Submitted:

01 January 2025

Posted:

02 January 2025

You are already at the latest version

Abstract

This study aims to derive internal and external characteristics of non-performing real estate Project Financing workplaces and examine the effects of specific factors on their successful bidding. In addition, significant variables are selected based on the analysis result, and an AHP analysis is performed to establish a new valuation system for real estate development projects. After careful consideration of various literature reviews and expert opinions, the analysis model is established to secure the suitability of the study model with the error range minimized. As AHP was performed based on the newly established hierarchy, the higher ranks of each valuation factor were derived based on priority and importance, and the valuation basis was rearranged accordingly. The conclusion was derived through a comprehensive review of the results of the two analyses above. It was verified that certain factors—business feasibility assessment, work performance assessment, basal evaluation—played key roles in the success and successful bidding of real estate projects. This point suggests that strict project management and performance standards must be set based on the economic achievements of financial validity indexes and business performance capabilities. Stable profit distribution and business transparency are also viewed as vital factors for the success of projects. Therefore, this study reestablishes the valuation basis for development projects and presents policy suggestions on location propriety and business advancement based on the analysis of non-performing PF bid decision factors and the development project valuation basis.

Keywords:

development project

; project financing

; bid decision factor

; regression analysis

; AHP

; valuation basis

1. Introduction

1.1. Study Background and Objective

Recently, the scale of loans for real estate PF among large construction companies has been increasing continually, and construction projects have been suspended frequently. The PF default rate in the existing financial sector is gradually growing as well. Notably, the ratio of non-performing loans for PF in the financial sector of Korea has almost tripled compared to that in 2023, which means that the increase rate is as high as 11.2%. The rate increased rapidly by as much as 6.1% within half a year [1]. It is then unlikely that this increase in the ratio of non-performing loans will lead directly to system risks in the financial sector. Still, some analytics suggest that the rate has rapidly increased as financial authorities intensified pressure on normalizing non-performing workplaces this year [2]. The default rate of PF loans is increasing because the regulation on risks has become stricter for workplaces involving the suspension of projects, insufficient supply of new funds, estimated loss of 100% for non-performing bridge loans in the financial sector, and delayed arrangement of non-performing PF workplaces [3]. To address such problems, therefore, it is necessary to normalize development sites where the construction was discontinued. In other words, non-performing real estate PF development sites need to be re-operated by winning the bids, and it is necessary to thoroughly analyze factors that affect such successful bidding on non-performing real estate PF development sites. For this purpose, the Korean government entrusted Korea Asset Management Corporation (hereafter, referred to as KAMCO) with the non-performing PF auction amounting to 13.5 trillion won and the real estate PF normalization plan during the second half of the year with the intention of managing non-performing development sites. Against this background, verifying the factors that affect successful bidding in auctions of non-performing real estate PF and how development project valuation and deliberation need to be conducted [4] is necessary. With such a tremendous amount of investment, the government has displayed a strong will to restructure non-performing workplaces and has paid keen attention to this issue. To fulfill this policy successfully, analyzing and specifying deciding factors related to the bidding of non-performing real estate PF led by the government is vital. For standards for development project valuation before construction initiation, factors that affect the successful bidding of non-performing PF workplaces need to be considered. Even for standards applicable before implementation of such development projects when delayed funding due to a construction suspension or delay does not occur yet, careful item adjustment will be necessary for the success of projects. Most of all, the vagueness and subjectivity of the valuation basis for development projects are the most significant issues to be handled [5].

For similar problems, many policies and research projects have been initiated in Korea regarding the deciding factors of bidding and valuation system enhancement for non-performing real estate PF. The valuation basis has recently become a more serious social issue due to bankruptcy and work-out among enterprises resulting from increasing construction costs and labor fees. In 2016, KAMCO purchased non-performing loans to normalize non-performing PF workplaces and attempted bidding on 32 among 484 non-performing buildings [6]. As a result, 15 places were auctioned, and 17 places failed in bidding. This result suggests normalization was not performed as planned for regulating non-performing workplaces. Furthermore, bidding factors were not exactly understood as procedures were initiated. This is mainly because of the sudden market contraction and complex interests among the entities concerned. On the other hand, KAMCO could not partially take the lead of normalization for additional reasons, such as lack of related regulations and grounds, passive implementation of public enterprises, etc. Active institutional supplementation will be necessary to normalize many non-performing PF workplaces remaining in the future [7]. In addition, there are various and complex development projects; thus, reviewing such projects is complicated. However, there is only one unified standard for evaluation, which is not enough to consider such various characteristics [8]. This advantage is pointed out as a significant factor resulting in construction delays and increased default rates. Therefore, it is necessary to examine bid decision factors for non-performing real estate PF and factors that affect bidding. It is essential to apply weights to the valuation basis for real estate PF, as suggested by many research projects based on analysis results, to make up for weak points on the current valuation basis. This is one suggestion to address inadequate aspects of the existing valuation basis, which have been pointed out, and to revitalize the real estate PF market. For development projects, weights must be applied to investment examination to derive verified results [9].

Therefore, this study analyzes factors that affected successful bidding among 32 out of 484 non-performing real estate PF development sites that KAMCO acquired in the year of 2016. To address simplified restrictions to non-performing PF variables pointed out by previous studies on real estate PF as a limitation, the spatial scope was established based on quantitative analysis, followed by qualitative analysis of bid decision factors to derive various implications. Variables with significant results of the suggested analysis are utilized in additional analysis to restructure the valuation system before each real estate development project. Further analysis provides significant variables as central elements in using the analytical hierarchy process (AHP) to establish a new valuation system for real estate development PF.

1.2. Scope and Method

This study utilized the two following analytic methods: First, this study analyzed factors affecting the successful bidding among 32 out of 484 non-performing PF development sites that KAMCO acquired. With the bidding result as a dummy variable, regression analysis compared the decision factors of failed bids (y=0) and successful bids (y=1). With the spatial scope added, the methodology for internal and external factors was selected. In this context, the ’spatial scope’ means the range that covers the geographical boundary in which real estate properties are located (physical scope), the economic sphere in the real estate market (economic scope), and the boundary of the local living area and community (socio-cultural scope).

Regression analysis is a statistical method to analyze the causality between an object variable and an explanatory variable, with results categorized into two. This method is utilized mainly to understand the trend based on collected data or factors that affect the result. It is quite useful in establishing strategies by inferring the relation among variables and predicting the result in the future. However, this method is disadvantageous in that the analysis result may be distorted as an important variable is omitted or an unnecessary variable is included in the analysis. Besides, the reliability of the regression coefficient decreases when the correlation between independent variables is high, which is another disadvantage. As part of this study, therefore, correlation analysis was also performed to minimize interferences with the effects of multicollinearity in the analytic model. As for regression analysis, many studies did not include multicollinearity. The analytic methodology of this study also excluded it since it was expected that the VIF value would be affected when the Pearson correlation coefficient was 0.8 or higher because the estimated coefficient’s reliability would decrease if explanatory variables were highly correlated. As for independent variables affecting the bidding result, various previous studies, literature, and policy and economic aspects were widely considered. Second, the analytic hierarchy process (AHP) was utilized to establish a new valuation system specifying evaluation areas of real estate development projects and applying weights to them. After investigating previous studies and considering policy and economic aspects, the hierarchy was schematized and the model was set on this basis. Also, each valuation standard’s weights were selected based on the established hierarchy. Under the major classification of real estate development project valuation, factors of the first and second ranks were divided into 5 groups: basic evaluation of land lots, business feasibility assessment, work performance assessment, investor protection plan, etc. Fourteen valuation models were then established: physical suitability, legal suitability, administrative suitability, adjacent market analysis, analysis of profit and loss factors, analysis of income and expenditure indexes, analysis of investment risks, management ability, business ability, allotment and operation plan, investment payback plan, sustainability, eco-friendly factor, and proptech. Based on the hierarchy above, the relative importance of valuation factors was derived by considering policy and economic aspects to correct weights. In this way, the importance of each valuation factor was quantified objectively.

This study adopts both methodologies for the analysis, and the model was established to secure suitability and minimize the error range. Based on the bidding result of each workplace of non-performing PF, this study suggests a new real estate development valuation based on the types and characteristics of each development project.

2. Theoretical Investigation

2.1. Concept and Characteristics of Real Estate PF

Real estate PF (Project Financing) is a financial method to procure funds by utilizing future cash flows as a significant source for redemption to attract investments from financial companies for specific real estate development projects. In Korea, real estate PF was first introduced after the IMF crisis in 1997, and this system was established as a primary mechanism to expand subjects of large-scale real estate businesses to cover the private sectors after the global financial crisis originating from the US in 2008 [10,11].

Real estate PF is a way of procuring funds for development projects with cash flows in the future as security. In other words, when the business operator is to pay back the principal, it generally depends on the project cash flows. However, a real estate development project involves a tremendous amount of investment in line with the rapidly changing real estate market condition, and thus, more than assets related to the development project are involved in such cash flows [12,13]. Most real estate development projects are long-term and thus cannot flexibly cope with drastic changes in the real estate market. Therefore, the business operator’s credibility among interested parties is also essential. An escrow account is installed and managed as a trust account to secure fund management thoroughly. All earnings from projects are deposited into this trust account, and withdrawal is practiced in the order agreed upon in advance [14,15].

Real estate PF in Korea operates in the way specified for financing from the development step. Thus, funding in the steps of business preparation and construction is essential. Since a financial company is responsible for funding in the initial stage of the business, credit offering by the constructor is required [16]. On behalf of the company conducting a project, the parent company or constructor bears the risks in general. If a special purpose company responsible for the development project is independently established for PF, the parent company’s foreign credit is unaffected [17,18].

2.2. Investigation of Previous Studies

There have been various studies on non-performing real estate PF, which may be classified into two. The first studies the causes of non-performing PF, like studies on bid and investment decision factors for non-performing real estate [5]. PF aims to maximize assistance to promote the national economy and development industry [19]. In Korea, however, aspects to maximize the parent company’s profits are prioritized, and thus, PF is increasing rapidly and thoughtlessly. Due to the recent financial crisis and the crisis in the real estate market, many construction sites have suspended the project, one after another [20]. This is because there is no proper valuation system for quantitative analysis and control of risks for objective PF valuation [21,22]. Many studies and suggestions have been made to address this problem. However, PF is a financial method developed in the limitation of Korea’s development industry and real estate market. Therefore, it has limitations in improving or quickly normalizing the structure in line with the rapidly changing financial market. One realistic method for prompt normalization, thus, is to promote large constructors’ quick decision-making regarding investment into workplaces of non-performing PF. Many projects, however, have been canceled or suspended due to differences in the recognized importance of decision-making among agencies and financial companies, including large constructors in reality [23]. For this reason, investment decision factors are vital. When the empirical analysis is conducted, the importance of each investment decision factor needs to be derived, and the hierarchy needs to be schematized in consideration of various aspects, including policy and economic characteristics, with the grounds clarified [24,25,26]. Many overseas studies have analyzed significant causes, focusing on project delays that result in non-performing PF. This study points out project delay factors such as climate, communication, disputes among interested parties, inefficiency of project plans, lack of materials and financing, delayed payment, lack of capabilities, etc. [27]. Similar studies also identify PF risk factors and suggest a risk management system suitable for the project planning step [28]. On the assumption that the way of investment into real estate PF is a cause of PF, some studies argue that crowdfunding with ordinary citizen participants needs to be considered as one limitation of PF funding is related to the existing escrow account [29].

The second suggests ways to handle non-performing real estate PF, including revitalizing the market and improving the current status of real estate PF and related policies. The economic decline in the real estate market that has continued for an extended period is likely to lead to the non-performance of real estate PF and a crisis in the construction industry and the financial sector [30]. For this reason, many studies discuss policies, normalization methods, and improvement plans for the crisis of real estate PF. Among them, some studies examine the structural problems of Korean real estate PF and suggest fundamental plans for them [31]. Some similar studies examine the current condition of construction and finance markets and compare overseas development finance, with domestic ones focusing on real estate PF. Some studies suggest improvement plans to minimize non-performing real estate PF and settle sound real estate PF [32]. Some studies present suggestions to revitalize real estate PF and address its issues, including the following: a review of policies related to real estate PF, the establishment of a dedicated system for business feasibility assessment, the foundation of a professional real estate PF assurance agency, division of risks burdened on the constructor, and revision of related laws [33,34]. Regarding real estate PF, some studies argue that legal problems linked to types of capital structures, credit preservation, and execution procedures need to be reviewed and that legal security solutions and institutional operation methods to secure the stability of development projects need to be developed [35]. In addition, some studies suggest that actual management cases need to be analyzed for the efficient management of workplaces of non-performing real estate PF, presenting related indexes such as workplace scrutiny, additional funding, thorough fund management, contract management, lot sale management, cash flow management, construction work management, etc. [36]. Similar studies present suggestions for revitalization, such as fundraising for real estate PF business feasibility assessment led by a public enterprise, regional allocation of PF, traceability of constructors and operators, etc. [37]. While the above-stated studies focused on domestic real estate PF, other studies analyzed overseas real estate PF cases with a focus on performing effective project development, increasing the success possibility of projects, minimizing development project risks, and creating practical project evaluation factors [38]. Despite many studies, however, there has been no specific discussion on arrears or delays resulting from failing to consider all the internal and external characteristics of real estate PF, as pointed out frequently. Moreover, studies on the unitary valuation method and system are insufficient. Therefore, this study adopts both methodologies to differentiate itself from previous studies. First, the spatial scope of regression analysis variables was set to address the simplification of restrictions, and internal and external factors were considered. Analysis results were utilized to set the hierarchy, while a literature review and a survey of experts were conducted before the AHP analysis. Focus Group Interviews (FGI) were likewise undertaken to minimize the error range. The final model was decided to secure the suitability of the derived study model. This study suggests minimizing construction suspension and delays in non-performing real estate PF and applying such items to the valuation system of new development projects.

3. Analysis of Bid Decision Factors for Workplaces of Non-performing Real Estate PF

3.1. Variables

As for variables, the bidding result of each constructor was set as the dependent variable: the workplace of a successful bidding was set to ‘1’ (dummy variable), while the workplace of a failed bidding was set to ‘0.’ Regarding factors affecting the bidding result, under the high classification of real estate development project valuation in previous studies, relevant factors were divided into the five following groups and used as independent variables: business feasibility assessment, land lot basic evaluation, work performance assessment, and investor protection plan. Internal factors were divided mainly into building characteristics, profitability analysis, business steps, and debt settlement. External factors were divided into the review of legal aspects, administrative elements, transportation facilities, cultural and convenience facilities, and education facilities. These factors were set in reference to variables in business plans at each workplace and in previous studies. Among sub-variables, a 5km radius distance is a linked traffic distance stated in transportation geography. This variable was included since the distance from each facility within 10 minutes is considered significant for success.

Table 1.

Variables.

| Variable name | Description | Remarks | ||

|---|---|---|---|---|

| Dependent variable | Bidding result | Based on the bidding result of each constructor was set as a dependentA successful bidder: 1, A failed bidder: 0 |

Subfactor of dummy | |

| independent variables | ||||

| Feasibility assessment | Building characteristics | Floor area ratio | Land area to total ground area ratio | % |

| Feasibility assessment | Building characteristics | Building-to-land ratio | Land area to building area ratio | % |

| Feasibility assessment | Building characteristics | Scale | No. of households in the building | Unit |

| Feasibility assessment | Profitability analysis | Profitability | Financial feasibility analysis result | % |

| Target site basic evaluation |

Legal risk review | Legal suitability | No. of legal disputes | Case |

| Target site basic evaluation |

Administrative review | License acquisition | License acquisition | Subfactor of dummy |

| Target site basic evaluation | Transportation means | Subway in a radius of 5km | No. of subway stations in a radius of 5km | Unit |

| Target site basic evaluation | Cultural and convenience facility | Adjacent movie theaters | Distance from the building to the nearest movie theater | km |

| Adjacent large outlets | Distance from the building to the nearest outlet | km | ||

| Outlet in a radius of 5km | No. of outlets in a radius of 5km | Unit | ||

| Target site basic evaluation | Educational facilities | Elementary/middle/high school/university in a radius of 5km | No. of schools in a radius of 5km | Unit |

| Business performance evaluation | Business step | Business site buying rate | The percentage of business sites where the purchase is completed among business sites required in the project plan | % |

| Business performance evaluation | Business step | Period of business suspension | Total period during which the construction is suspended in the project schedule | No. of months |

| Investor protection plan | Debt info. | Total amount of bonds (a) | Total amount of bonds for the building | x 1 million won |

| Investor protection plan | Debt info. | Amount of obtained bonds (b) | Amount of obtained bonds | x 1 million won |

*The table above modifies and complements the variables of Shim Hui-cheol and Kim Jae-hwan (2017).

3.2. Descriptive Statistics

As the descriptive statistics analysis was performed before the empirical analysis, the basic statistics are shown in Table 2 below. Regarding the bidding result, which is a dependent variable, there were 15 successful bidding places among non-performing buildings (46.88%) and 17 failed bidding places (53.12%). Among independent variables, the business site buying rate in the business step was 91.3% on average, which indicates that the land buying rate was favorable. On the other hand, the period of business suspension was from about 42 months on average to 111 months, which indicates that normalization was not practiced actively. As for debt information variables, including the amount of obtained and total bonds, the obtained bond ratio was 78.11% on average. Among cultural and convenient facilities, which were independent variables, movie theaters and large outlets adjacent to a workplace were located at a distance of 2.47km and 2.684km on average. The movie theater and outlet were located at the farthest distance from the workplace, 14.68km and 11.63km away, respectively, which, in other words, was within 20 minutes by car.

3.3. Correlation Analysis

Before regression analysis, correlation analysis was performed to identify highly correlated variables and remove some, if necessary, to prevent problems of multicollinearity among independent variables. While many studies did not consider multicollinearity, this study includes correlation analysis to clarify each variable’s contribution and simplify the model more. The results are presented in Table 3.

Items in a positive correlation reflect the similarity with the construction indexes regarding floor area ratio, building coverage ratio, and location. Notably, items indicating the aggregation of commercial and educational facilities were highly correlated. Items in a negative correlation indicate the scale, bidding result, legal suitability, and the relation with certain facilities such as the number of certain facilities within a radius of 5km. This means that the physical size or legal requirements of a project may affect its success or failure. Correlation analysis results show that variables whose correlation coefficient was at least 0.8 included the floor area ratio and building coverage ratio, the distance from an adjacent movie theater and the number of schools in a radius of 5km, the distance from an adjacent large outlet and the number of schools in a radius of 5km, and the total amount of bonds and the amount of obtained bonds. Based on analysis results, certain variables—floor area ratio, distance from an adjacent movie theater, distance from an adjacent large outlet, and amount of obtained bonds—were excluded. These variables were excluded for the following reasons: First, the floor area ratio was excluded while the building coverage ratio remained because the latter is an indicator of the business scale or use and thus could contribute to regression analysis. Second, to represent the living infrastructures within the neighborhood, the distance from an adjacent movie theater was excluded while the number of schools within a radius of 5km remained. Third, to reduce the duplication of commercial/educational facilities and include the living infrastructures, the distance from an adjacent outlet was excluded while the number of schools within a radius of 5km remained. Finally, the amount of obtained bonds was excluded while the total amount remained because the latter could represent the scale of bonds. Thus, 4 highly correlated variables were excluded from 15 basic independent variables, with the rest (11) used in the analysis.

3.4. Model Fitness

The analysis model is shown in Table 4 below. The value of -2 Log Likelihood was 78.524, and the factors representing the same usefulness regarding the model fitness included the R-square of Cox and Snell and the R-square of Naglekerke, which accounted for 52.1% and 65.8% of the whole dispersion, respectively.

In addition, statistics of the Hosmer-Lemeshow Test representing the model fitness are as in Table 5. The Pierson Chi-square value was 9.753, and the significance probability was 0.247, more significant than 0.05. Thus, the model fitness was substantial.

3.5. Bid Decision Factor Analysis

This study utilizes 11 independent variables to understand and analyze factors that affect successful bidding. Variables used in the analysis were restructured in view of multicollinearity based on variables utilized in previous studies. According to analysis results, variables with a significant value included building coverage ratio, scale, profitability, license, subway within a radius of 5km, outlet within a radius of 5km, business site buying rate, period of business suspension, and total amount of bonds. The results of the analysis of significant variables were interpreted as follows: As to the building coverage ratio, B had a negative value of –31.3215, which indicates that as the building coverage ratio was high, the probability of successful bidding decreased. The scale value B was -0.0684, a small and significant value. This suggests that as the scale increased, the likelihood of successful bidding decreased to an insignificant extent. The profitability value was –28.5572, a negative value. Thus, it suggests that the probability of successful bidding was significantly reduced as the profitability was high. The license value B was –26.7496, a negative value. It was significant at a significance level of 99%. This means the probability of successful bidding decreased significantly when there was a license. As to a subway within a radius of 5km, the B value was –3.0774, a negative value. This suggests that as there was no subway nearby, the probability of successful bidding increased. As to an outlet within a radius of 5km, the B value was 2.1577, a positive value. This suggests that as there was no subway nearby, the probability of successful bidding increased. As to the business site buying rate, B had a negative value of –26.9258, which indicates that as the rate was high, the probability of successful bidding decreased. As to the period of business suspension, the value B had a negative value of –0.3643, which indicates that as the period was extended, the probability of successful bidding decreased. The total amount of bonds, Exp(B), was close to 1. This means that as the amount of bonds increased slightly, the probability of successful bidding increased slightly with no significant effect.

Table 6.

Analysis result.

| Classification | B | S.E. | Wald | Degree of freedom | Significant probability | Exp(ᵝ) | |

| Step 1 | Building coverage ratio(%) | -31.3215 | 6.8623 | 20.833 | 1.0 | 0.0 | 0.0 |

| Scale(Unit) | -0.0684 | 0.0175 | 15.2359 | 1.0 | 0.0001 | 0.9339 | |

| Profitability(%) | -28.5572 | 6.9241 | 17.0098 | 1.0 | 0.0 | 0.0 | |

| Legal suitability(Case) | -2.404 | 1.8507 | 1.6872 | 1.0 | 0.194 | 0.0904 | |

| License acquisition (Subfactor of dummy) | -26.7496 | 7.2176 | 13.7355 | 1.0 | 0.0002 | 0.0 | |

| Subway in a radius of 5km (Unit) | -3.0774 | 0.8723 | 12.4458 | 1.0 | 0.0004 | 0.0461 | |

| Outlet in a radius of 5km (Unit) | 2.1577 | 0.6487 | 11.0628 | 1.0 | 0.0009 | 8.651 | |

| Elementary/Middle school/High school/University within a 5km radius(Unit) | -0.0285 | 0.0365 | 0.61 | 1.0 | 0.4348 | 0.9719 | |

| Business site buying rate(%) | -26.9258 | 7.5165 | 12.8322 | 1.0 | 0.0003 | 0.0 | |

| Period of business suspension(No. of months) | -0.3643 | 0.0998 | 13.3163 | 1.0 | 0.0003 | 0.6947 | |

| Total amount of bonds (x 1 million won) |

0.0005 | 0.0001 | 15.3272 | 1.0 | 0.0001 | 1.0005 | |

| Constant term | 21.3263 | 3.3149 | 16.0176 | 1.0 | 0.0001 | 0.9128 | |

In summary, major variables affected the bidding result to a significant extent. Certain factors, such as building coverage ratio, scale, profitability, and license, were essential variables of the probability of successful bidding. Based on the analysis result, the following academic and policy implications can be derived:

As to academic implications, first, a high building coverage ratio can weaken the economic feasibility of the project. Therefore, future studies may examine the relationship between the building coverage ratio and successful bidding from a diversified perspective to understand the various effects of the building coverage ratio on the economic feasibility of real estate development. Second, it is necessary to reconsider the importance of location factors. The result is that location factors such as an outlet within a radius of 5km affect the probability of successful bidding significantly, supporting the assumption that local infrastructures affect the value of the real estate. In future research on location factors, this analysis result can be utilized as empirical proof for economic value analysis.

As to policy implications, first, the criteria of the building coverage ratio and policies for scale restriction need to be reconsidered. The analysis suggests that the building coverage ratio and scale may affect the economic feasibility of the real estate market. Therefore, related policies need to be reconsidered to reduce unnecessary investment into large-scale projects and to induce projects of a proper scale that can secure economic feasibility. Second, as convenient facilities such as outlets are located nearby, the probability of successful bidding increases. This suggests the importance of local infrastructure development for revitalizing real estate. Thus, the government needs to consider ways to contribute to economic revitalization and increase real estate value when establishing a development plan for infrastructure. Third, the possibility of successful bidding in real estate projects whose licensing was completed decreased because the economic validity was likely to decrease as the selling price increases due to the decrease of initial risks. Accordingly, the government needs to establish risk management policies such as consulting service and public guarantee scheme to manage risks of projects in the initial state and to attract investments more effectively. Fourth, the possibility of successful bidding in real estate projects of high profitability decreased probably because actual risks were not properly reflected while the bidding competition was fierce and the expected rate of return was high. Therefore, it is necessary to develop policies to control the bidding competition to a proper level and to create transparent and fair competition environments. In addition to that, ways to establish a public database and to secure the transparency and accessibility of information need to be considered for clear understanding of actual risks of projects and expected rates of return. As a result, long-term and sustainable development in the market will be promoted. Such implications may be referred to in decision-making and legislation related to real estate development. Future studies based on empirical data can also contribute to more systematic analysis and policy suggestions.

4. Valuation Basis in Consideration of Bid Decision Factors

4.1. Hierarchy Setting

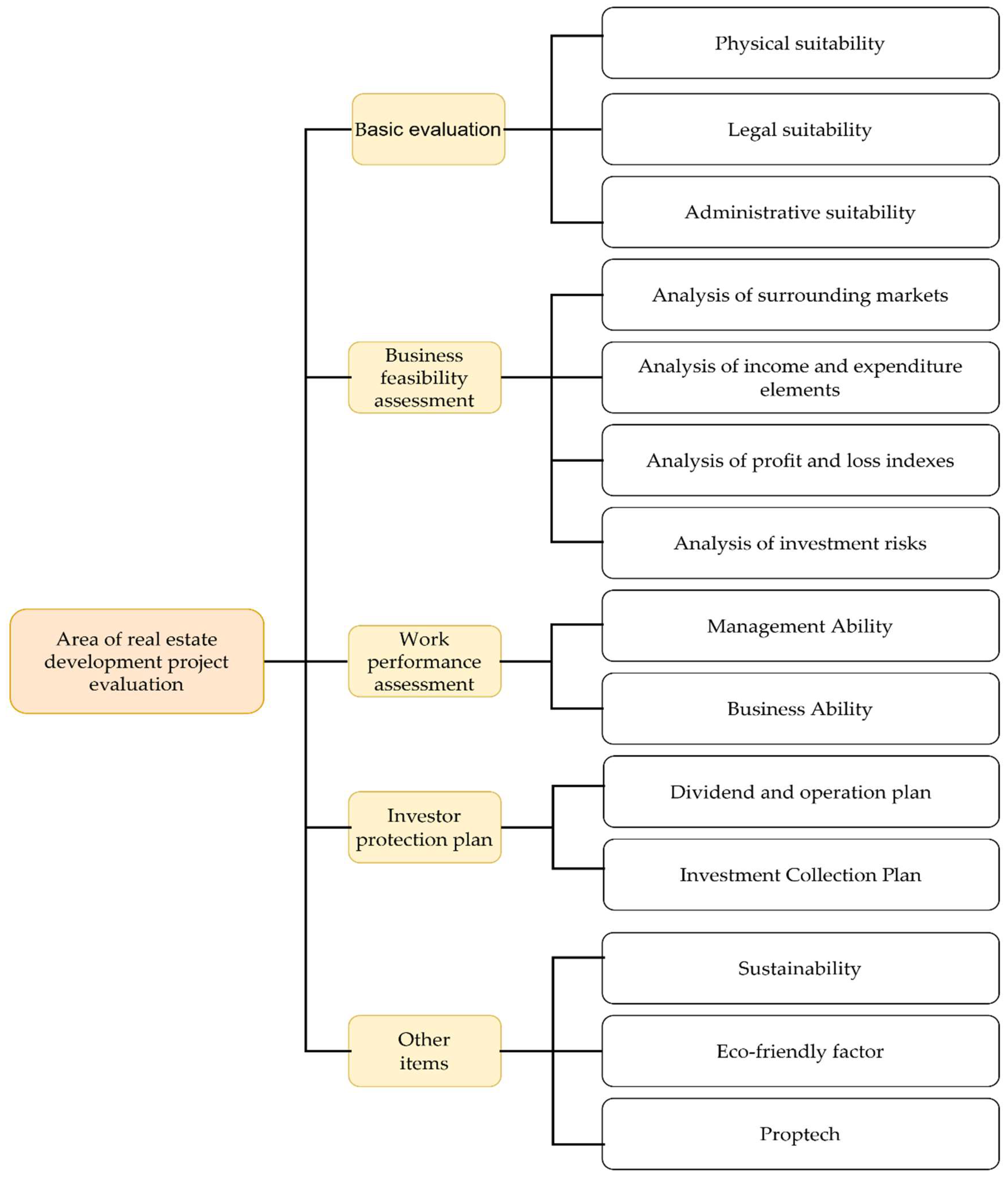

This chapter presents the hierarchy diagram to establish the valuation criteria of real estate development projects that sufficiently reflect bid decision factor analysis results in Chapter 3. To this end, various previous studies and references related to valuation of real estate development projects are examined in addition to the findings of this study such as Jeong Hui-nam et al. (2013), Ahn Guk-jin at al. (2014), Lim Ui-taek et al. (2016), and Shim Hui-cheol et al. (2017). Policy and economic aspects were also considered and specified to schematize the hierarchy and secure the grounds. The established hierarchy consisted of 2 layers and included high classification and sub-items, such as basic evaluation (target site), business feasibility assessment, work performance assessment, and investor protection plan.

Prior to business feasibility assessment and work performance assessment for a real estate development project, basal evaluation needs to be conducted first to examine the PF potential. To determine subordinate items of basal evaluation, this study suggests elements to evaluate the licensing and business appropriateness of a project area based on physical, legal, and administrative suitability. For business feasibility assessment, subordinate items were classified based on the following four factors: First, analysis of adjacent markets is defined as an item to evaluate market environments including such factors as real estate policy trend, location, demand and supply, etc. Second, analysis of profit and loss factors focuses on evaluating the sale and occupancy rate and the value increase rate after development. Third, analysis of profit indexes is to evaluate the return on investment and cash flow based on loan and profit indexes. Fourth, analysis of investment risks is to evaluate the ratio of one’s own equity, dependence on the sale price, etc. based on the analysis of capital soundness and the developer’s fund raising and redemption. Work performance assessment consists of two subordinate items: business ability and management ability. The business ability means the ability to conduct a development project stably on the basis of the business operator’s experience and credibility. The management ability means the ability for a business organization to perform the development project in a systematic and effective manner. An investor protection plan consists of two subordinate items: dividend and operation plan and investment payback plan. The dividend and operation plan is defined as an element to evaluate the appropriateness of the rate of dividends and the validity of a fund plan. The investment payback plan is defined as an element to protect the investor. Finally, this study suggests three additional elements: eco-friendly factor, sustainability, and proptech. These elements were selected as important items that can contribute to the long-term development and transparency of the real estate market.

Finally, the hierarchy was set as in Figure 1. Based on the system of valuation given bid decision factors of PF workplaces involving construction suspension, analysis is performed in reflection of the types and characteristics of businesses in each real estate development project valuation area. In addition, the finalized analysis results are rearranged depending on priority and importance, and then the higher ranks are determined. The ranks were determined in the order of final correction values. The higher rank, the higher importance.

4.2. Survey Overview and Details

To form a new valuation basis, including successful bid factors, and to apply weights to each item, a survey was conducted among experts, with 70 copies distributed via e-mail, personally, and Focus Group Interview(FGI). The judgment sampling method was utilized. Two copies that were not collected and 5 copies whose statistical consistency was 0.1 were excluded, while the remaining 63 valid copies were used in the analysis. Samples for this study were selected based on their understanding of local financial investment projects and their tasks and previous research projects. The survey was conducted among the following participants: 27 university professors (42.85%), 16 researchers at central or local government research centers (25.39%), 7 representatives or employees at architect offices or engineering companies that participated in a feasibility study (11.11%), and 13 other experts or public officers (20.63%). The characteristics of these samples were viewed as appropriate to represent the results of weighting and the real estate development project valuation system to be suggested by this study.

4.3. Analysis Result

The AHP was performed to classify bid decision factors of non-performing real estate PF into layer 1, layer 2, and layer 3. The relative importance of each valuation item is shown in Table 7. The most crucial element was an analysis of income and expenditure elements (final correction value: 0.1020; rank: 1). The item significantly affects the probability of successful bidding and economic achievement. The following elements were business performance (final correction value: 0.1008; rank: 2) and dividend and operation plan (final correction value: 0.1007; rank 3). Therefore, the ability to perform and operate a business and the validity of investor protection plans are essential. In addition, analysis of profit and loss indexes (rank 4) and management ability (rank 5) factors were among priority items, meaning that profitability, profit index analysis, and management ability are essential in evaluating businesses’ financial stability. Such items are of high rank because financial achievements are critical to the success of real estate projects. Likewise, such factors as legal suitability (rank 6) and administrative suitability (rank 7) significantly affect the stability of projects. Compliance with regulations and harmony with public policies are also essential. In contrast, physical suitability (rank 14) was relatively low because projects are more affected by financial, policy, and legal factors than existing physical environments. This result suggests that financial validity, legal and policy suitability, and investor protection significantly affect the successful bidding of real estate projects. Therefore, policymakers and investors must carefully examine businesses’ financial achievement and legal and policy suitability. Notably, the importance of analysis of income and expenditure elements, business performance ability, and investor protection plans was significant. Thus, these three elements must be carefully managed for the success of projects.

Based on these AHP analysis results, the following academic and policy implications have been derived. For academic implications, first, the priority of a new valuation basis was derived by applying the AHP method. Thus, it became possible to compare the relative importance of each class through the structural analysis of multiple hierarchical elements. This can be utilized as a practical instrument to systematically evaluate the success factors of real estate projects. Second, the importance of financial validity and business performance was reconfirmed. Financial validity indexes such as analysis of income and expenditure elements and analysis of profit and loss indexes were necessary, which is an academic base for the importance of economic achievements in the success of real estate PF. Additionally, the result that business performance significantly affected project achievements supports the theoretical view emphasizing the importance of project management and execution abilities. Third, location elements such as an outlet within a radius of 5km were viewed as less important than financial validity and business ability because economic, legal, and policy elements should be prioritized in real estate projects. In contrast, weights for location factors should be a supplementary element.

Policy implications include the following. First, financial factors and legal suitability were viewed as high priorities. Thus, the government must strictly consider economic validity and regulation compliance when assessing each real estate project. Based on this result, the government needs to intensify its profitability and legal suitability reviews in the early stages of each real estate project. Second, investor protection plans and management ability were viewed as high-ranked bid decision factors, which suggests that, from a policy perspective, real estate projects need to secure stable profit distribution and management transparency. Therefore, investor protection plans and operation ability need to be considered in the valuation criteria of projects so that investment risks are minimized and long-term reliability is secured as part of policy standards. Third, factors such as sustainability and proptech were viewed as relatively less essential but need to be complemented from a policy perspective. This is because sustainability and the introduction of proptech can contribute to the development and transparency of the real estate market in the long run. Therefore, the academic and policy implications stated above are expected to serve as basic data for the long-term sustainable growth of the real estate industry, specifically for real estate project evaluation and policy making.

5. Conclusion

5.1. Summary and Implications

This study examines factors that affect the successful bidding of 32 workplaces of non-performing real estate PF through regression analysis and AHP, sets the hierarchy, and establishes a new standard for weighting the valuation system. According to the regression analysis result, the critical factors for successful bidding include the following: business feasibility assessment (building coverage ratio, scale, profitability), basic evaluation of sites (license, transportation means, cultural and convenient facility), work performance assessment (site buying rate, period of business suspension), and investor protection plan (total amount of bonds). Factors that affect the success of bids were thoroughly examined as below: First, the building coverage ratio showed a negative correlation (value of B: -31.3215), and which indicates that as the building coverage ratio is high, the probability of successful bidding is likely to decrease. Therefore, the increase of building coverage ratios may reduce the economic validity and does not conform to legal standards or standards for urban planning. An excessively high building coverage ratio may hinder the legitimacy and licensing probability of a real estate project. It also suggests that as the real estate market tends to prefer low-density buildings, the acceptability may decrease. Second, the scale showed a delicate negative correlation (value of B: -0.0684), which indicates that as the real estate project scale increases, the probability of successful bidding is likely to decrease. This is because a relatively large project requires of more capital and resources, increasing the risk and lowering the investment profitability as a result. Third, the profitability showed a high negative correlation (value of B: -28.5572). As the profitability increased, the probability of successful bidding tended to decrease. The cause may be the excessive bid competition in a highly profitable real estate project or the failure of reflecting actual risks in an estimation of high rates of return. Fourth, licensing showed a negative correlation (value of B: -26.7496), which suggests that once the licensing of a real estate project is completed, the probability of successful bidding decreases. If licensing is completed, the initial risk decreases while the selling price increases. As a result, the economic validity is likely to decrease. Fifth, traffic, cultural, and convenience facilities were examined as below: The number of subway stations within 5km showed a negative correlation (value of B: -3.0774), which indicates that an excessive traffic network may rather hinder the economic feasibility of a real estate project. In contrast, the number of large outlets within a radius of 5km showed a positive correlation (value of B: 2.1577), which indicates its positive effect on the probability of successful bidding. This analysis result shows that the accessibility to living convenience facilities increases the probability of successful bidding in a real estate project. Sixth, the business site buying rate and the period of business suspension showed a negative correlation (value of B: -26.9258, -0.3643). As the business site buying rate was high or the period of business suspension was long, the probability of successful bidding decreased. This result indicates that a construction delay or additional expense in a process of real estate project implementation may hinder the economic validity of the project. Finally, the total amount of bonds showed an insignificant positive correlation with the probability of successful bidding (Exp(B): close to 1). This result indicates that as the value of bonds increases, the increase of the probability of successful bidding may be affected delicately, and that ensuring investors’ trust affects the probability of a real estate project’s success. Additionally, the following factors were verified by AHP as priorities: business feasibility assessment (analysis of income and expenditure elements), work performance assessment (business ability), investor protection plan (dividend and operation plan), business feasibility assessment (analysis of profit and loss indexes), work performance assessment (management ability), and basic evaluation (legal suitability and administrative suitability) and based on the comprehensive review of the two analysis results stated above. Certain factors—business feasibility assessment, work performance assessment, and basic evaluation—played a key role in the success and successful bidding of real estate projects. It is necessary, therefore, to set strict standards for financial achievements and project performance capabilities. The government and regulatory agencies need to evaluate the financial validity of each real estate development project and strengthen standards so that only projects whose economic achievement to a certain degree is estimated can be approved. In addition, the legal suitability of legal regulations and administrative suitability of licenses are closely related to bid decision factors. Therefore, policy improvement must be achieved to reduce legal and administrative risks by clarifying legal requirements and complicated administrative procedures. Additionally, investor protection plans were highly ranked among bid decision factors, which suggests the necessity of establishing investor protection measures and securing their reliability. Accordingly, the government must develop policies to ensure real estate investment projects’ reliability and transparency to attract investors and provide stable and predictable profits. Finally, other elements such as sustainability, eco-friendliness, and proptech were found to be in a low rank but included among items of correction values. This means that social interests in environments and innotative technologies such as proptech, even if they are low-rank elements, affect the economic value of real estate development projects in the future. It is necessary, therefore, for the government to provide incentives that promote sustainable development and application of innovative technologies to real estate development projects. These various academic and policy implications show the necessity of diversified and scientific approaches to the potential of success in real estate projects.

5.2. Limitations and Future Issues

This study selected variables based on previous studies, and correlation analysis was additionally conducted to minimize multicollinearity problems. The spatial scope was also added to consider both internal and external factors of PF by adopting the two methodologies. Based on such significant variables and the established hierarchy, this study could assess the weights of each valuation basis and secure the suitability of the study model, with the error range minimized. On the other hand, however, the study was conducted only with 32 samples of successful bidding from KAMCO, which is a limitation of this study since it could not derive more diversified variables. This was because it was challenging to collect data on PF workplaces. However, future research is expected to produce more meaningful results by utilizing more variables as long as sufficient data on domestic PF workplaces are accumulated and information on internal and external factors is more effectively acquired.

Author Contributions

T.K. conceived, designed, analysed, and wrote this paper. H.S, S.K. advised on this research, from concept to writing. Both authors have read and agreed to the published version of the manuscript.

Funding

This research received no external funding.

Acknowledgements

This work was supported by a research grant from the Kongju National University in 2023.

Conflicts of Interest

The authors declare no conflict of interest.

References

- Financial Supervisory Service. Evaluation of financial companies’ business feasibility and plans regarding their real estate PF. Available online: https://www.fss.or.kr/fss/bbs/B0000188/view.do?nttId=137993&menuNo=200218&cl1Cd=&sdate=&edate=&searchCnd=1&searchWrd=&pageIndex=4 (accessed on 21 November 2024).

- Bank of Korea. 2024. Global Financial Stability Report.

- Financial Supervisory Service. The 4th meeting of measures for soft landing of real estate PF. Available online: https://www.fss.or.kr/fss/bbs/B0000188/view.do?nttId=137993&menuNo=200218&cl1Cd=&sdate=&edate=&searchCnd=1&searchWrd=&pageIndex=4 (accessed on 21 November 2024).

- Maeil Business Newspaper. News Report. Available online: https://www.mk.co.kr/news/economy/11105179 (accessed on 21 November 2024).

- Shim, H.C.; Kim, J.H. Analysis of determinants of successful bidding for insolvent PF projects: With a focus on PF establishments whose construction was suspended by mutual savings banks. Real Estate Acad Rev 2018, 71, 93–104. [Google Scholar]

- Korea Asset Management Corporation (KAMCO). Internal data (2017). Available online: www.kamco.or.kr (accessed on 21 November 2024).

- Shin, J.C.; Baik, M.S. Research on the Normalization Schemes for Insolvent Development Site on Mutual Savings Banks. J Korea Academia-Industrial Coop Soc 2015, 16, 195–204. [Google Scholar] [CrossRef]

- Jo, K.H.; Lee, C.K. , Kim, S.J. Improving local investment appraisal system for local public investment efficiency. Korea Res Inst for Local Adm Basic Res Proj 2012, 1–217. [Google Scholar]

- Shim, H.C. , Kim, J.H. A Study on the Application of Weights in the Area of Regional Development for the Examination of Local Financial Investment Project. J Resid Environ Inst Korea 2020, 18, 43–56. [Google Scholar] [CrossRef]

- Hong, S.J. Legislative tasks of real estate PF measures to normalize the real estate market. Korea Publ Land Law 2024, 134, 105–133. [Google Scholar]

- Nevitt, P.K.; Fabozzi, F. Project Financing 6th Edition; Euromoney Publication: London, UK, 1995. [Google Scholar]

- Yang, K.J. An Exploratory Study on Project Financing of Korea Mutual Savings Banks. Corp Law Res 2011, 25, 299–328. [Google Scholar]

- Esty, B.C. Modern Project Finance: A Case Book; John Wiley & Sons: Hoboken, NJ, USA, 2004. [Google Scholar]

- Jang, S.H. 2013. A Study on Improvement of Project Financing Structure and New Directions in Real Estate Market: Focusing on Financing Structure Founded on Risk Taking of Financial Institutions. Master’s Thesis, Konkuk University Real Estate Graduate School, Seoul, South Korea.

- Wood, P.R. Project Finance, Subordinated Debt and State Loans; Sweet & Maxwell: London, UK, 1995. [Google Scholar]

- Yoon, Y.S.; Sung, J.H. A Study on the Efficient Risk Management with the Relative Importance of Risk Facts by Stage in the Real Estate Development Project. Korea Real Estate Acad 2014, 59, 59–73. [Google Scholar]

- Merna, A.; Chu, Y.; Al-Thani, F. Project Finance in Construction: A Structured Guide to Assessment; Wiley-Blackwell: Hoboken, NJ, USA, 2010. [Google Scholar]

- Finnerty, J.D. Project Financing: Asset-Based Financial Engineering; John Wiley & Sons: Hoboken, NJ, USA, 2013. [Google Scholar]

- Kim, J.J. Diagnosis on Project Finance Crisis in Real Estate Market and Policy Response. Constr Issue Focus 2022, 1–34. [Google Scholar]

- Kim, J.J. Diagnosis on Project Finance Crisis in Real Estate Market in Korea and Policy Suggestion. Future Growth Stud, 2023, 9, 101–128. [Google Scholar] [CrossRef]

- Ahn, W.H. 2011. A study on factors of the financial distress and the soundness of the mutual savings banks in Korea. Master’s Thesis, Yonsei University, Seoul, South Korea.

- Lee, D.G.; Cha, H.S. An Exploratory Research on Quantitative Risk Assessment Methodology Throughout Success Factor Analysis in Project Financing. Korean J Constr Eng Manag 2013, 14, 92–102. [Google Scholar] [CrossRef]

- An, K.J.; Cho, Y.K.; Lee, S.Y. An Analysis on the Investment Determinants for Insolvent Housing Development Projects. Korean J Constr Eng Manag 2015, 15, 112–121. [Google Scholar] [CrossRef]

- Choi, H.S. The Effect of the UEC on the Price of Nearby Lands: Focused on Times Square UEC. Korea Real Estate Acad Rev 2014, 58, 60–71. [Google Scholar]

- Lim, E.T.; Lee, H.B. A Research on the Impact of the NPL Related Factors on the Auction Winning Price Rate of Real Estates. Korea Real Estate Acad Rev 2016, 67, 116–128. [Google Scholar]

- Ong, S.E.; Lusht, K.; Mak, C.Y. Factors Influencing Auction Outcomes: Bidder Turnout, Auction Houses and Market Conditions. J Estate Res 2005, 27, 181. [Google Scholar] [CrossRef]

- Durdyev, S.; Hosseini, M.R. Causes of delays on construction projects: a comprehensive list. Int J Manag Proj Bus 2020, 13. [Google Scholar] [CrossRef]

- Voronina, N.V.; Steksova, S.Y. Project finance risk management at the stages of the housing projects’ life cycle. Mater Sci Eng 2020, 913. [Google Scholar] [CrossRef]

- Kurmanova, L.R.; Kurmanova, D.A. Financial technologies in project financing of housing construction. Mater Sci Eng 2020, 753. [Google Scholar] [CrossRef]

- Kim, J.; Ji, K.H. Current status of real estate PF (Project Finance) loans and policy responses. Available online: https://eiec.kdi.re.kr/policy/domesticView.do?ac=0000150505 (accessed on 22 November 2024).

- Lee, B.G.; Lee, C.W. Research on real estate PF crisis response plan. Korean Law Rev Rehabilit Bankruptcy 2024, 28, 75–116. [Google Scholar] [CrossRef]

- Choi, E.Y. Actual Status of Real Estate PF Loans and Improvement Measures. Constr Econ 2011, 66, 68–79. [Google Scholar]

- Shin, K.H. Study of Analysis of Real Estate Project Financing Issues and Activated through Improvement of a System. Inst Leg Stud 2015, 11, 181–215. [Google Scholar]

- Son, J.J. 2009. A Study on Improvement and Problems of PFV System in Korea: Focused on Real Estate Development Business. Master’s Thesis, Kangnam University, Gyeonggi-do, South Korea.

- Cho, J.Y. A Study on the Measure of Securing Stability of the Project Finance. Korea Real Estate Acad Rev 2016, 64, 268–280. [Google Scholar]

- You, J.G.; Oh, D.H. Efficient Management Scheme for Insolvent Development Site in Real Estate Project Financing. J Korea Real Estate Anal Assoc, 2010; 16, 99–114. [Google Scholar]

- Lee, G.B. A Study on How to Activate Small and Medium-sized Real Estate Development PF. J Humanit Soc Sci 2020, 11, 2205–2216. [Google Scholar]

- Chung, B.K.; You, D.M. Strategies for vitalizing the domestic real estate PF market: Focusing on domestic and foreign precedent research analysis. Korea Real Estate Soc 2023, 41, 159–182. [Google Scholar] [CrossRef]

Figure 1.

Hierarchy.

Table 2.

Basic statistics.

| N | Ave | Std | Min | Max | |

| Bidding result (Subfactor of dummy) |

32.0 | 0.4688 | 0.4998 | 0.0 | 1 |

| Floor area ratio(%) | 32.0 | 3.2681 | 2.4196 | 1.53 | 10.56 |

| Building-to-land ratio(%) | 32.0 | 0.2616 | 0.1527 | 0.13 | 0.66 |

| Scale(Unit) | 32.0 | 515.9688 | 465.4663 | 38.0 | 2059 |

| Profitability(%) | 32.0 | 1.2428 | 0.1698 | 1.05 | 1.72 |

| Legal suitability(Case) | 32.0 | 0.375 | 0.6004 | 0.0 | 2 |

| License acquisition(Subfactor of dummy) | 32.0 | 0.7188 | 0.4503 | 0.0 | 1 |

| Subway in a radius of 5km(Unit) | 32.0 | 6.75 | 11.5044 | 0.0 | 54 |

| Adjacent movie theaters(km) | 32.0 | 2.47 | 3.4084 | 0.27 | 14.68 |

| Adjacent large outlets(km) | 32.0 | 2.684 | 3.1352 | 0.22 | 11.63 |

| Outlet in a radius of 5km(Unit) | 32.0 | 4.5 | 3.7891 | 0.0 | 14 |

| Elementary/ middle/high school/ university in a radius of 5km(Unit) |

32.0 | 5.154 | 6.0948 | 0.596 | 26.31 |

| Business site buying rate(%) | 32.0 | 0.9125 | 0.142 | 0.53 | 1 |

| Period of business suspension (No. of months) |

32.0 | 41.5625 | 30.3913 | 0.0 | 111 |

| Total amount of bonds(x 1 million won) | 32.0 | 41324.6562 | 34623.9782 | 3000.0 | 196614 |

| Amount of obtained bonds(x 1 million won) | 32.0 | 32282.8125 | 17520.8063 | 3000.0 | 68327 |

Table 3.

Results of correlation analysis.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | 11 | 12 | 13 | 14 | 15 | 16 | |

| 1. Bidding result (Subfactor of dummy) |

1.0000*** | |||||||||||||||

| 2.1 Floor area ratio(%) | -0.1027* | 1.0000*** | ||||||||||||||

| 2.2 Building-to-land ratio(%) | -0.0384 | 0.8938*** | 1.0000*** | |||||||||||||

| 2.3 Scale(Unit) | -0.3728*** | -0.1394** | -0.2184*** | 1.0000*** | ||||||||||||

| 2.4 Profitability(%) | -0.1559*** | -0.1441*** | -0.1599*** | -0.0190 | 1.0000*** | |||||||||||

| 3.1 Legal suitability(Case) | -0.1697*** | -0.1011* | -0.1124** | 0.1192** | -0.0380 | 1.0000*** | ||||||||||

| 3.2 License acquisition (Subfactor of dummy) |

-0.1088* | -0.0983* | -0.1806*** | 0.0800 | 0.0063 | -0.4203*** | 1.0000*** | |||||||||

| 3.3 Subway in a radius of 5km(Unit) | -0.2303*** | 0.0601 | 0.0183 | -0.0432 | -0.0601 | 0.4175*** | -0.4553*** | 1.0000*** | ||||||||

| 3.4 Adjacent movie theaters(km) | 0.0906 | -0.2130*** | -0.0229 | -0.0064 | -0.1597*** | -0.1638*** | 0.0511 | -0.1568*** | 1.0000*** | |||||||

| 3.5 Adjacent large outlets(km) | 0.2198*** | -0.2127*** | -0.0174 | -0.1234** | 0.2384*** | -0.2224*** | 0.0569 | -0.2763*** | 0.7347*** | 1.0000*** | ||||||

| 3.6 Outlet in a radius of 5km(Unit) | -0.1407** | 0.0917 | 0.0079 | -0.0681 | -0.0962* | 0.1929*** | -0.2480*** | 0.7134*** | -0.3792*** | -0.5549*** | 1.0000*** | |||||

| 3.7 Elementary/middle/high school/university in a radius of 5km(Unit) | 0.1637*** | -0.2285*** | -0.0218 | -0.0671 | 0.0333 | -0.2060*** | 0.0579 | -0.2298*** | 0.9371*** | 0.9252*** | -0.4975*** | 1.0000*** | ||||

| 4.1 Business site buying rate(%) | 0.0762 | 0.2524*** | 0.2199*** | -0.2735*** | 0.1443*** | 0.1802*** | -0.2733*** | 0.2880*** | -0.6328*** | -0.3780*** | 0.3088*** | -0.5483*** | 1.0000*** | |||

| 4.2 Period of business suspension (No. of months) |

-0.3538*** | -0.1126** | -0.1367** | -0.0667 | 0.2183*** | -0.0717 | 0.3414*** | -0.1150** | -0.0419 | 0.0391 | -0.1840*** | -0.0033 | 0.0804 | 1.0000*** | ||

| 5.1 Total amount of bonds(x 1 million won) | -0.0183 | 0.0056 | 0.0227 | 0.6137*** | -0.0214 | 0.1192** | 0.0771 | -0.0528 | -0.0279 | -0.0291 | -0.1649*** | -0.0306 | -0.2229*** | -0.0761 | 1.0000*** | |

| 5.2 Amount of obtained bonds(x 1 million won) | 0.1335** | 0.1584*** | 0.1850*** | 0.2931*** | -0.0014 | 0.0351 | 0.0113 | -0.0017 | 0.0208 | -0.0267 | -0.1334** | -0.0021 | -0.0257 | -0.0816 | 0.8051*** | 1.0000*** |

Table 4.

Model summary.

| Step | Pseudo R-squared | -2Log likelihood | R-square of Cox and Snell | R- square of Nagelkerke |

| 1 | 0.7851 | 78.524 | .521 | .658 |

Table 5.

Hosmer-Lemeshow Test.

| Step | Chi-square | Degree of freedom | Significant probability |

| 1 | 9.753 | 8 | .247 |

Table 7.

Analysis result.

| Class 1 | Class 2 | significance/weight of criterion | Class 3 | significance/weight of criterion | Final Correction value |

Rank |

| Area of real estate development project valuation | Basic evaluation | 0.188 | Physical suitability | 0.215 | 0.0404 | 14 |

| Legal suitability | 0.422 | 0.0793 | 6 | |||

| Administrative suitability | 0.363 | 0.0682 | 7 | |||

| Feasibility assessment | 0.311 | Analysis of surrounding markets | 0.168 | 0.0522 | 12 | |

| analysis of income and expenditure elements | 0.328 | 0.1020 | 1 | |||

| Analysis of profit and loss indexes | 0.299 | 0.0930 | 4 | |||

| Analysis of investment risks | 0.205 | 0.0638 | 8 | |||

| Business performance valuation | 0.184 | Management ability | 0.452 | 0.0832 | 5 | |

| Business ability | 0.548 | 0.1008 | 2 | |||

| Investor protection plan | 0.162 | Dividend and operation plan | 0.622 | 0.1007 | 3 | |

| Investment collection plan | 0.378 | 0.0612 | 9 | |||

| Other items | 0.155 | Sustainability | 0.387 | 0.0600 | 10 | |

| Eco-friendly factor | 0.271 | 0.0420 | 13 | |||

| Proptech | 0.342 | 0.0530 | 11 |

Disclaimer/Publisher’s Note: The statements, opinions and data contained in all publications are solely those of the individual author(s) and contributor(s) and not of MDPI and/or the editor(s). MDPI and/or the editor(s) disclaim responsibility for any injury to people or property resulting from any ideas, methods, instructions or products referred to in the content. |

© 2025 by the authors. Licensee MDPI, Basel, Switzerland. This article is an open access article distributed under the terms and conditions of the Creative Commons Attribution (CC BY) license (http://creativecommons.org/licenses/by/4.0/).

Copyright: This open access article is published under a Creative Commons CC BY 4.0 license, which permit the free download, distribution, and reuse, provided that the author and preprint are cited in any reuse.