -120.34 | 0.5104 | 0.0568 | 0.0751 | 0.0780 | 0.0759 | 0 | -4.51 | 1.62 |

| Std. Dev. | 0.5216 | 25.62 | 2,609 | 0.0997 | 0.0532 | 0.0576 | 0.1046 | 0.0576 | 0.5477 | 0.8450 | 0.2588 |

| Skewness | -0.0506 | 0.0396 | 0.8466 | -0.3198 | 0.8760 | 0.3107 | 0.4970 | -0.0156 | 0 | -0.8501 | -0.1887 |

| Kurtosis | 1.78 | 1.50 | 2.66 | 1.51 | 2.54 | 2.65 | 1.79 | 1.43 | 1 | 2.67 | 2.39 |

| Jarque-Bera | 0.4056 | 0.4651 | 2.22 | 0.7376 | 0.8455 | 0.7059 | 0.7028 | 0.6334 | 1 | 1.69 | 0.3266 |

| Probability | 0.8169 | 0.7926 | 0.4059 | 0.6916 | 0.6618 | 0.7209 | 0.7071 | 0.7286 | 0.6065 | 0.4951 | 0.8561 |

Table 3.

Granger causality tests between the dependent and each independent or control variable

| A | B | C | D | E | F | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| H1 | F-statistic | 5.18 | 333.87 | 1.59 | - | 0.25 | - | ||||